9 July 2025

1300 794 893

Market sentiment was more cautious to start the week on concerns about the economic reopening from rising COVID-19 cases and vaccine delays. US shares on the S&P500 still managed to close the week 1.6% higher, with a rally towards the end of the week, while the heavier tech NASDAQ index was down by 0.6%. NASDAQ shares are now down by nearly 7% since a peak in mid February. Australian shares rose by 1.7% over the week, with all sectors rising except for information technology.

US 10-year bond yields have retreated slightly to 1.67% after last week’s peak at around 1.75%. The $US also continues to track higher and was up by 0.9% over the week. After the $US fell to a two year low early in 2021, it has rallied by around 4% on better US economic news and higher yields. We still expect the $US to weaken over 2021 on stronger global growth but in the short term it could appreciate further. The $A has been weakening as the $US has been rising, with the $A trading at US$.7637 at the end of the week, down from nearly US$0.80 in late February.

A 400 metre container ship stuck in the Suez Canal has caused havoc to trade routes in the area. Around 9% of global seaborne oil passes through the canal. Oil prices are getting supported by the supply disruptions created by the ship but are also under pressure from concerns around demand from a slower economic re‑opening. The oil price ended the week relatively unchanged at $64.57/barrel. Iron ore prices have also been weakening and are now at $US155/tonne, down from ~$US170 a few weeks ago, from faltering Chinese demand.

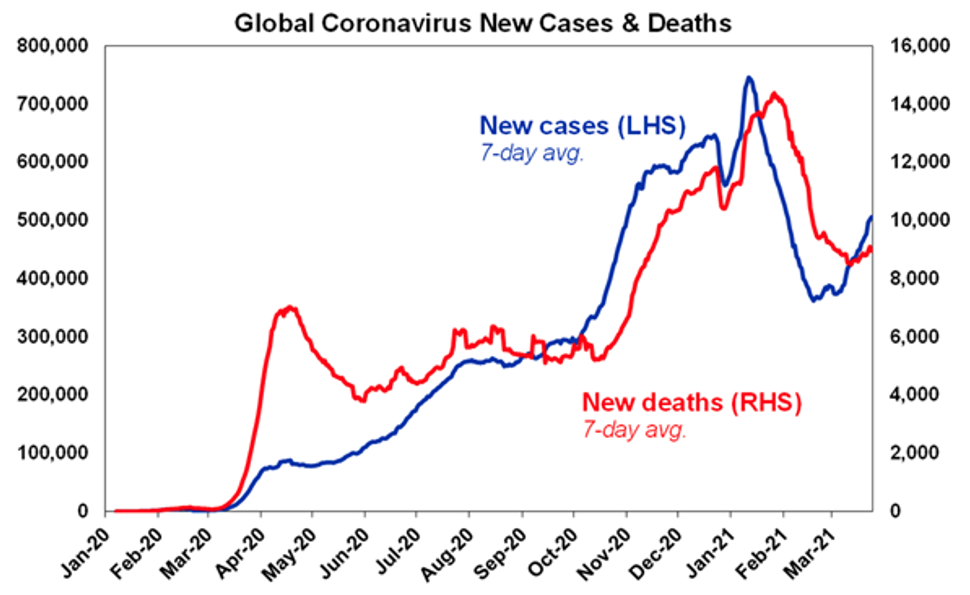

Global COVID-19 cases are trending higher again (see chart below) after some stabilisation in recent weeks.

