12 July 2025

1300 794 893

US shares started the week strongly but higher bond yields following the US Federal Reserve’s meeting led US shares down 0.8% over the week on the S&P500 index. Australian shares were also down this week by 0.9%, led lower by materials, energy and industrials. The US dollar was up slightly this week and the $A ended the week around US $0.774.

US 10-year yields touched 1.75% this week (before settling back down to around 1.72% by the end of the week) but this only takes them back to early 2020 levels. While the recent run-up in global bond yields has been fast, the actual level of yields is not a concern, especially while US real yields are still negative which means that financial conditions are not tightening too fast. Oil prices fell this week to $64.5/barrel from $68/barrel from a range of issues – concern about rising Russian oil production with higher risk of US sanctions on Russia after Biden called Putin a “killer” and worries about lower oil demand from Europe from a slow vaccine rollout. Metals prices were mostly higher over the week while there was some pull back in agricultural commodities after some strong gains in recent months.

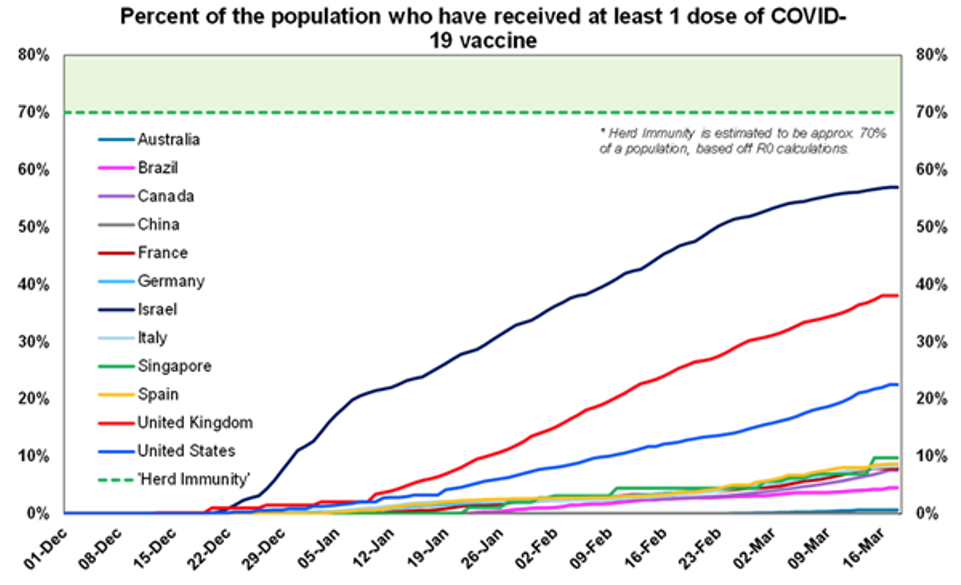

News of some European countries (Germany, France, Italy, Spain and Portugal amongst others) pausingAstraZeneca vaccinations temporarily because of concern that it causes blood clots didn’t spook markets because it seemed to be an overreaction with the European Medicines Agency (EMA) and the World Health Organisation saying the vaccine was still safe to use (although the EMA is still investigating the blood clot side effect). There were 18 cases of a “hard to treat” blood clot out of 20 million vaccines Germany, Italy and France have since resumed its AstraZeneca vaccinations programs. Europe is still well behind in vaccinating its population despite the very high number of cases having only vaccinated 8% of the population, compared to 57% in Israel, 38% in the UK and 23% in the US (see the chart below). (Also see Dr Ross Walker’s article on allergy, clots and vaccinations).

