12 July 2025

1300 794 893

Stories about rising interest rates and confidence falling tell us a lot about how confusing indicators about inflation, recession, job losses and stock market collapses can be. Right now what could be an excessive call on rising interest rates and hard-to-beat inflation is worrying economists and their anxiety has been passed down to consumers and, undoubtedly, business owners via the media.

Of course, that’s the media’s job — to report what experts like economists have to say — but sometimes there can be an excessive preoccupation with one side of an argument or story.

This came to me at 5.30 this morning as I watched US business TV CNBC and pedalled away on my Nordictrack exercise bike, which is a local business success story I’d like to tell you about one day.

At that time, Spiro, my colleague at 2GB texted me telling me the breakfast host Ben Fordham wanted to cover the story about falling consumer confidence, which came out of an SMH report from Shane Wright.

Sensibly, Ben linked the latest reading from consumers and their confidence to the big event on Saturday — the federal election.

And while there have been many issues grabbing headlines during the campaign, the cost of living and the expectation of rising interest rates is at the core of a lot of the vote-catching talk from politicians out on the hustings.

Interestingly, Shane revealed that the RBA minutes say the Board was considering a 0.4% interest rate rise, which would’ve been a shocker to those with loans, and I’d say also for the Morrison Government.

This news makes the 0.25% rise look a lot more digestible!

And what hovers in the minds of those voters with loans is that more interest rate rises are coming as inflation couldn’t be on the way down yet. In fact, some economists think the cash rate could be 1.5% by year’s end and some are talking about 2% or 3% within 12 months!

That would crush those in debt and I reckon deliver a recession and I can’t believe that future inflation will merit such rises. I also don’t think the RBA is that dumb!

That’s my best guess but I know CBA’s Matt Comyn is in my camp predicting much smaller rate rises. This is what the AFR’s James Eyers wrote last week: “Commonwealth Bank of Australia CEO Matt Comyn says home-owners may be worrying unnecessarily about the pace of interest rate rises over the next 12 months, because he has confidence in the bank’s forecasts that the cash rate will rise to only half the levels predicted by the market.”

The CBA tips the cash rate only going to 1.35% this year and 1.6% by next year. The excitable people in the bond market have the cash rate at 2.5% by the end of 2022 and 3% plus by next year!

With stories like that, why wouldn’t consumer confidence be dropping? This is what CommSec’s Craig James told us yesterday: “The ANZ-Roy Morgan consumer confidence index fell by 1.3% last week to 89.3 points (long-run average since 1990 is 112.4). It was the fourth straight weekly decline in confidence.”

By the way, this could get worse in the short term, with Westpac’s Bill Evans tipping a 0.4% rise next month taking the cash rate to 0.75%, which would add $172 to the monthly repayments on an $800,000 mortgage.

And if they do this, confidence will plummet and I suggest wage data out today could determine what the RBA’s June 7 rate rise ends up being.

In the short term, I can’t see any positive news to break us out of this current negativity. Other stories I came across while I was pedalling (and you were probably sleeping!) make me think that the bad stuff out there about inflation, interest rates and very negative stock markets could soon change.

Overnight, US stock markets were strongly positive with the Dow up 431 points (or 1.3%), the S&P 500 up 2.02% and the Nasdaq put on 2.76% and you get the feeling that many in US stock markets think that the sell-off of stocks was over-the-top and maybe it’s time to peel back the too negative story about interest rates.

“Our inputs today support the kind of momentum that we saw on Friday and a continuation of that,” said Art Hogan, chief market strategist at National Securities. “But the most important thing for investors is you get to a point where you’ve priced in a lot of worst-case scenarios.” (CNBC)

It's too early to call the sell-off of stocks over, but better news is seeping in. Like what? Try these:

1. The Fed has ruled out 0.75% interest rate rises.

2. Goldman Sachs chief bond guy Jonathan Fine thinks the bond market is toning down its fast-rising interest rate fears.

3. China thinks the lockdown will end in June.

4. Recession fears are lessening in the US.

5. The latest US job number showed a slowing of wage rises.

What one expert on CNBC reminded me of was the strength of consumers’ balance sheets because of government payouts and how the lockdowns reduced our spending. Like Americans, our personal balance sheets are much stronger than ever before.

We apparently have $270 billion of savings in our bank accounts, which will help a lot of us cope with rising interest rates.

Also, lots of Australians don’t have home loans and retirees will save more with rising rates.

I’m tipping that over the next few months confidence will rise, inflation will start to fall after a few months of more rises, predictions of interest rate rises will be reduced, the stock market will love this news and confidence will turn on a dime and head up.

I wrote yesterday that investing now in stocks is for the courageous but there are some positive signs developing, as I showed above.

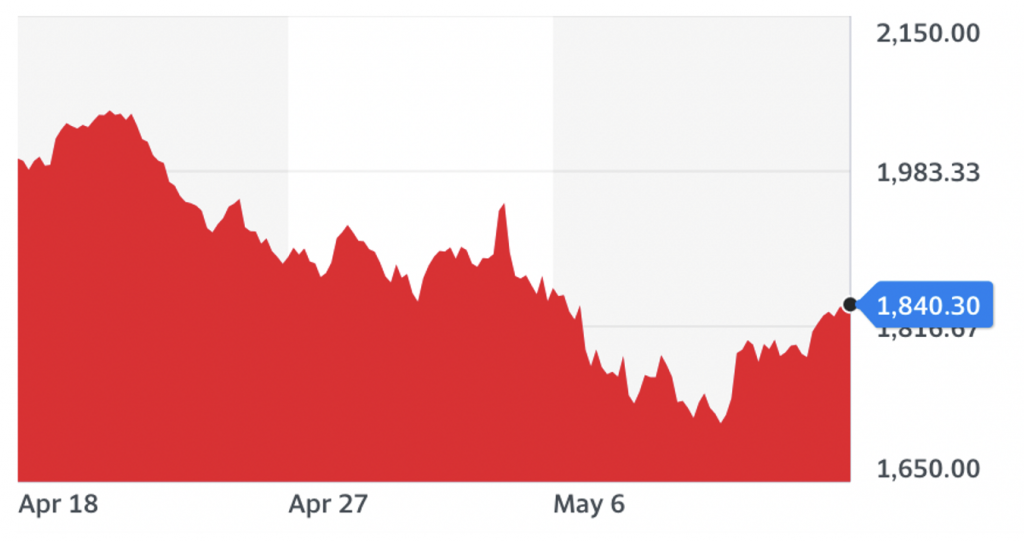

Interestingly, the Russell 2000 Index looks at US small cap companies and it has been starting to outperform the bigger cap company indexes, which can be a good omen for stocks.

Russell 2000 (RUT)

The Dow is up 4.17%, the S&P 500 Index is up 5.4% in the past month, while the Russell is up 7.4% — and that’s a trend I hope continues.

A lot of good stuff needs to happen to turn this market uptick into a sustainable trend, but one takeout message could be that the stock market sell-off and the interest rate fears have been more negative than they needed to be.

If China can escape lockdown and the Ukraine war can end ASAP, you will see how right my guarded optimism will be, but I admit there are a few ‘ifs’ and ‘buts’ in my story.

And I guess if I’m proved wrong, many of you might say: “On your bike, Switzer!”