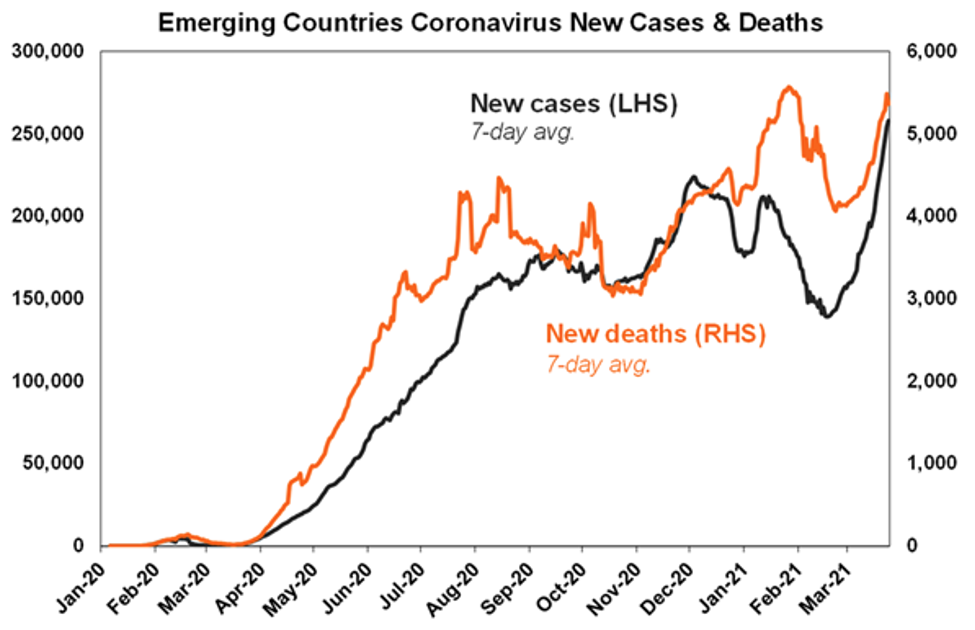

Cases in developed countries cases are still declining. Although Europe cases have started to pick up again particularly in Italy, Germany and France because of variant strains. Emerging countries cases are rising swiftly (see the chart below), getting close to their prior highs, with elevated numbers in Brazil, India, Turkey, Pakistan and Bangladesh.

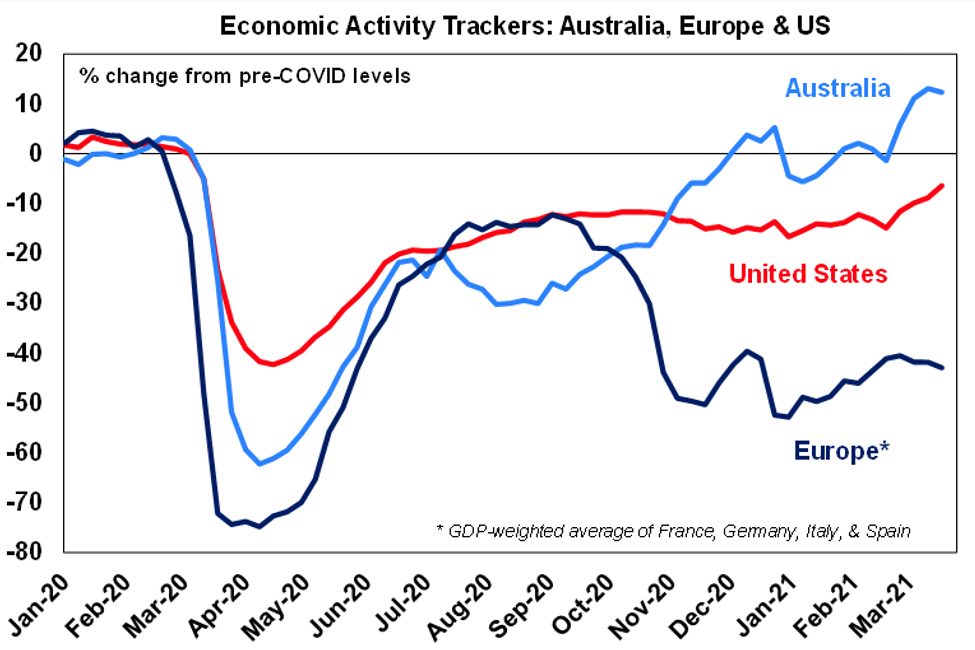

European vaccine rollout continues to be slow moving with the EU this week making comments that it could potentially block shipments of the AstraZeneca vaccine to countries outside of Europe (mainly targeting the UK) if the delivery targets for Europe were not first met. Strict mobility restrictions and the slow vaccine rollout continues to weigh on our European Activity Tracker, which has stepped down marginally again (see chart below) as some European countries have gone into another short lockdown. The US Activity Tracker picked up significantly this week on better confidence, mobility, restaurant bookings, hotel bookings and retail traffic. This is consistent with slowing US virus cases. The Australian Activity Tracker flat-lined this week but is still positive and showing that activity has recovered to pre-COVID levels.