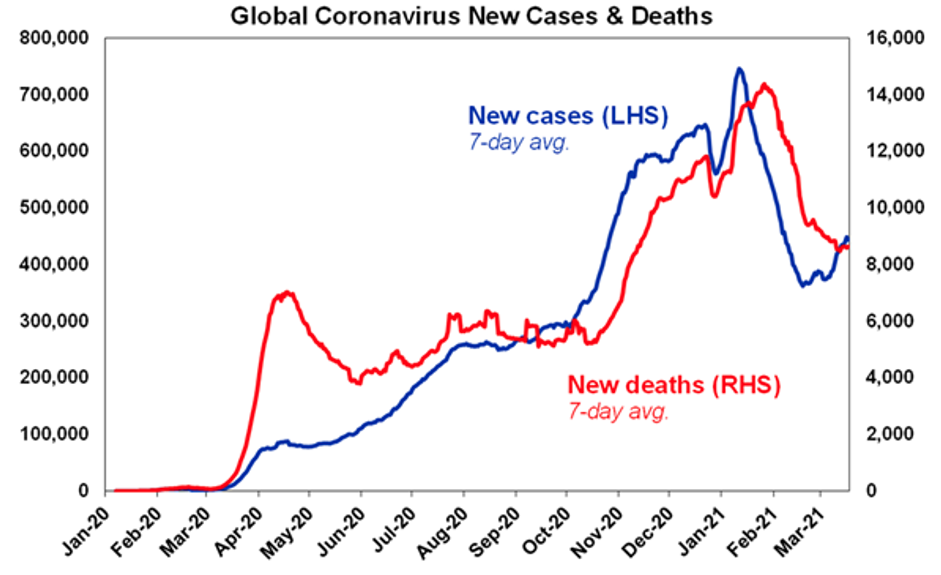

Global coronavirus caseshave crept back up a little again (see chart below), driven by higher cases in emerging markets. Developed countries cases have stabilised over February/March – a sign of lockdowns (especially in Europe) working (Paris is in a lockdown again for four weeks) and the vaccine rollout.

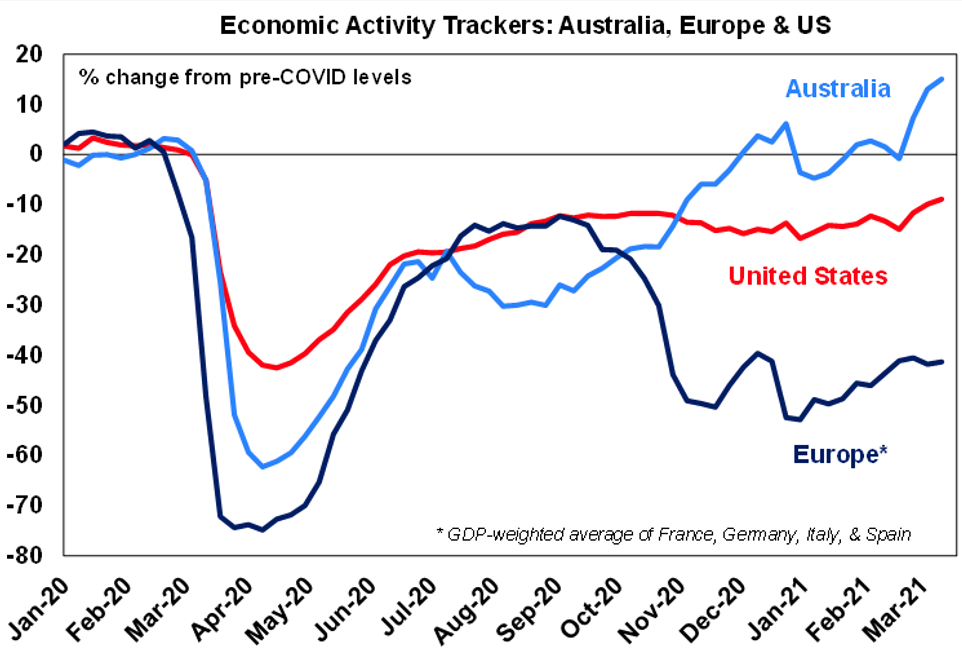

Our weekly Activity Trackerscontinue to improve for Australia and the US (see chart below), even once we start to take base effects into account which are starting to become evident in the data. Australian restaurant spending, hotel bookings and foot traffic are the biggest drivers of the lift higher. In the US, the improvement is broad based across indicators and especially in job ads, hotel bookings and mortgage applications. The Europe Activity Tracker is still tracking sideways as many countries are still operating with strict mobility restrictions in place.

