3 July 2025

1300 794 893

One of the world’s most famous historians, Niall Ferguson, has suggested that “the world is sleepwalking into an era of political and economic upheaval akin to the 1970s — only worse” CNBC’s Karen Gilchrist informs us.

Ferguson has been a Harvard Professor and has written something like 16 books, with his latest called 'Doom: The Politics of Catastrophe'.

Ferguson is a well-qualified historian but isn’t an economist but he’s always happy to offer his best guesses on what lies ahead.

As someone who tries to hose down the views of extremists (that grab headlines and sell books) because I have to talk to our advisory clients, subscribers, listeners, viewers and followers on the subject of investing, I’ve occasionally had to evaluate Ferguson’s big calls.

While he has got some right, he’s got some wrong but my colleagues in the media don’t seem interested in reminding us that he’s fallible.

So what does Ferguson say about the 1970s that could be repeated? “The monetary and fiscal policy mistakes of last year, which set this inflation off, are very alike to the 60s,” he said, likening recent price hikes to the 1970′s doggedly high inflation. “And, as in 1973, you get a war,” he continued, referring to the 1973 Arab-Israeli War (also known as the Yom Kippur War) between Israel and a coalition of Arab states led by Egypt and Syria.

He’s probably right in arguing that “this war is lasting much longer than the 1973 war, so the energy shock it is causing is actually going to be more sustained,” but how the world responds today could be very different to the world of 50 years ago.

As an economist who has had a healthy interest in economic history, I know the economic world of 1973 is very different to that of 2022. The political events could be similar, but the world today is no longer excessively regulated with tariffs and nationalistic protections. Unions have less power and so a wage-price spiral is less likely, reducing the chances of stagflation showing up, with both rising inflation and unemployment.

The financial system is more deregulated, money markets send signals to central bankers and governments like never before. And the Internet has created a world that means competition has escalated such that if workers want to hold employers to ransom, they might lose work to rivals in Asian countries.

Economists say that there have been structural changes to our economies, which means what we used to think was a relationship in the economy might not work the way it used to. For example, once upon a time when a bank raised interest rates, we all paid higher rates. However, since the 1990s, products such as fixed rate loans, interest-only loans and offset accounts have changed how monetary policy might work.

Here's another example from the RBA Financial Stability Review of securitisation data that says the median excess payment buffer for owner-occupiers with a variable-rate mortgage was about 21 months’ worth of scheduled repayments in 2022 – up from about 10 months at the onset of the COVID-19 pandemic.

This was not around in the 1970s.

Our new world of borrowers has created buffers that actually help those in debt to weather rising interest rates, and this affects the success of monetary policy.

What I’m trying to say is that Ferguson’s 1970s comparison of similar political events might be happening in a very different economic world.

The history I’ve written around since 1985 in the media has had four stock market crashes:

But the world’s economies and stock markets muddled through.