In Australia, those of us in NSW are grateful for the better weather after a week of horrific rain, which also spread to some parts of Victoria and southern parts of Queensland and caused tens of thousands to be evacuated. The economic impact will show up in lower mobility data, some weakness in retail sales but is unlikely to be long lasting. Coal prices have been increasing from the supply disruptions in Newcastle.

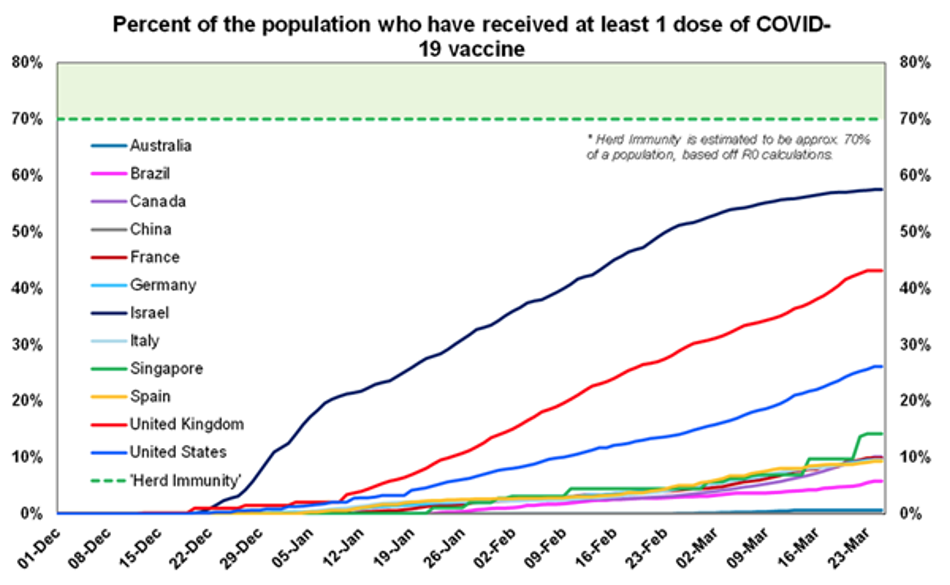

US President Joe Biden gave his first press conference this week. While there was speculation that there would be some announcement on the next spending package, there was no mention of this. The next spending bill is likely to be around the $3 trillion mark focussed on infrastructure and investment. There may end up being multiple bills passed, depending on the support that is received from the Republicans. Republicans are not likely to agree to significantly higher taxes to pay for infrastructure or green energy plans. But multiple bills also have complications because the reconciliation process doesn’t’ allow for unlimited bills. Biden did mention that his initial target of vaccinating 100 million people in his first 100 days in office has now been doubled to 200mn. So far, the US has vaccinated 130.4 million people (or around 26% of the population). There was no other major news to the vaccine rollout this week.

Powell and Yellen testified before the House Financial Services Committee. Comments around the risks to inflation continue to be downplayed - Powell and Yellen expect that inflation will move higher in 2021 from supply-chain bottlenecks and base effects but that this effect will not be large or persistent.

