3 July 2025

1300 794 893

The end of the financial year is just around the corner. Here are 5 end-of-year actions to make sure you get the most out of the super system.

1. Concessional contributions

Can you make additional concessional contributions to super?

Concessional contributions include your employer’s 9.5%, salary sacrifice contributions and any amount you claim as a personal tax deduction. (You no longer need to be self-employed to claim the tax deduction). Your concessional contributions cannot exceed $25,000 in aggregate.

The normal age rules apply. Up to age 67, anyone can make a contribution. If you are between 67 and 74 years, you must pass the ‘work test’, which is defined as working 40 hours over any period of 30 consecutive days. If you are 75 or over, only mandated employer contributions (the compulsory 9.5%) can be made.

2. Non-concessional contributions

Can you make additional personal (after tax) contributions?

The cap on non-concessional contributions is $100,0000. Up to age 67, anyone can make a non-concessional contribution provided their total superannuation balance on 30 June 2020 was less than $1,600,000. If you are between 67 and 74 years, you must also pass the ‘work test’.

You may be able access the ‘bring forward rule’, which allows up to 3 years’ worth of contributions in one year. Potentially, you could contribute $300,000 in one hit and a couple could put a combined $600,000 into super. The age limit for this is different - you must have been aged 64 years or less on 1 July 20 and not have accessed it in the preceding two years.

Super balances are measured each June 30 (i.e. your balance on 30 June 20 determines whether you can make non-concessional contributions in 2020/21) and include all amounts in accumulation and pension. If your total super balance was between $1,400,000 and $1,500,000 then the maximum amount you can access under the bring-forward rule is $200,000, and if your balance is between $1,500,000 and $1,6000,000, you are limited to $100,000. Above $1,600,000, you can’t make any non-concessional contributions.

3. Government Co-Contribution

Can you access, or can a family member, access the Government Co-Contribution? If eligible, the Government will contribute up to $500 if a personal super contribution of $1,000 is made.

The Government matches a personal contribution on a 50% basis. This means that for each dollar of personal contribution, the Government makes a co-contribution of $0.50, up to an overall maximum of $500.

To be eligible, there are 3 tests. The person’s total income must be under $39,837 (it starts to phase out from this level, cutting out completely at $54,837), they must be under 71 at the end of the year, and critically, at least 10% of this income must be earned from an employment source.

While you may not qualify for the co-contribution, this can be a great way to boost a spouse’s super or even an adult child. For example, if your kids are university students and doing some part time work, you could potentially make a personal contribution of $1,000 on their behalf – and the Government will chip in $500!

4. Tax offset for spousal contributions

Can you claim a tax offset for super contributions on behalf of your spouse? If you have a spouse who earns less than $37,000 and you make a spouse super contribution of $3,000, you can claim a personal tax offset of 18% of the contribution, up to a maximum of $540.

The tax offset phases out when your spouse earns $40,000 or more. Your spouse’s income includes their assessable income, reportable fringe benefits and any (though unlikely) reportable employer super contributions. One additional eligibility test – your spouse’s total super balance on 30 June 2020 was less than $1,600,000.

5. Pension payments

Finally, if you are taking an account-based pension, have you been paid enough? The Government requires that you take at least the minimum payment, otherwise your fund will potentially be taxed at 15% on its investment earnings, rather than the special rate of 0% that applies to assets that are supporting the payment of a super pension.

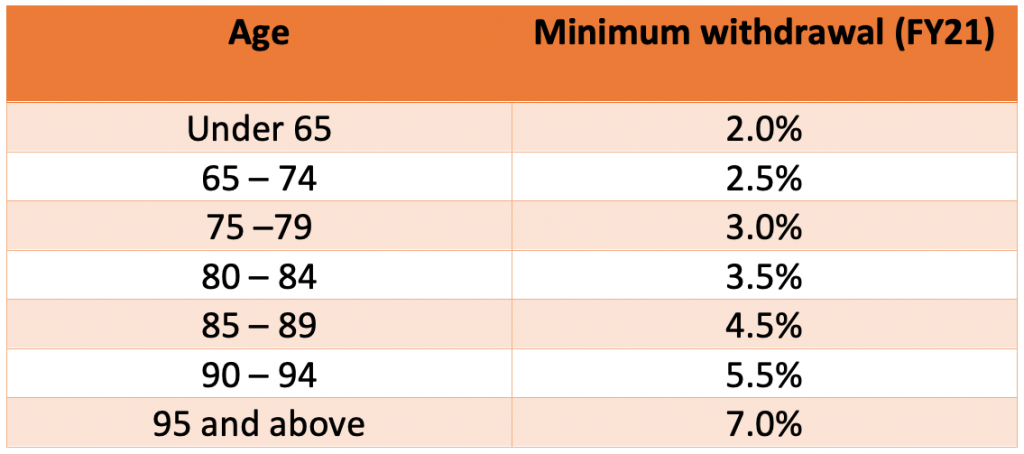

The minimum payment is based on your age, and calculated on the balance of your super assets at the start of the financial year (1 July). To assist retirees following the Covid-19 pandemic, the Government has reduced the minimum annual payment required by 50% for the 2019-20, 2020-21 and 2021-22 financial years. The factors to apply this year are shown below:

For example, if you were aged 66 on 1 July 2020 and had an account balance of $1,000,000, your minimum payment is 2.5% of $1,000,000 or $25,000. You can take your pension at any time or in any amount(s), but your aggregate drawdown over the year must exceed the minimum amount. If you commenced a pension mid-year, the minimum amount is pro-rated according to the number of days remaining until the end of the financial year.

Don’t leave it to the last minute

Super contributions must be receipted and banked by your SMSF or super fund on or before 30 June. If paying by BPay, electronic funds transfer or even cheque, please allow sufficient processing time.