2 July 2025

1300 794 893

This is a huge week for stocks, with the US election bound to have market and economic consequences. And the Reserve Bank is near certain to cut the cash rate of interest on Tuesday from 0.25% to 0.1%. To any normal person, this looks a little crazy but don’t you dare complain, even if you’re a saver who wants higher interest rates. (I’ll explain this warning below.)

That said, with second-wave Coronavirus infection rates spiking in Europe and the USA, which is leading to lockdowns in the UK, France, Germany and in other countries, the need for the RBA to do “whatever it takes” (as the old saying goes) has become more imperative.

An escalation of lockdowns means global economic growth will be less. That means more stimulus from local sources will become more important. Even before these infection/lockdown threats, the RBA was bound to cut the cash rate on Tuesday, as Cup Day is famous for rate rises and cuts.

Why? Well for starters, there’s RBA board meeting in January and because the Christmas shopping period is a big deal for the economy, and because interest rate changes don’t work instantaneously, the RBA often sees good reason to move in November.

If the economy is booming and looking very inflationary, it raises rates, and vice versa. It’s cut time now and the local lockdowns in Victoria are a part-reason why the RBA would have pencilled in another cut. The Big Bank wouldn’t have wanted to do this but getting economic growth (whatever the cost) is critical.

That’s why the October Budget is expected to be around $213 billion this financial year but Treasurer Josh Frydenberg has admitted that if our economy does better and is helped by an early proliferation of a vaccine, there could be a $34 billion saving (or reduction) in that Budget bottom line!

Now you might be saying, how does a cut from 0.25% to 0.1%, help? Getting bank interest rates down to encourage borrowing, consumption and then business investment to get the economy rolling with a full head of steam creating jobs before March (when the Treasurer plans to stop JobKeeper) is a big deal.

The RBA is like the godfather of banks. This rate cut is an offer of “when we cut, you cut” and is one the banks can’t refuse.

If they do, the PM would garrot them in the Parliament and pillory them with all the insults that came out of the Hayne Royal Commission. And anyway, the Morrison Government is dangling the end of the responsible lending legislation that has made borrowing too hard for too many households and businesses.

If the Government can change the toughness of responsible lending that has made bank loan officers as forensic on a borrower’s spending as tax office investigators (when they’ve caught a taxpayer red-handed dodging tax), then there’ll be an economic dividend.

And the economy needs all the business creating dividends it can muster right now. That’s why a rate cut is coming.

A lower cash rate will cement more low-fixed rate home loan rates of interest, which right now are as low as 2.59% fixed for five years at UBank! In all likelihood, a cut will keep rates lower for longer, unless we get an extremely huge growth spurt here and worldwide in 2022.

Why 2022? Well, 2021 is bound to be better than 2020 but these lockdowns globally and the wait for a vaccine means the enthusiasm for businesses to invest and to create jobs, and consumers to spend, will be curtailed until the world thinks the worst of this Coronavirus is behind us.

I know we have occasional reasons to gripe about some of the problems with Australia and Australians but given what’s happening in most of the nations and economies we compare ourselves to, we’re one of the luckiest countries on the planet.

For savers who want higher interest rates, you can only get these if the economy is growing and threatening inflation.

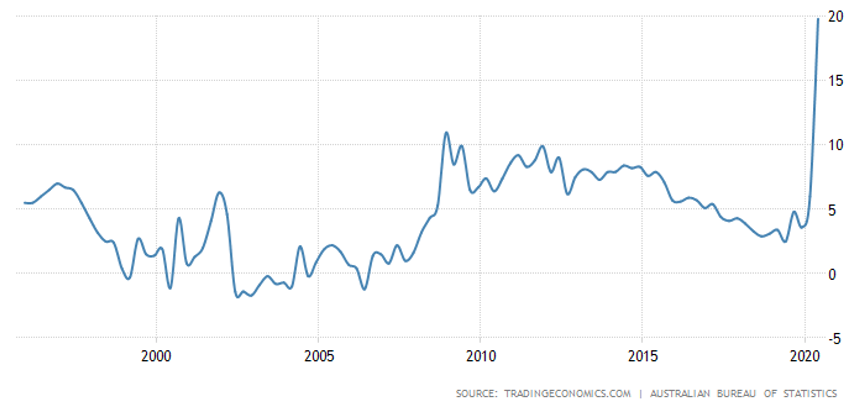

Our saving ratio

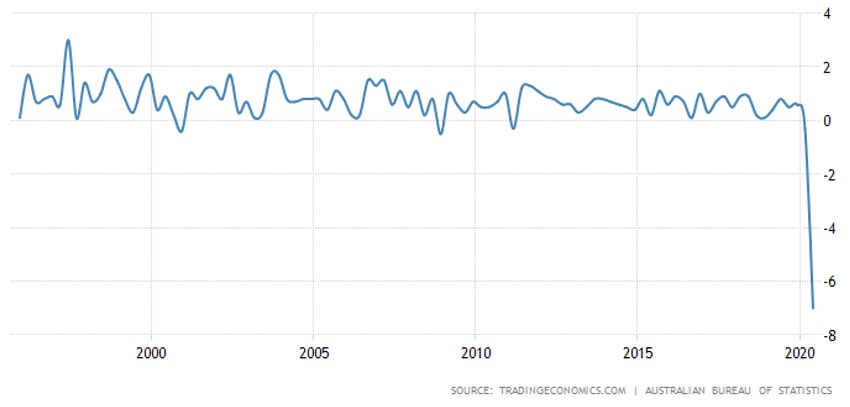

Our economic growth

When we go into recession, fear increases the saving ratio and there’s too much money saved when fewer people want to borrow or are in a position to qualify for a loan. When we grow faster, we spend more and save less and interest rates rise to attract more money to banks, which then lend it out to borrowers who are mad keen to do ‘stuff’. Ultimately, growth will be good for savers, so cop the cut and don’t even think about whinging!