4 July 2025

1300 794 893

The coronavirus, followed by the nascent oil price war, has been the largest shock that the most expensive equity markets since the Great Depression and lowest yielding bond markets in history has received.

By the reactions of governments with stimulus packages already announced in the US and Australia, and the actions of central banks, we can see how seriously this issue is being taken.

What do bond holders do?

As usual, we focus on the fundamentals of the credit position of the bonds we hold. Remember that the base case for every bond investment is that you should be comfortable holding to maturity in the event you need to do so.

With markets presently dislocated, this is a true test of that philosophy as investors assess their portfolio exposure.

This will require mental fortitude, as market prices can be far removed from the fundamental reality of the credit condition of the issuer.

Investment grade bonds

These continue to offer security of income despite the market volatility. We would be very confident that all investment grade bonds will pay their coupons as and when they fall due.

In particular, Australian issued investment grade bonds have a superior track record to those issued internationally, with only three defaults recorded in the last 30 years. Take comfort from this track record as we would say it is likely to be repeated, given the conservatism of the local lending market.

Locally issued RMBS also fall into this bucket, with no losses ever being recorded on a rated note, including sub investment grade. Please note this does not mean that market prices cannot move sharply, but you should have confidence in the underlying collateral.

Despite primary markets currently being quite inactive due to the volatility, we would expect that a strong investment grade issuer would be able to issue bonds, even if they would be paying a higher level to do so in the current environment.

This offers opportunity – long-term FIIG clients would recall in late 2013 when Qantas was downgraded from investment grade and then subsequently issued two new bonds at yields of 7.50% and 7.75%, which rapidly appreciated as Qantas restored their investment grade rating.

We are always on the lookout for these types of opportunities although we think we are still a little early in this cycle. We have seen some large businesses recently downgraded such as Kraft-Heinz and expect some more to follow, although they are not yet in the buy zone.

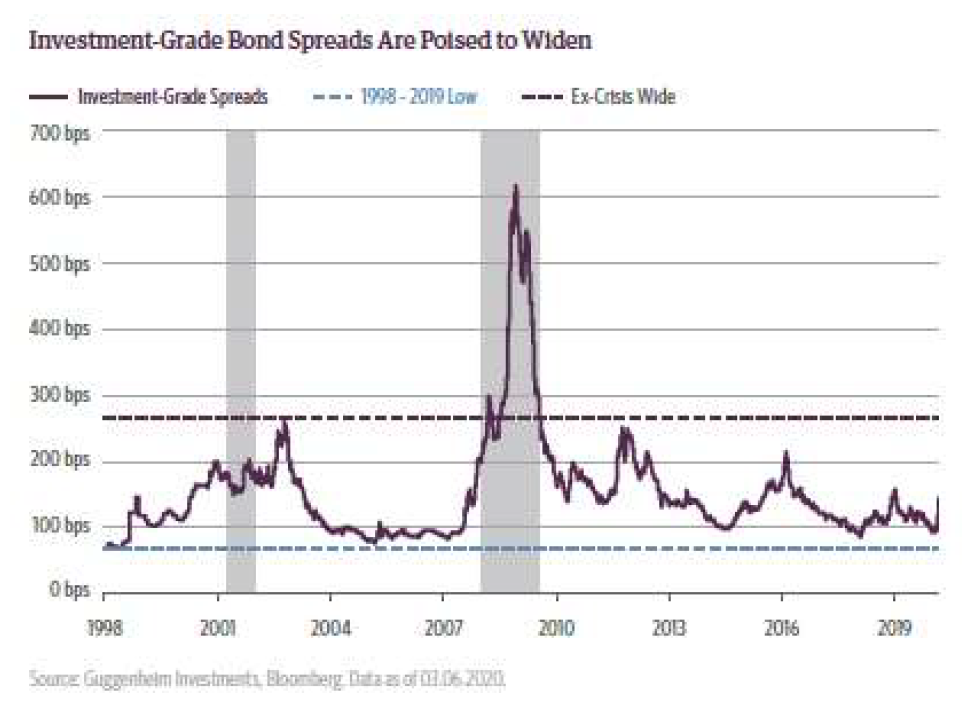

We have seen investment grade spreads widen a little in the last couple of weeks, albeit off historically low levels. This could continue, but again we reiterate the confidence you should have in the issuers of those bonds being able to meet their obligations.