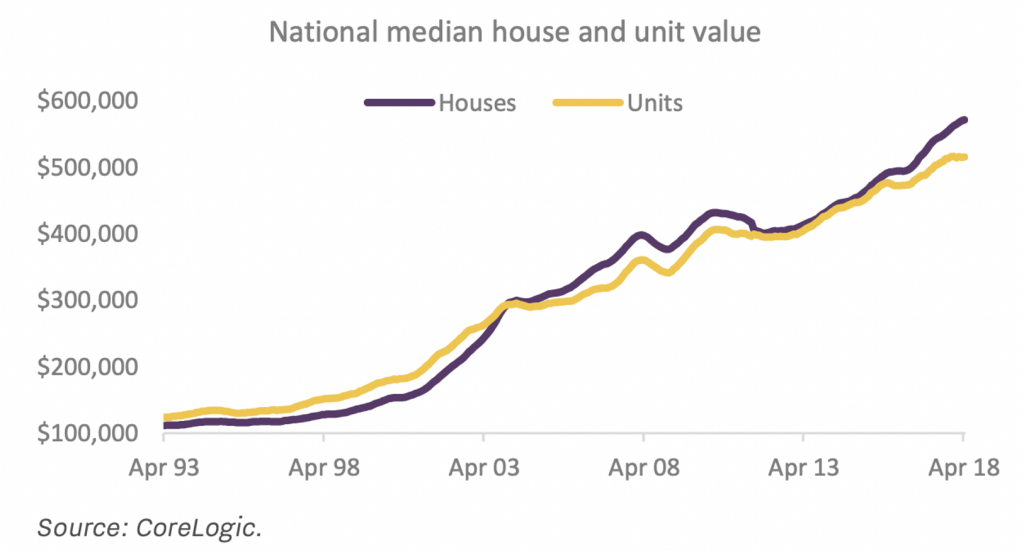

We’re great muddlers. The worst thing you can do is overreact and make investment decisions based on doomsday predictions that mean you lose out. And this chart shows why being invested in property for the past 25 years has been a good idea.

Property prophets have been telling us for decades to beware of a bubble bursting. One day it probably will, but these doomsday merchants have had ‘a long run of outs’ with their predictions. As urban.com.au reported, “Jeremy Grantham, the co-founder of Boston-based hedge fund GMO, caused a stir in April 2010 when he declared a housing bubble in Australia and said prices would tumble as interest rate rose [the Reserve Bank pushed rates up by 25 basis points to 4.25% in April 2010].”

If you’d listened to Jeremy, you missed 12 years of a 25-year bull run for house prices. You also would have missed last year which saw national average home prices rise 22%, their fastest 12-month increase since 1989!

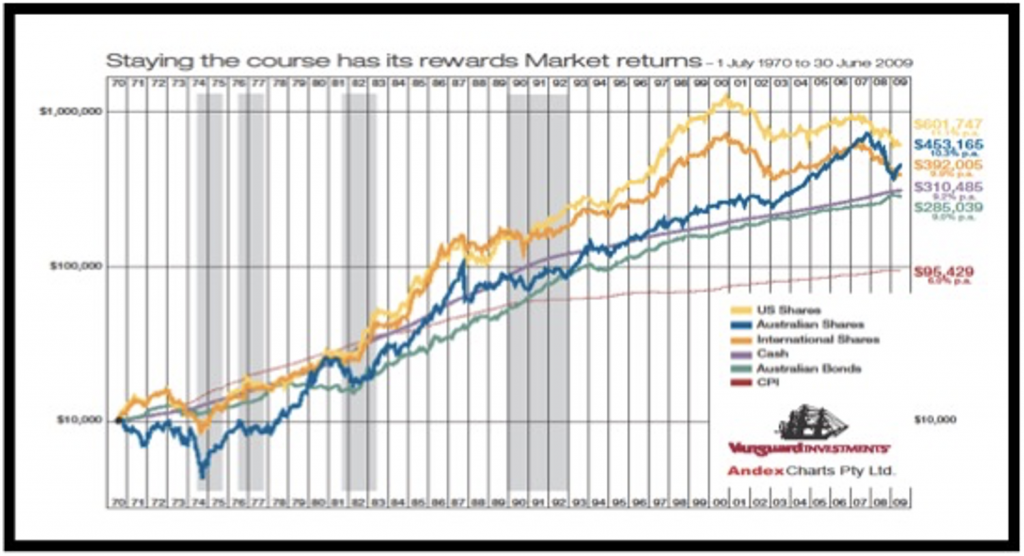

Whenever a pessimist gets me nervous, I go back to this chart from Vanguard of someone being invested in the All Ords and reinvesting the dividends from 1970 to 2009. That was one year after the GFC crash took stocks down by 50%. Even with that, and the 1987 crash and the dotcom crash, $10,000 invested and allowed to roll over turned into $453,542!

That’s the return from being invested in quality assets and having faith in the power of economies, companies, governments and central banks that all muddle through to deliver returns of about 10% per annum over a decade.

Some decades it could be less and in others, it might be higher, but a history lesson Niall Ferguson doesn’t push is one that smart investors (like Warren Buffett) have been telling us about for decades — invest in quality assets, be greedy when others are fearful and “our favourite holding period is forever”. But remember, Buffett was talking about quality assets — these have the ability to survive doomsday scenarios.