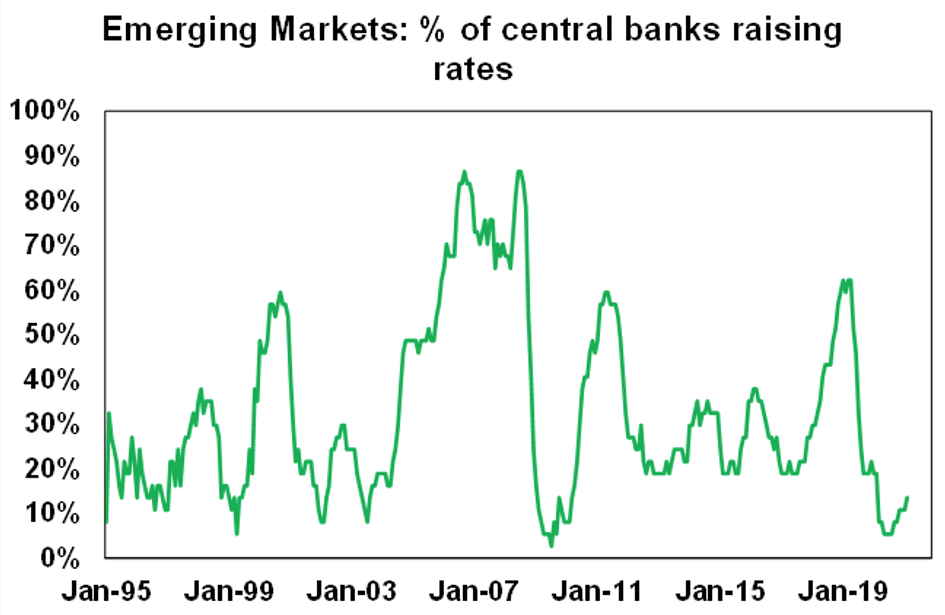

In Turkey, President Erdogan replaced the central bank governor unexpectedly because the central bank hiked interest rates more was deemed necessary (875 basis points worth of hikes in four months). This move has questions the independence of the central bank and further downside is likely in the Turkish Lira and other Turkish assets. We have seen some emerging markets start to hike interest rates recently (see chart below) to prevent capital outflows as global growth picks up and global bond yields lift which moves capital away from emerging markets and puts downward pressure on currencies which leads to inflationary pressures and higher debt burdens (because a large chunk of emerging market debt is in $US). Higher interest rates should limit these falls in emerging market currencies.

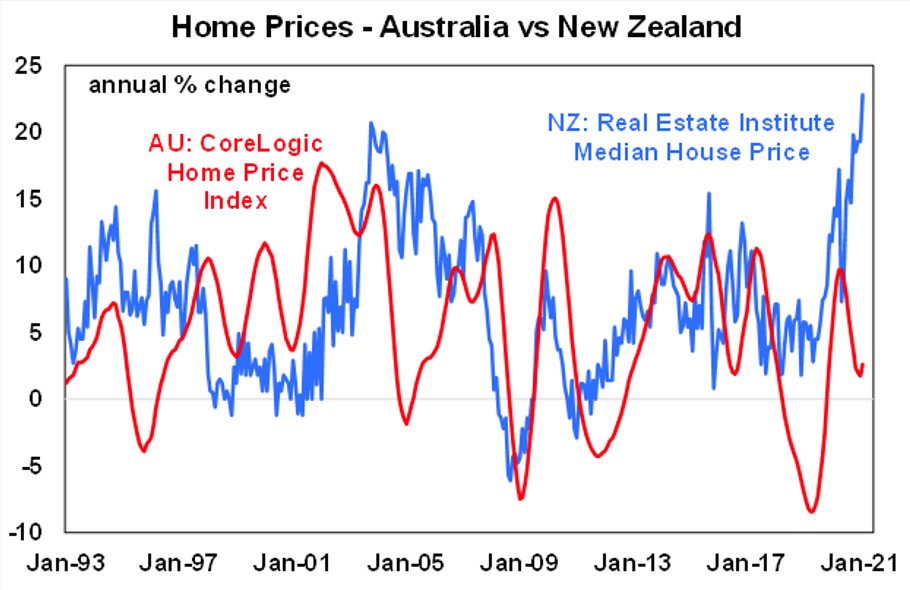

The New Zealand Labour Government implemented some big changes to housing policy this week to cool medium-term house price growth and avoid risks around elevated investor lending. Changes include: removing interest deductions (or negative gearing) for investors (except for new builds), increasing the time that you need to hold onto a property for to avoid paying tax when you sell to ten years from five years (which reduces churn in the housing market), giving more people access to the First Home Grants and Loans scheme with increased income and house price caps and plans to boost housing supply. The government wants to tilt the balance in the housing market away from investors and towards first home buyers. The New Zealand housing market has been running very hot since the pandemic with house prices up by 22.8% over the year to February. While Australia has also seen a very fast turnaround in the housing market, home prices are up by 2.6% across the eight capital cities (see the chart below) which is much smaller compared to New Zealand. Following this news, the $NZ has fallen by around 7%. In the long-run, these changes are likely to mean lower home price growth, lower housing debt, less interest rate hikes required by the Reserve Bank of New Zealand and potentially some upward pressure on rents (although new builds still qualify for negative gearing concessions). Australia is unlikely to follow suit with changes to negative gearing or capital gains tax (remember these policies were not looked upon favourably at the last federal election) but macro prudential policy is likely to become implemented gain over 2021 to slow down the frenzy in the housing market.