4 July 2025

1300 794 893

One of the more interesting aspects of the share market is the performance of the “rotation trade” stocks. These are companies that were big beneficiaries of the pandemic and lockdowns, but are now perceived to be “losers” as the market looks forward to vaccines and a return to a pre Covid-19 “normal”.

Zoom and Netflix are two of the best known examples, although I don’t think too many people will be in a hurry to cancel their Netflix subscription and “zooming” is now part of the lexicon. But growth rates should slow.

In Australia, “losers” include Woolworths and Coles, online retailers such as Kogan.com and non-clothes specialty retailers. Wesfarmers with its Bunnings franchises, as well as Harvey Norman and JB Hi-Fi, have also been tarred with this brush.

This month, the stockmarket is up a stunning 12.8%, closing yesterday at a post Covid-19 high of 6683. However, Australia’s best retailer, JB Hi-Fi, is down 4.3% over the same period. Is the market right to think that things are going to get much harder for JB Hi-Fi, or is this an example of “momentum trading” creating a buying opportunity for value investors?

The JB Hi-Fi story

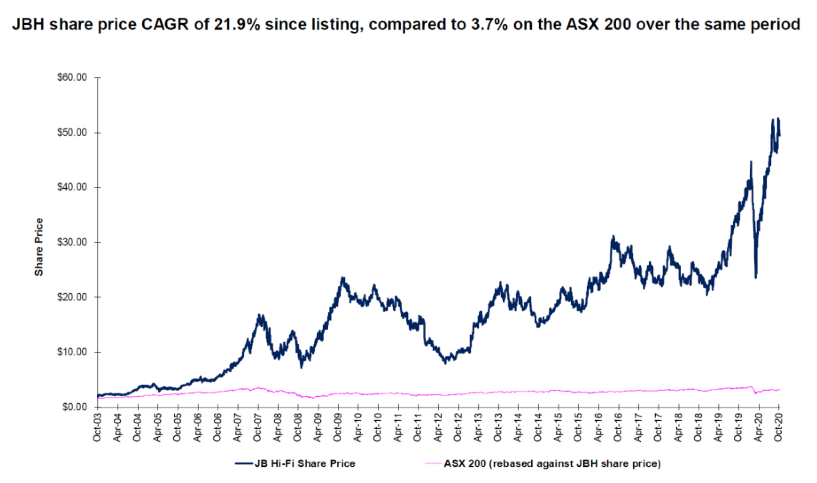

JB Hi-Fi is one of my favourite stocks. I just love graphs like the one below that shows year in, year out increases in sales, profitability and earnings per share.

And for shareholders, massive and consistent outperformance compared to the rest of the market. In JB Hi-Fi’s case, going all the way back to its listing in 2003.

Under the leadership of CEO Richard Murray, I have no doubt that JB Hi-Fi is Australia’s best listed retailer.

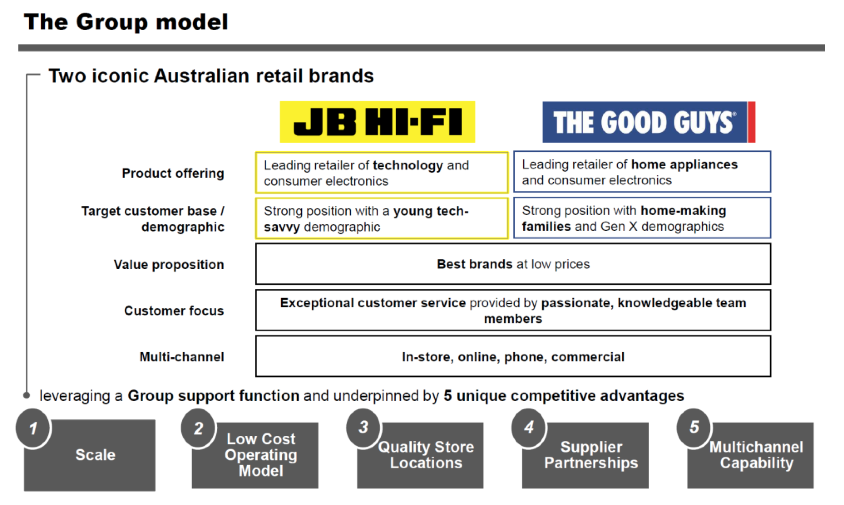

The JB Hi-Fi strategy is pretty simple. Two leading retail brands: JB Hi-Fi with a focus on technology and consumer electronics; and The Good Guys with a focus on home appliances and consumer electronics. The former targeting a young tech savvy demographic, the latter home-making families and Gen-X. A value proposition of “the best brands at low prices”, supported by exceptional customer service across multiple channel (in-store, online, phone and commercial).

