19 July 2025

1300 794 893

Welcome to the new financial year!

As usual, there are changes to tax, super and health insurance …….and those dreaded road tolls. Here is a rundown on the changes that could impact you.

1. Taxes

The good news is that there is no increase to personal tax rates. The bad news is that there are no cuts, nor are thresholds being increased.

Claiming a tax deduction for working from home expenses will be more onerous as the ATO ends its special Covid-19 shortcut method. This was introduced to cover anyone who worked at home during the period 1 March to 30 June and gave a blanket deduction of 80c per hour worked (no receipts, just a simple diary).

Companies will see their tax rate come down. In 20/21, companies with a turnover under $50m will pay tax at 26% - down from 27.5% last financial year. Another cut next year will see the rate reduce to 25%. Bigger companies will continue to pay tax on profits at 30%.

They will also be able to access the instant asset writer-off, which allows businesses with a turnover of less than $500m to instantly write off 100% of equipment purchases up to $150,000. Back in June, the Government announced that it was extending the scheme until 31 December 2020.

The threshold of $150,000 excludes GST, so businesses can potentially purchase an item that costs up to $165,000 (including GST). It can be new or second-hand equipment, applies to motor vehicles including utes, although a limit of $57,581 applies to passenger vehicles, and is available on a per item basis and can apply to multiple assets.

The tax on jobs…payroll tax…is being reduced in some states. In NSW, the threshold to payroll tax rises by $100,000 to $1,000,000. This will save bigger companies $5,450 and mean others will stop paying any payroll tax. In WA, the threshold will also rise to $1,000,000.

2. Super

There are five changes to super. The big one is that Australians aged 65 and 66 years will be able to make a contribution to super without having to meet the work test. This covers both concessional and non-concessional contributions, and essentially means that ‘67’ is the magic super age, just as it is for aged pensions.

Along with this change, the Government says that it will legislate to allow 65 and 66-year-old persons to access the “bring-forward rule”. The rule allows an individual to make up to 3 years of super contributions in one hit. This means that a 66-year-old could potentially contribute $300,000 into super, a couple could get $600,000 into super.

The age limit for spouse contributions will increase from 69 years to 74 years.

The final two changes relate to Covid-19 relief measures. If you have been adversely financially affected by Covid-19, you can apply to access up to $10,000 of your super. This is in addition to any amount you accessed last financial year (i.e. prior to 1 July), and is only available to citizens and permanent residents. The early release scheme closes on September 24.

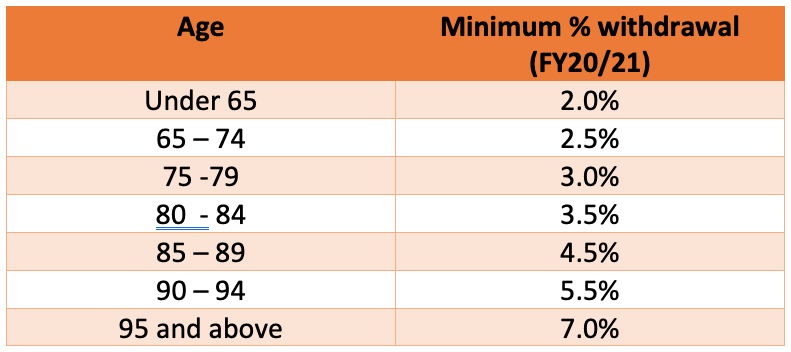

To assist retirees who depend on account based super pensions, the Government has reduced the minimum annual payment by 50%. The minimum payment is based on your age, according to the factors in the following table:

For example, if you were aged 66 on 1 July and had a balance of $1,000,000, your minimum payment is 2.5% of $1,000,000 or $25,000. You can take your pension at any time or in any amount(s), but your aggregate drawdown over the year must exceed the minimum amount. If you commence a pension mid-year, the minimum amount is pro-rated according to the number of days remaining until the end of the financial year.

3. Health Insurance

The good news is that most private health insurers deferred any premium increase for 12 months. This is because the Covid-19 lock down led to halt on elective surgery, and private hospital visitations and allied health treatments plummeted. The insurers had almost no claims.

Some insurers indicated that they were considering providing members with a premium rebate, although as time marches on, they seem to be walking away from this commitment.

4. Low deposit home loans

The government is making another 10,000 low deposit loans available to first home buyers under the First Home Loan Deposit Scheme. Eligible first home buyers can purchase a modest home with a deposit with as little as 5 per cent, rather than the normal 20%. Singles must earn less than $125,000, while couples need to have a taxable income under $200,000. There are also property price caps e.g. $700,000 for Sydney, $600,000 for Melbourne.

Applications are made directly to the participating lenders (there are 27 banks, including the Commonwealth and NAB).

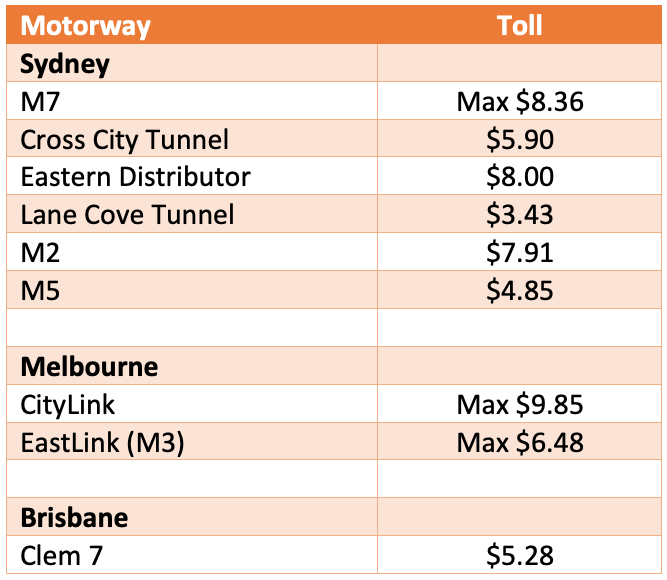

5. Tolls go up

Another quarter, another road toll increase. And do not believe that tolls just go up at the rate of increase in the CPI (consumer price index), most tolling agreements have inbuilt minimum increases that ensure they increase at a rate that is higher than the inflation rate. The State Governments who sold these tolling concessions gravely misled the public over this matter.

Listed below are some of our major tollways, and the prices you are now paying.

And if you want to get square, buy some shares in Transurban, Australia’s largest toll road operator. Interestingly, Transurban has just squeezed into the top 10 companies by market capitalisation on the ASX. What a river of gold!