12 July 2025

1300 794 893

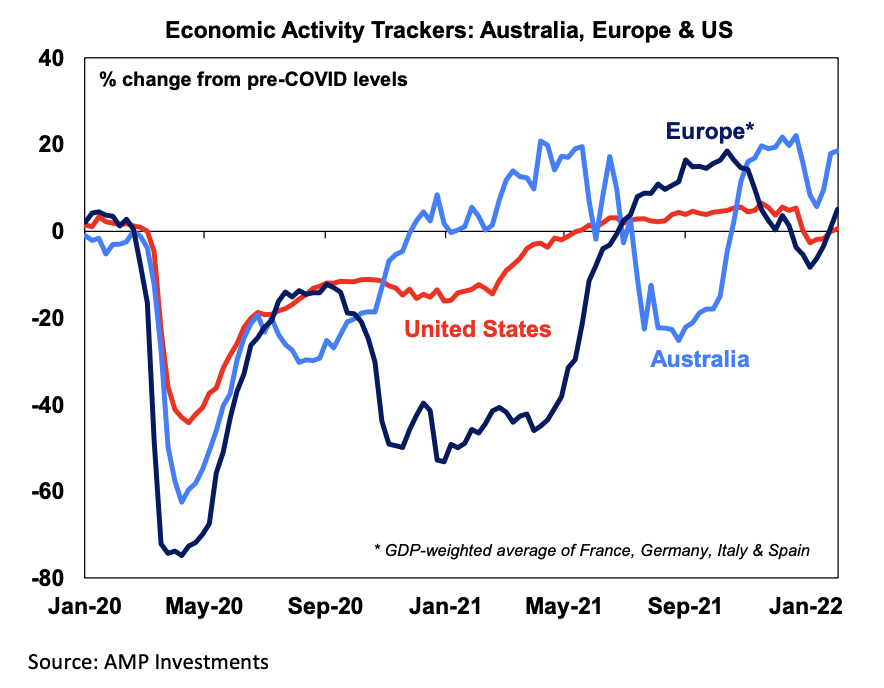

Economic activity trackers

Our weekly economic activity trackers have continued to improve this week (albeit very slightly). In the US, jobless claims, job ads, mobility, restaurant bookings and hotel bookings all improved. In Europe, the roll over in Omicron cases has been matched by an improvement in hotel bookings, Apple mobility, restaurant bookings, retail foot traffic and job advertisements. In Australia, credit card spending, mobility, hotel bookings and job advertisements all rose. But, all trackers still have further room to increase to get back to pre-Omicron levels.

Major global economic events and implications

US January CPI data was stronger than expected. Headline CPI rose by 0.6% (expectations +0.4%) and core CPI (excluding food and energy) also rose by 0.6% (expectations +0.5%). This took annual headline CPI up to 7.5% (from 7.0% in January) and core to 6% (from 5.5%). This was the largest headline annual pace of inflation since 1982.

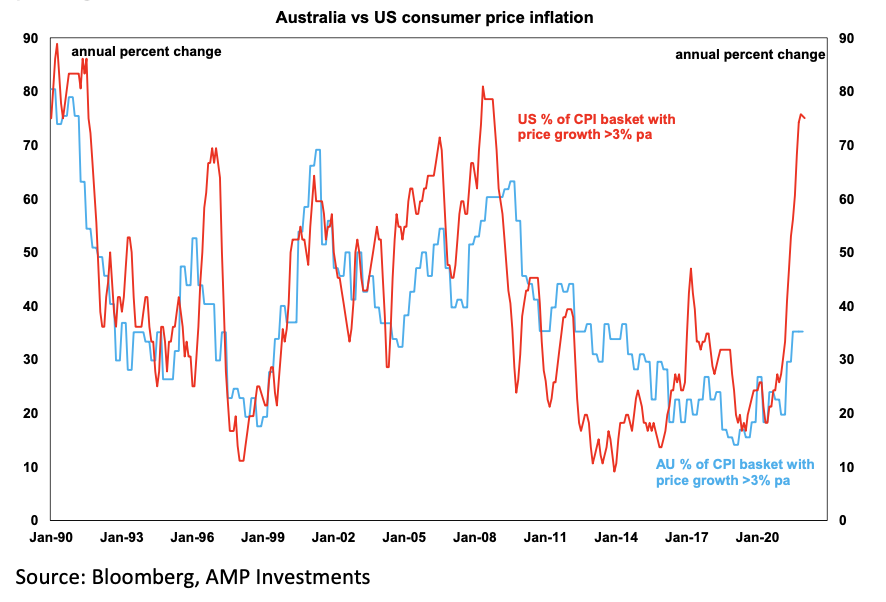

High inflation is still occurring in areas related to pandemic disruption (like used vehicles and airfares). But price growth for everyday items like primary rents and medical care services is also too high and CPI breath is very elevated. About 75% of components in the CPI basket have annual price growth above 3% (see the chart below). In comparison, about 35% of Australian CPI components have annual price growth above 3%.

