We’ve spent the last few weeks craning our necks to look up at the CBA share price, which has set and reset its all-time record a few times now. Today’s trading update from CEO Matt Comyn answers the question: can the CBA share price go any higher? You betcha.

By the numbers

Commonwealth Bank booked an unaudited cash net profit of $2.6 billion for the three months to 31 March 2025, effectively flat on the December‑quarter result and bang on the $2.57 billion quarterly average achieved in 1H25. Statutory profit matched cash profit at $2.6 billion.

Group operating income crept 1 % higher quarter‑on‑quarter, keeping it marginally ahead of the first‑half run‑rate. Meanwhile, underlying net‑interest margin (NIM) remained stable.

Operating expenses also rose 1 %. CEO Matt Comyn points to higher tech and cybersecurity spend and more frontline staff driving the increase. CBA reveals it has offset this number slightly, however, shaving $60 million off the top thanks to productivity programs.

Rising arrears, tricky margins

CEO Matt Comyn delivered his commentary alongside the results, saying – like all bank CEOs who have reported in the previous week – that our economy is facing some rough seas.

“We know it has been another challenging period for many Australian households and businesses dealing with cost‑of‑living pressures. We have remained focused on proactively engaging with our customers on a range of support options to help those who need it most,” he said in his accompanying statement. And from the looks of CBA’s numbers, there are more customers in need of “a range of support options” than in previous quarters.

Home loan arrears are up 5 basis points quarter-on-quarter to 0.71 %, meanwhile personal loan arrears are up 19 basis points. CBA has reported a loan-impairment expense of $223 million for this quarter.

Rising arrears serve as a bit of a “check engine” light for not only CBA but also for the economy. With more and more borrowers struggling to make their repayments despite Australia entering potential rate-cut territory, it’s a sign that we’re not out of the woods yet. Plus, for CBA, it puts a minor dent in what is otherwise another astronomical profit figure and could make the cost of funding a tricky conversation going forward.

The economy continues to show signs of recovery, however. Inflation is falling, unemployment and underemployment rates of 4% and 5.9% are steady and, as mentioned, we’re on the precipice of yet another interest rate cut if the economic data from this week breaks our way.

And these numbers aren’t out of left field for Comyn, at least. The CBA CEO flagged risks in the credit cycle in particular back in his February 2025 update to the market. But just because the risks are arising exactly where Matt-stredamus predicted doesn’t mean it’s completely safe. Now we just have to watch to see if these issues become a growing concern for the bank (and the economy).

Elsewhere, CBA – like all banks reporting in the last week – is being hawkish on its margins.

CBA’s net‑interest margin (NIM) still appears stable from headline results, but commentary reveals that the engine powering it is under some strain. The 1 % lift in net‑interest income for the quarter came from loan growth and a bigger boost from the replicating portfolio and equity hedge, yet those gains were “largely offset by deposit competition”.

This matches similar commentary from Westpac and NAB last week, which are also observing margin pressure in their businesses.

Money printer go brrrrr

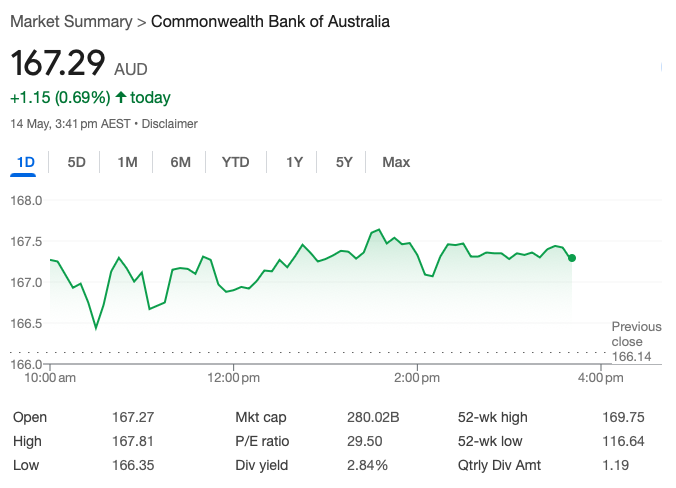

CBA is still trading at a whopping $167 a share at the close the Wednesday session. That’s up almost three-quarters of a percent higher than its previous day close of 167.27. It’s also hovering just below its record $169.75 intraday high set on 2 May.

Even if it’s not yet another record broken, it shows that CBA can still go higher, even when highlighting risks in its business.

On last week’s episode of Switzer Investing TV, guests including Grady Wulff of Bell Direct and Chris Haynes of Equity Trustees called out both the flight to safety that has pushed CBA to these massive share highs, as well as the inherent risks at the same time.

Haynes, Head of Equity at Equity Trustees, called it out explicitly on the show:

“We’ve had this flight to the banks in recent times thinking they’re perfectly safe… but the margin pressure is real” he said adding that investors are buying “the best house in the street and don’t care what they pay for it.”

“I think we may have just seen a little bit of a turning point in this result for all banks. There’ll be no earnings growth going forward…you’re paying a lot for nothing.”

And indeed, Haynes predictions are also coming to pass, with CBA’s latest quarterly numbers showing a slight lack of yeast. Today’s update from CBA shows a plateauing of profit if measured against the 1H 2025 average.

Regardless, people are still in a buying mood when it comes to CBA. Trading volume for the “best house on the street” spiked right before the close of the session today on the ASX.