High yield bonds

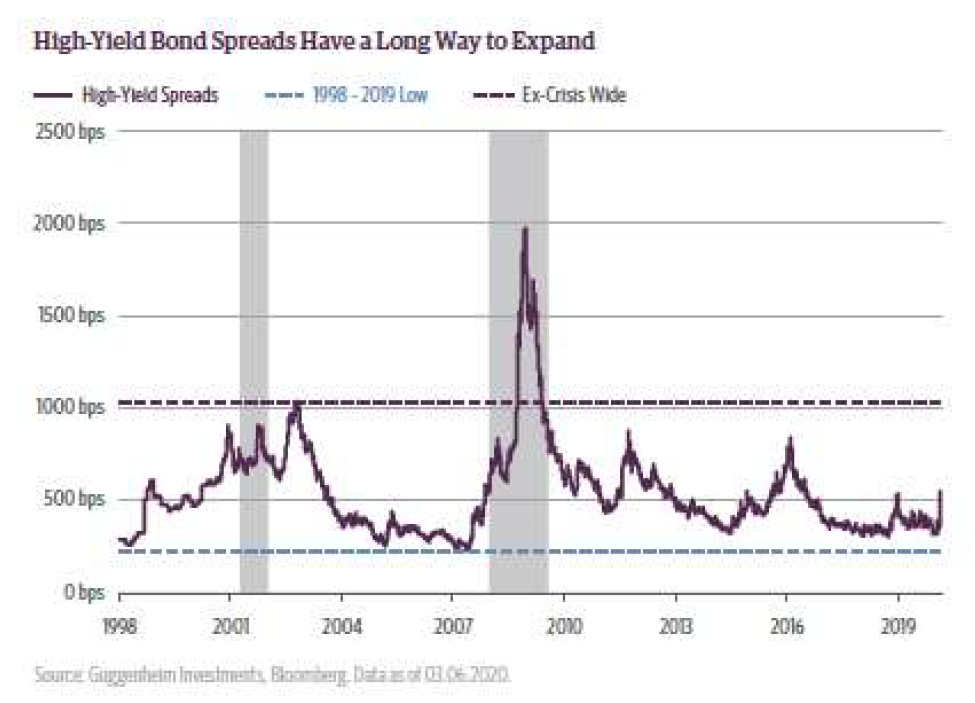

As detailed towards the end of this piece, the energy sector has driven high yield bond spreads to widen, however we are still at low levels compared to recent history (note the scale compared to the Investment grade chart):

This is again likely to continue if general economic conditions deteriorate, and as such we can expect further softening in prices.

Again, we come back to the fundamental credit proposition. Our Research team is closely monitoring the credits clients hold and are reviewing their fundamentals.

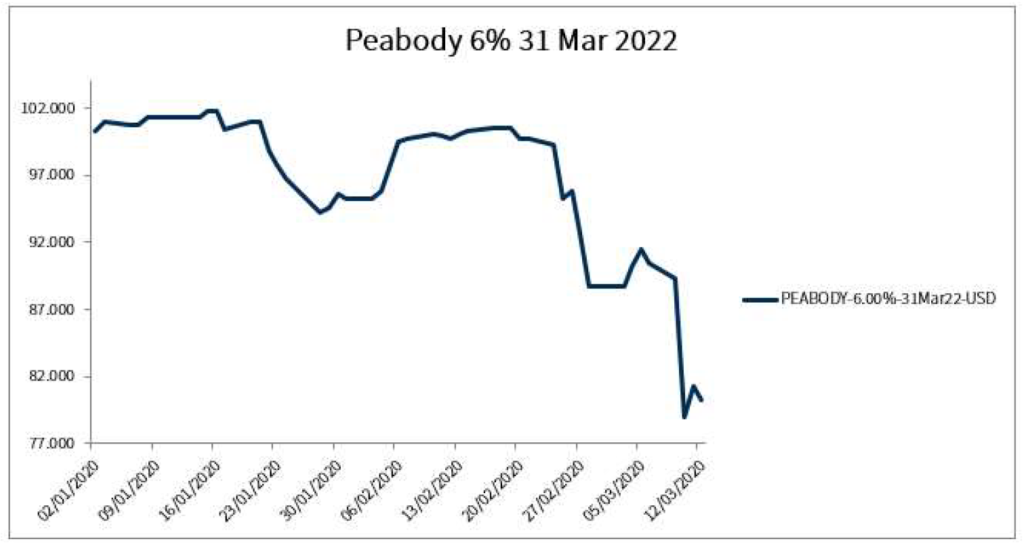

In this space the volatility can be extreme – take the Peabody 2022 senior secured bonds as an example:

Fundamentally nothing has changed for this company in the last month, as it mainly supplies coal for electricity production domestically in the US, and yet the bond price has fallen by >20%. The company in its latest results stated it had $750m in cash on balance sheet and >$1bn of available liquidity via bank facilities, with free cash flow expected to be break even or slightly positive over the next 2 years.

This gives us a high level of confidence they will have the ability to repay the bonds, and yet they are trading at a yield of >20% to the short, 2 year maturity.

Clearly, there is a level of risk involved, but it is not likely represented by the yield on offer.

Conclusion

In our opinion there are likely to be further falls in risk markets, and dislocation in liquidity, i.e. trading may become tricky at times. It is not known for how long this may last, but until we see some of the main indicators, such as the VIX, return to more normalised levels, we should brace ourselves to hold tight through these times and not look to panic.

Fundamentally we are invested in an asset class that has a payment obligation on a maturity date in the future when investors can expect to be repaid, regardless of market conditions. Clearly this expectation is tempered by the level of credit risk being taken in individual bonds, but the principle holds none the less.

Opportunities to buy assets at levels that do not reflect the fundamental risk are also likely to come up (as above) and may do so with short timeframes for execution.

Eventually the virus situation and the oil markets will normalise and while not excusing the human cost of the virus, businesses, markets and economies will return to normal, although that ‘normal’ may look different to where we are now.

As this eventuates, and the time period for this we suspect may be longer than currently anticipated, long-term stable holders of quality fixed income will be rewarded for their patience in holding out through the volatility, and if opportunities were taken to capitalise on dislocations, may come out significantly ahead.

If investors are comfortable with the level of income available at current prices on an investment grade bond, then they should be happy buying it today, ignoring price volatility and receiving the income until you are repaid at maturity.