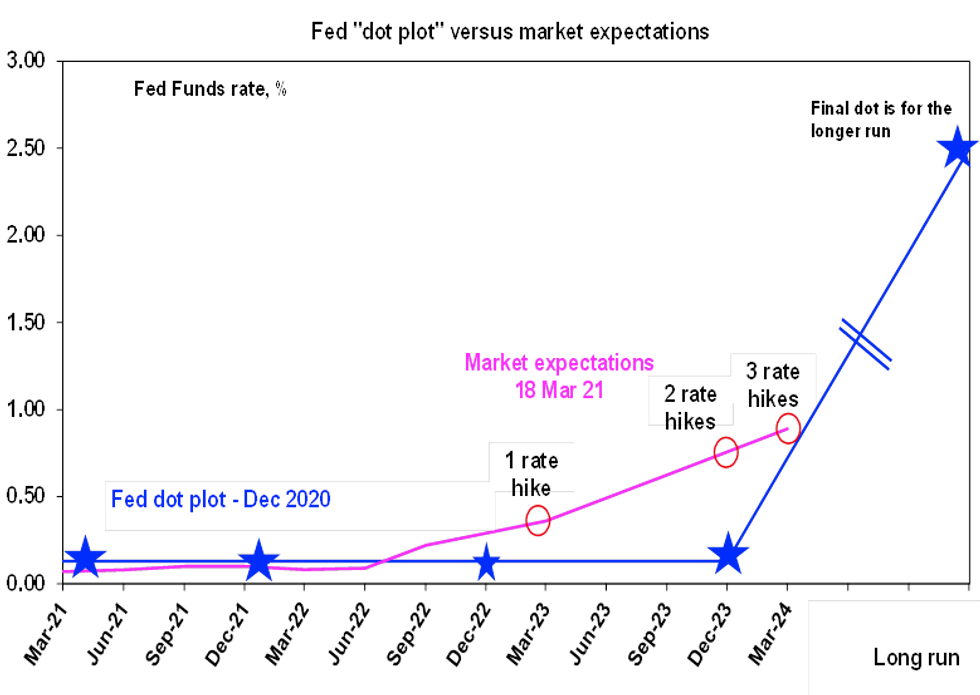

The Federal Reserve (“Fed”)meeting was highly anticipated this week given recent market fears that the Fed would have to taper its quantitative easing program if inflation spiked from the high level of US fiscal stimulus (which has totalled 12.7% in 2021 versus 7.8% in 2020). The Fed squashed any expectations of an early taper at this week’s meeting. The median Fed committee participant still sees no interest rate hikes until after 2023. This is much more dovish than market expectations which sees three rates by early 2024 (see chart below). Although, there were two more members of the Fed (out of 18) that expect rate hikes in 2023, up from 5 as at the December meeting. GDP forecasts for 2021 were revised up to 6.5% (from 4.2% in December) but on our forecasts GDP growth could easily be between 8-10% this year. Core inflation forecasts were also revised up, to 2.2% in 2021 (from 1.8% in December), 2.0% in 2022 and 2.1% in 2023 which shows that the Fed is not expecting a big inflation breakout and is willing to tolerate inflation above 2% for some time, in line with their new. average inflation targeting monetary policy regime (which allows for inflation overshoots and undershoots).

Clearly, the market is sceptical that the Fed will be able to keep interest rates at current levels for the next three years. We think that nominal bond yields can still shoot higher in the short-term towards 2% and above on inflation concerns, especially as annual inflation will push to 3‑4% per annum temporarily over the next few months because of base effects from 2020 and markets are likely to worry that this move is permanent, rather than temporary.

Something interesting to keep in mind – the latest Biden fiscal stimulus will distribute around $1.2trillion across the country over the next five months. In comparison, the Trump tax cuts of 2017 were worth $700bn over ten years. Of course, the US economy needs more support now because of the pandemic but this follows a very large stimulus package in 2020 and also comes at a time when the economy is re-opening. The level of US fiscal stimulus this year is extraordinary, especially considering that more is still likely this year.