12 July 2025

1300 794 893

The Coronavirus crash is creating some interesting opportunities with bank hybrid securities. Yields in the secondary market on the ASX have blown out by more than 1.5% over the last week, taking them to levels not seen for some years. And this is in an environment of ultra-low interest rates.

As the name implies, hybrid securities are a cross between fixed interest style securities and shares. A bit like the Toyota Prius motor car, which is also described as a “hybrid”, these securities have both capital and debt like features. Issued mainly by the major banks, they technically qualify as Tier 1 capital for the banks. Marketed under the generic name ‘Capital Notes’, they are potentially perpetual and in certain situations, are automatically exchanged into bank ordinary shares. On the debt or fixed interest side, they pay a regular quarterly distribution which is reset every quarter at fixed margin over the then market rate.

Importantly, they are not bank deposits, nor are they covered by any Federal Government guarantee. If a bank is wound up, they rank right near the bottom – only just ahead of ordinary shareholders. If a bank gets into serious financial stress, the chances are that you will lose most if not all of your investment. I consider them to be part of my “risky fixed interest” portfolio.

The flipside of course is that where there is risk there is the potential for higher return. A possible grossed up return near 5% looks reasonably attractive compared to term deposits paying around 1.2%.

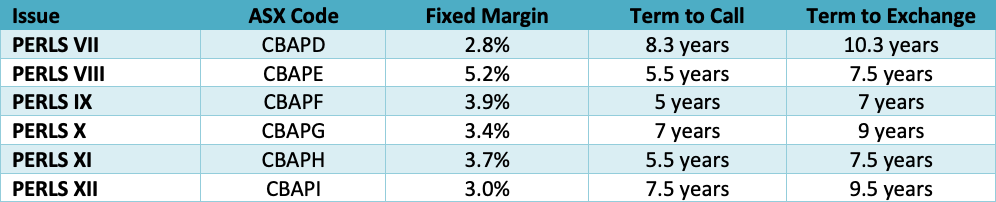

Historically, major bank hybrid securities (Capital Notes) have been issued at a fixed margin of between 3.0% and 5.0%. It has been a little bit higher and a little bit lower, but either strong investor demand or new supply from other banks has brought the margin back into the range. The table below shows the outstanding issues from CommBank, which are called CommBank PERLS Capital Notes or PERLS for short. The 7th issue from September 2014 was issued with a margin of 2.8%, the eighth from March 2016 at a margin of 5.2%, and the last four issues (3/17, 3/18,12/18 and 11/19) were in the 3’s.

In the new issue market right now with securityholder and public offers are two issues paying in the high 2’s. Macquarie Bank Capital Notes 2 are offering a margin of 2.90%, while NAB Capital Notes 4 are paying 2.95%. Launched a few weeks ago before the market got really worried about the impact of the Coronavirus, both these offers are open and were still accepting monies last night.

If you were thinking about investing in either of these issues, don’t. You can do seriously better by buying existing issues (such as any of the PERLS issues above) on the ASX.

Margins have blown out to around 4.5%. Driving this are three main factors. Firstly, the inevitable “flight to security” that happens when share markets get distressed. This sees investors drive the yields down on the highest “quality” debt securities (government treasury bonds), where “quality” is defined as the capacity to repay, and the yields go up on the lowest “quality“ securities. Effectively, the spread between the best and the worst widens.

And there is logic in this, because if the economy is going to slow down, businesses are going to suffer and loan defaults will increase. Underlying this is an assumption that the US Government or the Australian Government won’t default.

Banks are particularly vulnerable because they will see the impact of businesses in trouble through potentially higher bad debts. So, hybrid securities effectively get hit twice – firstly because they are lower rated securities and get caught out by the general movement in spreads, and then because they are issued by banks.

A third factor, which is probably more pertinent to retail investors, is that because bank ordinary shares have been sold off, potential bank dividend yields rise. To maintain relativity, hybrid securities need to come down in price and cheapen to remain attractive.

To be clear, I am not making the case that margins have peaked – if the Coronavirus situation deteriorates or the oil dispute between the Saudis and the Russians isn’t settled, margins could well move even higher. What I am saying is that by recent historical standards, the current margins on the ASX are attractive.

And this comes at a time when our major banks have never been better capitalised. They are “unquestionably strong” (the APRA benchmark).

Don’t invest in something you don’t understand

As the old adage goes, don’t invest in something you don’t understand”. Hybrid securities are complex investments. If a bank got into financial distress or there was a banking crisis in Australia, investors could potentially lose most if not all of their capital. So, it is important to understand the risks of investing and how these securities work. ASIC’s MoneySmart website provides some useful tutorials - see https://www.moneysmart.gov.au/investing/complex-investments/hybrid-securities-and-notes.