6 July 2025

1300 794 893

This time last week the ASX200 was up nearly 4% over five days, following the RBA’s surprise decision to increase rates by ‘just’ 0.25%. Global markets took heart from the decision, believing a pivot toward slower and smaller rate increases may be in store, but Friday night’s strong jobs data in the US – featuring an unemployment rate of just 3.5% (even though the participation rate fell slightly), dashed those hopes. Since then the ASX200 has fallen 2.5%, having fallen heavily on Monday morning following Wall Street’s lead, and barely moving since. All eyes are on US CPI figures this week; volumes remain subdued and most investors are awaiting significant price action before considering changes to their holdings.

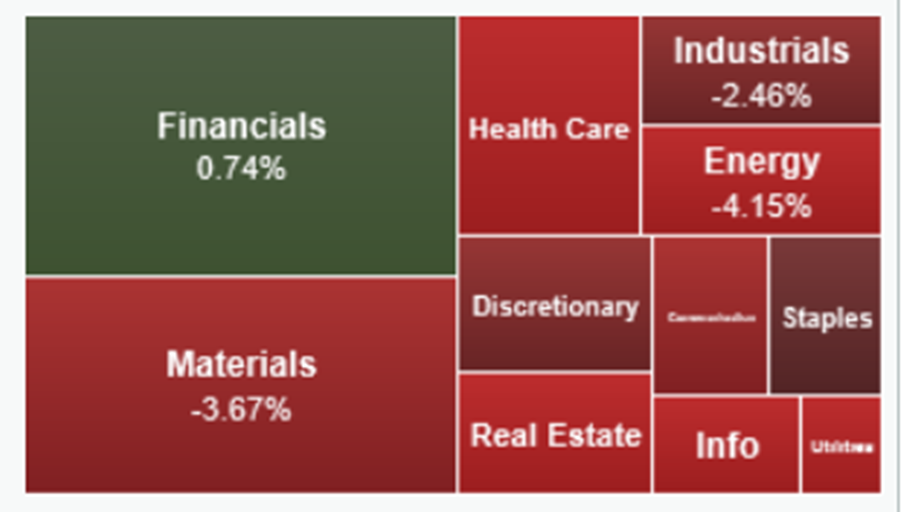

The only sector to record green this week was financials, with energy and material leading the losses. As nabtrade investors are broadly holding a lot of exposure to the big four banks, much of it bought during the Covid downturn at significant discounts to today’s price, many have taken the opportunity to trim their positions. Nab (NAB) was a huge sell on Thursday, followed by Westpac (WBC) and then Commonwealth Bank (CBA). Given their overweight positions, this is mostly trimming rather than exiting positions overall.

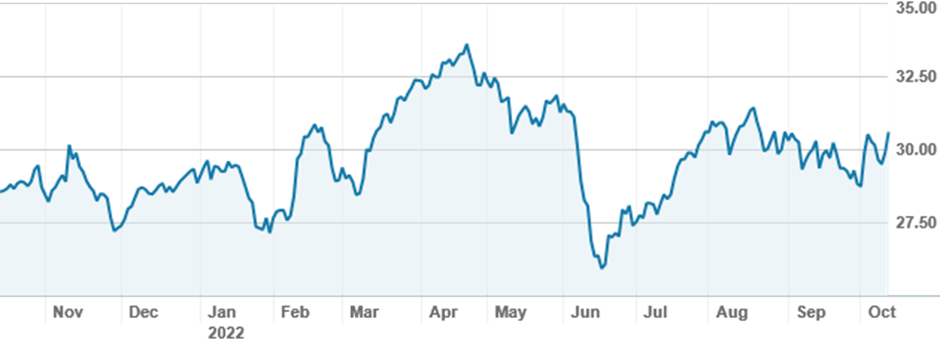

Nab share price over twelve months (NAB)

The other huge sell on Thursday was Qantas (QAN), which rose 8.7% on a market update that included a more rapid return to profitability and confidence in the company’s ability to pass on the cost of higher fuel and other costs to travellers. Nabtrade holders, who were big buyers of Qantas in the early days of the pandemic, sold heavily.

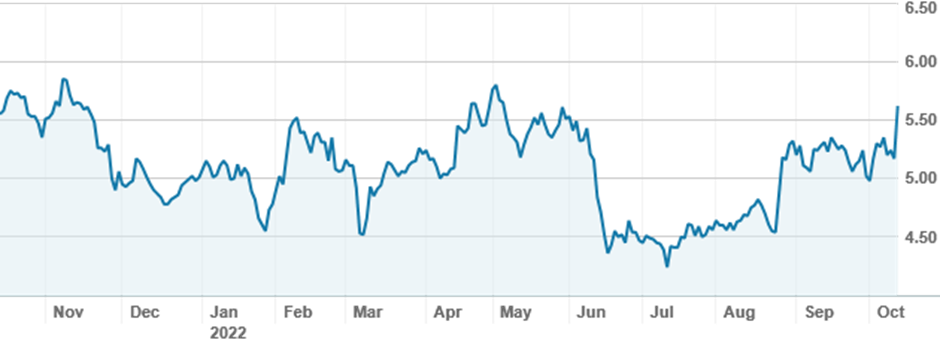

Qantas shares over twelve months (QAN)

One other interesting sale was Global X (formerly ETF Securities) Physical Gold ETF (GOLD), which has seen quite a bit of selling. The listed fund holds physical gold bullion on behalf of investors, and has returned over 6% over the last month, and 10% over the last year. Several investors have bought this option to diversify their portfolios, but some are taking profits.

In materials, Fortescue Metals Group (FMG) has returned to the top of the table after a brief challenge from Pilbara Minerals (PLS). Core Lithium (CXO) and Allkem (AKE) remain red hot, with a general buying theme, although strong days will see traders trimming. Trade sizes are consistently large; generally smaller and younger investors have not been actively trading this sector.

A few small caps also captured attention this week. Dubber Corporation (DUB) fell more than 30% on a major revision of its FY22 results and the (not surprising) resignation of its CFO; the call recording SAAS company is down nearly 90% over twelve months. Baby Bunting (BBN) also disappointed the market, albeit in less spectacular fashion, after sharing lower Q1 margins. A small number of buyers came out to see if they could nab a bargain.

On international markets, the semiconductor space is attracting interest again. Nvidia (NVDA.US) has fallen more than 40% over twelve months, and continues to see mixed trading, while Intel (INTC.US) and Advanced Micro Devices (AMD.US) are also mixed. Some enthusiasts for the sector are trading directional semiconductor sector ETFs rather than attempting to pick a winner.

Nvidia shares over twelve months (NVDA.US)

BIOGRAPHY & DISCLAIMER FIELD

Analysis as at 13 October 2022. This information has been provided by WealthHub Securities Ltd the ASIC Market Integrity Rules and a wholly owned subsidiary of National Australia Bank Limited ABN 12 004 044 937 AFSL 230686 (NAB). Whilst all reasonable care has been taken by WealthHub Securities in reviewing this material, this content does not represent the view or opinions of WealthHub Securities. Any statements as to past performance do not represent future performance. Any advice contained in the Information has been prepared by WealthHub Securities without taking into account your objectives, financial situation or needs. Before acting on any such advice, we recommend that you consider whether it is appropriate for your circumstances.