12 July 2025

1300 794 893

On a day when the borrowers of Australia hold their breath to see what new interest rate misery the RBA will impose on them, a sound-of-mind Aussie asks why do the banks play ball with Dr Phil Lowe and his hip pocket torture?

However, when a normal rational person ponders the thinking of economists, Reserve bankers, Treasurers and big bank CEOs, they encounter what could be called — “don’t go there, mate” analysis.

Matt Summerill, Business Director at SUMM Media, sent an email to my colleague and breakfast host on 2GB, Ben Fordham, which sounded completely sensible. Ben asked me to answer the questions posed by a guy who might understand business and customers, but clearly not bankers and dark art practitioners called economists!

Matt points out that banks don’t have to, by law, follow the RBA and raise interest rates. And given around 800,000 borrowers are expected to fall over a ‘financial cliff’ around July this year, as they roll onto high interest rate variable home loans after years on low fixed rate loans, what’s the good sense of banks killing customers?

This shows what an enlightened business operator Matt is, when he wrote: “The bank is in partnership with the customer on the ownership of the property. If the customer defaults and the property has to be sold, would the bank lose as much as the customer?”

Let’s look at Matt’s thinking one step at a time.

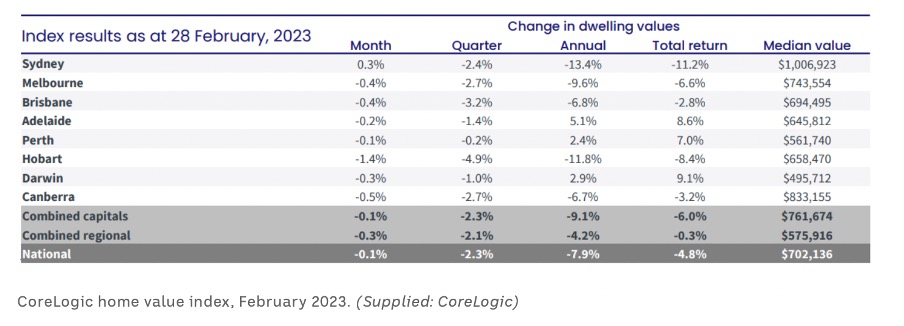

First, only if the house price fall was as bad as some doomsday merchants have predicted would the bank lose out in an enforced sale that it imposed on the borrower. That’s why we have deposits, that gives the bank a safety buffer in case of a debt default issue. By the way, the annual fall in house prices is slowing down, with the national drop being only 7.9%, while Sydney is down 13.4%.

Second, banks are fair weather friends — if you’re doing well, they can be great partners but as soon as you become a risk, they have to put the interests of the owners — i.e. the shareholders — first. Sure, keeping customers financially alive should be a win-win thing, but that would mean the bank might have to cop short-term profit falls or even losses, which would hit the share price and annoy shareholders. This then would reflect badly on the CEO of the bank, and as Paul Keating once effectively said: “If you go to the races and you see a horse called Vested Interest, back it because you know it's trying.”

If a CEO had to choose between his job and a pile of customers, most would choose themselves.

Third, if a bank didn’t pass on the interest rate rise, their profits compared to the others would be negatively affected and their share price would fall. Stock market investors on a daily basis. are very short-term focussed.

Fourth, banks would argue that if the RBA raised rates to kill inflation and they didn’t support the central bank’s actions, then they could be accused of working against the national interest. This could draw criticism, not only from Dr Phil but also Dr Jim Chalmers, because he keeps telling us how inflation is our biggest economic enemy.

Fifth, banks might also argue that the Treasurer and the media are always quick to bag banks if they don’t pass on rate cuts, so they should be able to pass on rate rises.

Matt, I learnt a long time ago, in fact from a US business guru Jay Abraham, that in business you should always be looking at the value of the long-term relationship. This means sometimes you might have to cop lower profits or even losses short term for a longer-term pay-off.

Banks will do this with big valuable irreplaceable customers, such as businesses and high net-worth clients, but many borrowers are seen as potential churn-and-burn temporary customers, especially in the age of mortgage brokers and refinancing. Therefore, a lot of Aussies will go over the so-called mortgage cliff and bank CEOs will keep their fingers crossed that it doesn’t become a widespread recession, which will hit their profits and their share prices.

In that situation, banking CEOs could see themselves as accessories after the fact, and they would be comfortable holding Dr Phil and Dr Jim as the real culprits in the piece.

Good try, Matt, but your arguments will never wash with the banking part of the big end of town.

One last thing. Comedian Bob Hope once said: “A bank is a place that will lend you money if you can prove that you don't need it.”

And then there is from the poet, Robert Frost: “A bank is a place where they lend you an umbrella in fair weather and ask for it back again when it begins to rain.”