12 July 2025

1300 794 893

Former PM and Treasurer, Paul Keating, once created what was called the “recession we had to have” because of our excesses of the 1980s that resulted in big borrowing, inflation, and home loan interest rates of 17%. Mr Keating talked about “burning” inflation out of the economy but a recession would result, and it did in 1990 with unemployment going over 10%! It’s now 3.7%.

However, if the RBA’s Dr Phil Lowe is not careful, we might end up in the recession we didn’t have to have.

And this construction story should be heeded by the RBA.

Nine interest rate rises in less than a year might not yet have killed inflation but it has KO’d the building sector, and it will take some time before it gets up off the canvas. This is why the Reserve Bank’s Dr Phil Lowe and his board have to be careful about rate rises going forward.

Why? Well, at the start of this inflation surge one sector that was leading the price rise hikes was builders. Stuff from OS, used on building sites, was up in price because of supply chain problems, especially in pandemic-locked-down China.

Also, there was a labour supply problem with half-a-million foreign workers exiting Oz to wait out that damn Coronavirus.

The above problems saw builders add 20% to quotes for upcoming jobs. Also, when homeowners or developers changed plans on building and renovation sites, as the work progressed, the extra cost was increased by 20% rather than the old 10%.

That added to inflation, which here got as high as 7.8% by the end of 2022.

And that was despite the fact, that interest rates were lower than they were when builders wacked on the 10% extra cost for unexpected changes to plans from an owner, in pre-pandemic Australia.

Funny that.

Now the Tele reports that the Housing Industry Association’s latest Economic and Industry Outlook Report says nine consecutive interest rate increases have seen housing construction starts plunge. We’re looking at the worst year in over a decade for the sector.

“There was a large volume of work in the pipeline when rates started to rise in May 2022, and there remains a record number of homes under construction but this will shrink quickly as market confidence continues to fade,” said Tim Reardon, the HIA chief economist.

“Lending for the purchase or construction of a new home had already fallen to its lowest level since 2012 by the end of 2022, and the full impact of last year’s rate increases is still to flow through to households,” he explained.

The Tele reports that the industry recorded 120,000 detached housing starts in 2022 and has forecast 109,000 in 2023. In 2024 it is estimated the number of detached housing starts will fall below 100,000 starts per year for the first time in a decade to just 96,300, compared to a 149,000 starts in 2021.

And you can bet current interest rates will be stopping would-be renovators from borrowing and that will also hurt the building sector.

The RBA screwed up after the 2008 GFC when their rate cuts saved us from a recession, which was good work considering nearly all Western economies went into recession. However, they raised them quickly again and by 2012 the building sector was stuffed.

Subbies United’s John Goddard thinks the Government needs to look at insolvency processes that he says favours liquidators, their lawyers and referral networks.

He says tradies and builders are exposed but so are their unsecured creditors, such as a plumber, who works on a building site where the builder goes broke because of these nine-interest rate rises.

By the way, sometimes builders are accessories to this problem.

“I know of dozens of subbies who have been destroyed by liquidating builders,” Goddard revealed. “We know of builders who have made an art form out of liquidating their companies.”

What’s worse is that history says it will be the building sector first that falls in a hole because of nine interest rate rises, which could easily become 11 before the year is out if economists are proved right with their rate rise predictions. However, after that, manufacturers and businesses catering to discretionary retail-buying consumers and even cafes and restaurants will feel the pinch when home loan repayments make non-essential spending harder to do for struggling mortgagees.

This is the anatomy of a recession and Dr Phil and his board will be to blame if they fail to gamble that we have had enough rate rises already to beat inflation by year’s end, which is a reasonable time to lower prices.

Economists might be predicting two more rate rises but that’s not to say that they all think we need them. Many just play the guessing game of what they think the RBA will do.

That mortgage cliff of fixed rate borrowers rolling onto variable rate loans starting mid-year will be a big kick in the guts for the economy and will do more to kill inflation than two more rate rises. However, together both spending-killing actions — rate rises plus borrowers going over the mortgage cliff — could turn an economic slowdown into a recession.

By the way, the Yanks too are starting to worry that their inflation-killing interest rate rises could be excessive and might bury their economy.

Wall Street was very negative overnight and could easily remain so until the US statistician produces economic data that says the economy is slowing enough to make it easy to believe that inflation is really falling.

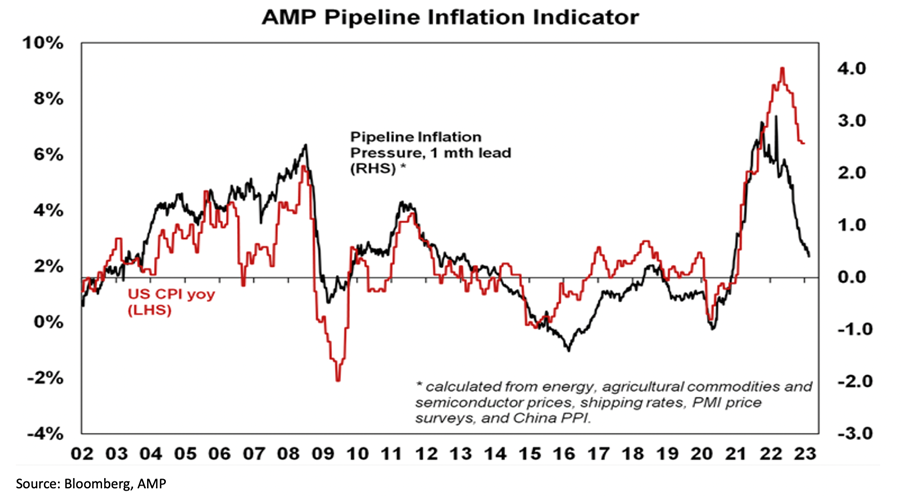

Like here, it will happen soon and this chart from AMP’s Shane Oliver shows it. It’s called the Pipeline Inflation Indicator. The black line shows how goods inflation is tumbling in the US but services inflation is still higher but like in our building sector, a threatening recession will even slow down wage and other service prices. It just takes a little longer.

I’d love Dr Phil to beat inflation ASAP so rates can fall and we can dodge a recession, and then we might stop bringing up his no rate rises until 2024 blooper.

That would be a win-win outcome for us and the good doctor.