2 July 2025

1300 794 893

Investors desperate for fixed interest style investments with a little bit of yield will gobble up National Australia Bank’s new hybrid securities issue, NAB Capital Notes 4. Set to pay a fixed margin of 2.95% over the 90 day bank bill rate and an offer size in excess of $750m, the final terms of the issue will be announced after a bookbuild early next week.

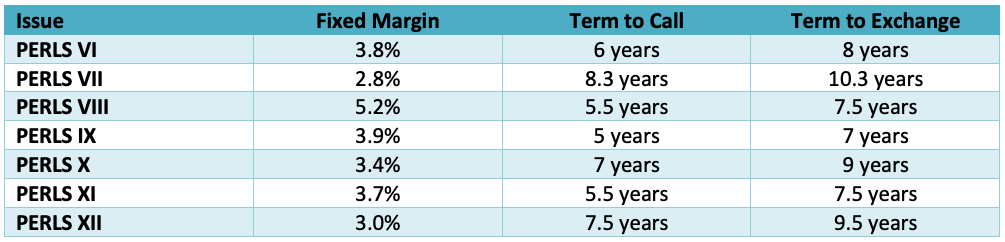

Historically, a margin under 3% would be considered to be on the light side, particularly for an issue with a term of almost 7.5 years to the call date (see table below for the biggest issuer, CommBank, and the issues of its equivalent PERLS capital notes over the last 7 years).

However, the environment for hybrid securities is very different today. Firstly, banks are stronger and better capitalized following APRA’s requirement that they become “unquestionably strong”. But perhaps more importantly, the thirst for “secure” yield has never been stronger following the cut in the cash rate by the RBA to just 0.75% and the flow on effects to term deposit interest rates and government bond yields.

The 2.95% margin also sits nicely compared to where CommBank’s PERLS XII is trading in the secondary market on the ASX (around 2.8%) and the recently announced issue of capital notes from Macquarie Bank, which were priced at a margin of just 2.9%. I expect this issue to be met by very strong investor demand. Here are the details.

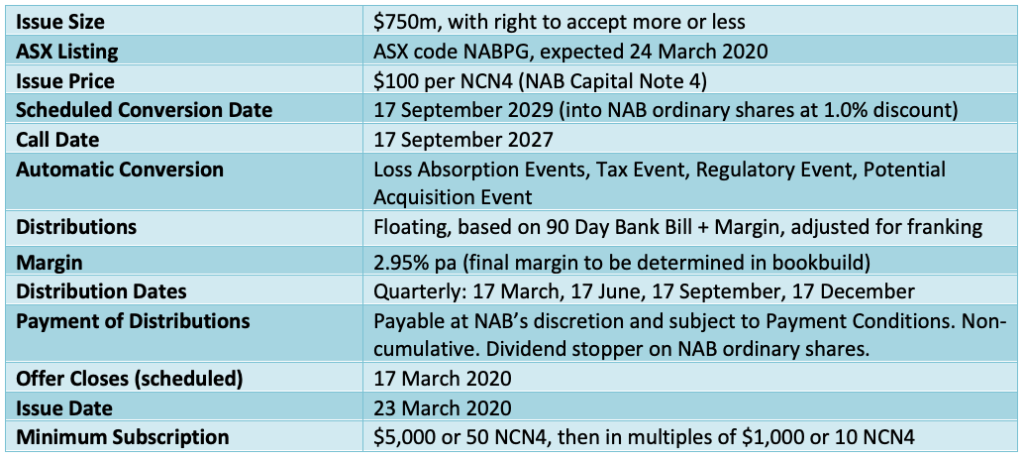

NAB Capital Notes 4 (NCN4)

NAB Capital Notes 4 (NCN4) will pay a quarterly, fully franked distribution. This is calculated at a fixed margin of 2.95%over the then 90-day bank bill rate, and then adjusted by the company tax rate (to take into account the benefit of the franking credits). The distribution is re-calculated each quarter based on the then current 90 day bank bill rate.