Underpinning this approach is what the Group sees as its competitive advantages: scale, low cost operating model, quality store locations, strong supplier partnerships and multi-channel capabilities.

In FY20, total group sales rose by 11.6% to $7.9bn. JB Hi-Fi Australia grew comparable store sales by 12.2%. Sales momentum was strong through the year and accelerated in the fourth quarter as customers spent more time working, learning and seeking entertainment at home. Comparable store sales for the Good Guys grew by 10.8%.

Despite additional operating costs, the increase in sales allowed JB Hi-Fi to improve its net margin, with EBIT as a proportion of sales increasing from 5.25% to 6.14%. Underlying NPAT increased by 33.2% to $332.7m, and dividends increased by 33.1% to 189 cents per share.

Buoyant trading conditions continued into the first quarter of FY21, with JB Hi-Fi Australia reporting comparable stores sales growth of 27.7% (compared to the same quarter in FY20). The Good Guys did even better, with sales on a comparable stores basis up 30.9%.

At its AGM on 29 October, Richard Murray said that “he was pleased to report very strong sales growth”, notwithstanding that this period covered the Victorian lockdowns and the temporary closure of JB Hi-Fi’s metropolitan Melbourne stores. He went on to say that “while the Group is pleased with its start to FY21, due to the uncertainty arising from Covid-19, the Group does not consider it appropriate to provide FY21 guidance”.

What do the brokers say

Each of the major brokers is “neutral” on JB Hi-Fi. According to FN Arena, they see limited upside with a consensus target price of $47.95, about 5.6% higher than yesterday’s closing price of $45.39. Credit Suisse tops the range with target price with $50..62, while Morgans is the most bearish with a target of $41.40.

Most see growth moderating as consumer behaviour returns to normal. UBS warns that the market may not be pricing in the risk of “pull-forward” expenditure by consumers. Morgans says that “it continues to think Christmas will be a boomer and first half results will show extraordinary growth with strong operating expense leverage on buoyant top-line trading. However, it considers that the market will likely look through this strength”.

The brokers forecast earnings per share to increase moderately in FY21 to 314.2c, before decreasing by 17.1% in FY22 to 256.3c (underlying EPS in FY20 was 289.6c). This places JBH on a price earnings multiple of 14.4x forecast FY21 earnings and 17.7x forecast FY22 earnings.

For shareholders, a fully franked dividend of 208 cents is forecast for FY21 (current yield of 4.6%) and for FY22, 172 cents (current yield of 3.8%.).

My view

There is no doubt that sales growth is going to moderate. The questions are how long will it take for consumers to redirect their spend to pre Covid-19 levels, and whether during the Covid period, JB Hi-Fi has enjoyed market share and/or category share gains.

Record low interest rates are driving the housing market and this should be boon for The Good Guys, which is targeting “home-making families” The demand for consumer electronics and the latest gadgets/peripherals/media have strong tailwinds.

JB Hi-Fi is a class retailer. It has fought off the “Amazon challenge”, the “Covid-19 challenge” and a rapidly changing dynamic in terms of consumer preferences for digital media, games, entertainment and electronics. It has been both resilient and adaptive.

Trading on a forward multiple of 17.7 times, it is not overly pricey. The dividend yield of 3.8% is attractive.

Technically, JB Hi-Fi is a little on the nose with some chartists saying the short term trend is down. However, the long term trend is still up and for investors, I think the question is not “if”, but rather, “when”? Dips are the opportunities to buy quality stocks and this “rotation dip” is moving JB Hi-Fi into the buy zone.