You couldn’t turn your head yesterday without seeing the PM or one of his many MPs spruiking the launch of the new Home Guarantee Scheme. It allows first-home buyers to leapfrog the tricky 10-20% deposit normally required in favour of just a 5% deposit. But buyer beware: you’ll end up paying far more in the long run.

How does the government’s 5% deposit Home Guarantee Scheme work?

Buying a home instead of renting a home is the great Australian dream. And it’s one that Millennials and Gen Z have been locked out of for some time as the price of property skyrockets compared to the average take home wage around the country (see below if you don’t believe me).

The Australian government’s Home Guarantee Scheme is designed to help these first-homebuyers get into the market sooner.

Under the scheme, eligible buyers can purchase a home with as little as a 5% deposit, instead of the typical 20% lenders usually require. The government acts as a guarantor for up to 15% of the loan, which means buyers can avoid paying costly lenders mortgage insurance.

The scheme has several streams, including support for single parents and regional buyers, but the core aim is the same: making it easier for people to buy their first home without needing to save a huge deposit.

There are caps on property prices and income limits for applicants, so not everyone will qualify. But for those who do, the scheme can reduce the time it takes to get into a home, giving a leg up to people who might otherwise be locked out of the market.

The scheme was officially launched by all and sundry from the Labor government, from PM Albanese on down. (For what it’s worth, Albo did concede that this scheme would in fact push up house prices as demand increased but let’s leave that one there for now, shall we?)

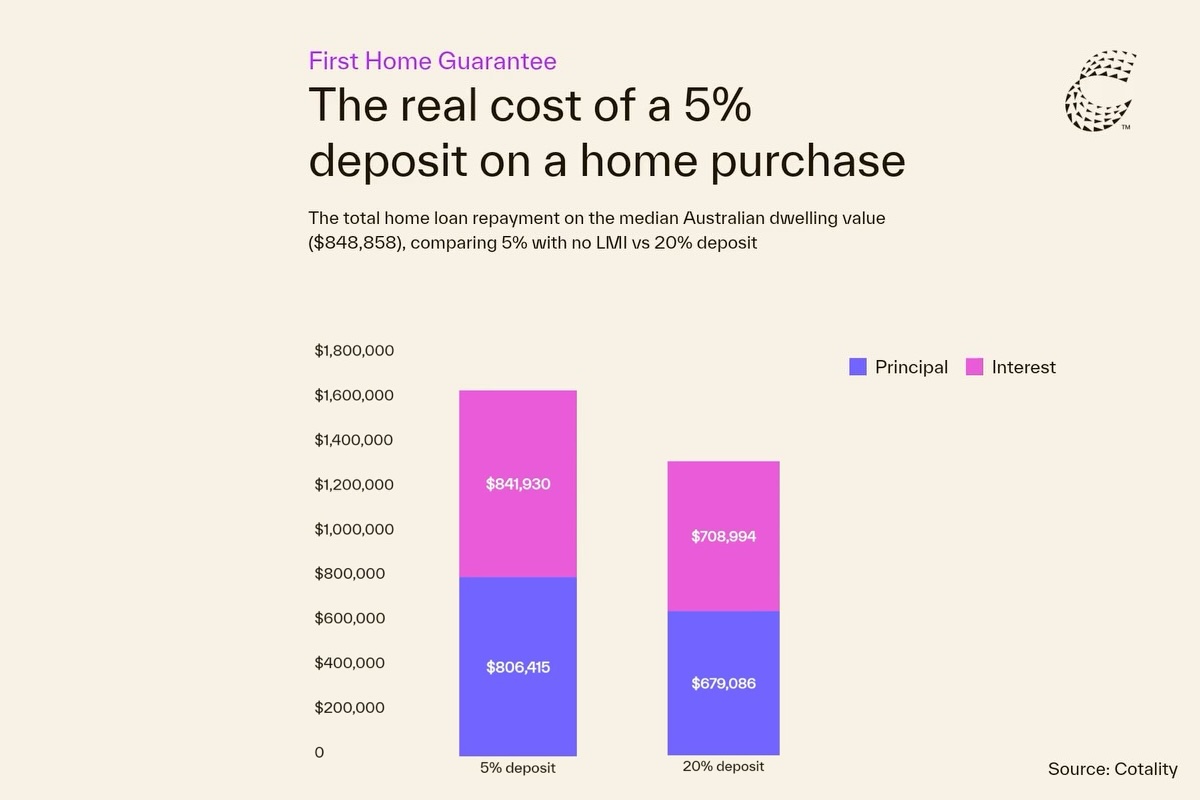

The real cost of a 5% deposit

It all sounds great if you’re in your mid-20s and still living with your parents, right? However, the real cost, as usual, is hidden in the details.

This quick little graphic from Cotality—formerly CoreLogic—tells the story of the lifetime of a loan.

As Eliza Owen, friend of Switzer Investing TV and Cotality’s Head of Research, explains, first home guarantee schemes can make buying more accessible, but they do come with a price tag.

“The main cost for individuals is extra interest paid over the life of a loan,” Owen says.

A 5% deposit means taking on a 95% loan-to-value ratio. That extra debt adds up, and over a 30-year loan, “the extra interest costs can be tens-of-thousands, or hundreds-of-thousands more expensive than a 20% deposit home loan.”

But for many buyers, the trade-off might still make sense—especially for renters in high-priced markets. Getting into a home sooner can mean less money spent on rent and the chance to ride any future market upswing. In Sydney, for example, Owen estimates that a 5% deposit could shave more than 12 years off the time needed to save for a typical home and avoid around $500,000 in rent.

Still, as Owen notes, the calculations “should be taken as more illustrative than advice.” Not everyone’s situation is the same.

For those who aren’t paying rent, it could make more sense to wait and save a larger deposit, which also means paying less interest and avoiding lenders mortgage insurance altogether. For others, the ability to buy sooner may outweigh the extra costs (especially to your mental health if you’re stuck living with your folks).