With the 90 day bank bill rate currently around 0.90%, this implies a gross distribution rate of 3.85% pa for the first 3 months (0.90% plus 2.95%). The actual distribution in cash, which is adjusted down for the franking credit benefits, would then be 2.70% (3.85% x 0.7 = 2.7%).

If for the following quarter the bank bill rate has moved higher to 1%, the gross distribution for that quarter will be 3.95%. On the other hand, if the RBA continues to cut interest rates and the bank bill rate falls to 0.5%, the gross distribution rate will be 3.45%.

Distributions are discretionary and subject to payment conditions. If a distribution is not paid, it doesn’t accrue and won’t subsequently be paid. To protect holders from this discretion being miss-applied, National Australia Bank is then restricted from paying a dividend on its ordinary shares.

Conversion into NAB shares or Early Repayment

NCN4 are perpetual and have no term. However, NAB must (subject to a test) convert NCN4 into NAB ordinary shares on 17 September 2029 (in about 9.5 years’ time). If conversion occurs, holders are issued $101 of NAB ordinary shares for every NCN4 of $100 face value (which effectively means that they are issued NAB shares at a 1% discount to the then market price). The test for the conversion is the price of NAB ordinary shares at the time – provided they are higher than approximately $13.80, conversion occurs – otherwise, it is retested on the next and subsequent distribution date(s) until the test is met.

To qualify as regulatory capital for NAB, two loss absorption events cause automatic conversion - a ‘common equity trigger event’ and a ‘non-viability trigger event’. Under these tests, the Australian Prudential Regulatory Authority (APRA) can require NAB to immediately convert NCN4 into ordinary shares if NAB’s Common Equity Tier 1 Capital Ratio falls below 5.125% (the ratio was 10.6% on 31/12/19), or if it believes NAB needs an injection of capital to remain viable. In these distressed circumstances, exchange would most likely result in a holder receiving considerably less than $101 of NAB ordinary shares as there is a cap on the maximum number of shares that can be issued.

NAB also has an option to convert the NCN4 early on 17 September 2027 (in approximately 7.5 years’ time) by paying holders $100 per NCN4. This is at the Bank’s sole option (not the investor’s option), and as all previous issues of major banks’ capital notes have been “called” early, the secondary market will initially trade and price NCN4 on the assumption that they will be redeemed early in September 2027 for $100.

The table below summarises the offer details:

How to invest

Following a bookbuild by institutions and brokers this week that will set the final margin (the Bank has indicated a range of 2.95% to 3.15% but it is absolutely odds on that it will be 2.95%), the Offer will open on Tuesday 25 February. It is scheduled to close on Tuesday 17 March.

There are three offers – a Broker Firm Offer, a Securityholder Offer and a Re-Investment Offer. Several brokers and financial planners are involved in the issue, including Morgans, Morgan Stanley, Ord Minnett, UBS, Bell Potter, J B Were and Shaw and Partners. If you are investing via a broker or financial planner in the broker firm offer, they are receiving a selling fee of 0.75% of the proceeds invested and, in some cases, may be willing to share some or all of this with potential investors.NAB shareholders and holders of NAB Income Securities, NAB Subordinated Notes 2, NAB Convertible Preference Shares II, NAB Capital Notes, NAB Capital Notes 2 and NAB Capital Notes 3 can also access NCN4 directly through a Securityholder offer at www.nab.com.au/NCN4offer

There is also a re-investment offer for holders of NAB Capital Notes (which trade on the ASX under code NABPC). These are being called and redeemed – holders can at their option elect to re-invest the proceeds into NCN4.

Don’t invest in something you don’t understand

Hybrid securities such as NCN4 are complex investments. If a banking crisis happened in Australia or National Australia Bank got into real financial difficulties, investors could potentially lose most if not all of their capital. So, it is important to understand the risks of investing and how the securities work.

You can learn more about hybrid securities at ASIC’s MoneySmart website (go to https://www.moneysmart.gov.au/investing/complex-investments/hybrid-securities-and-notes). Also, NAB has developed an education guide at www.nab.com.au/hybrideducation

As the old adage goes, don’t invest in something you don’t understand.