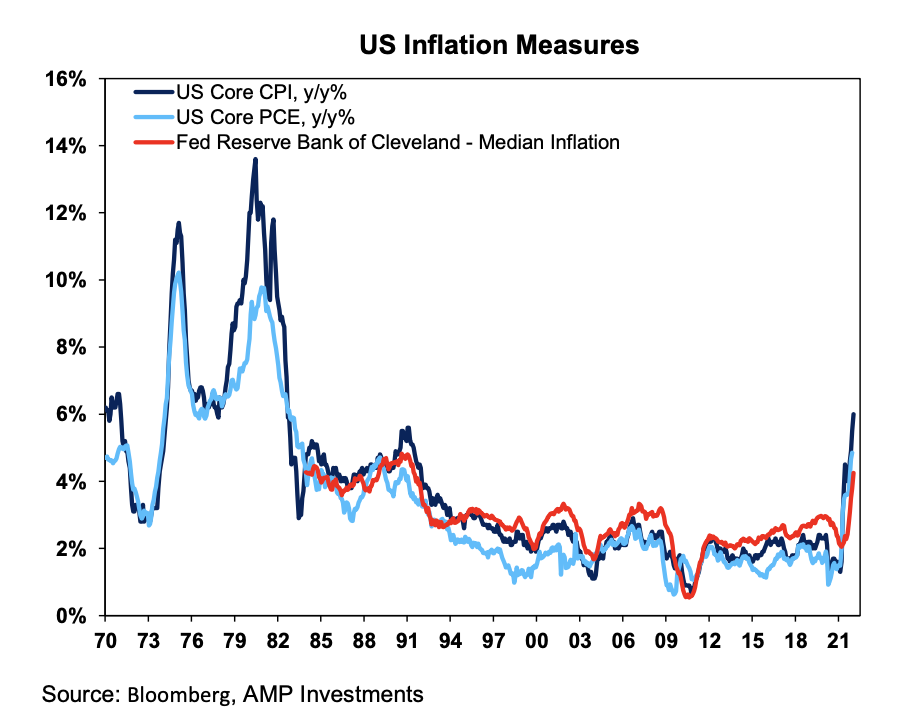

US NFIB small business confidence fell in January (to 97.1 from 98.9 in the prior month). Small business confidence has been trailing broader business conditions in manufacturing and services (according to the PMI and ISM) – see the chart below since the pandemic which could reflect less pricing power for small businesses or issues with staffing shortages.

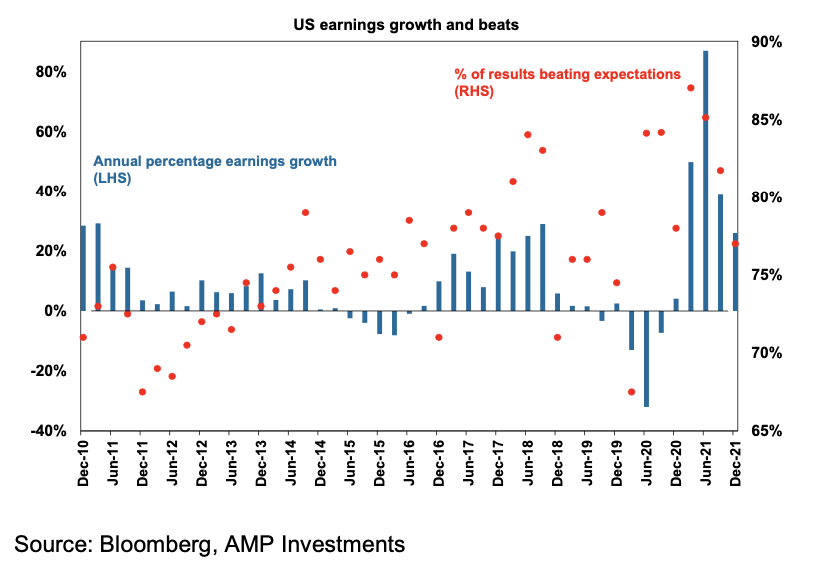

The University of Michigan consumer sentiment survey fell more than expected in February to 61.7 (from 67.2 last month), its lowest level since 2011 which reflects the high inflation environment that constrains consumer spending. 70% of US S&P 500 companies have reported December quarter earnings with 77% of results beating expectations which is just above average. Consensus earnings growth expectations are for a rise of 26% in earnings over the next year, which is a solid result and a good sign for share market returns (especially at a time when interest rates are increasing).

Australian economic events and implications

December quarterly retail data showed a big 8.2% rise in the volume of retail sales over the quarter, a bit stronger than expected. This will make a positive contribution to December quarter GDP growth of 1.4 percentage points (after retail detracted 0.8 percentage points in the September quarter during the Delta lockdowns). Our current forecast for December quarter GDP is a 3.0% lift (after a 1.9% decline last quarter) with annual growth running at 3.6% (this looks high but it reflects the bounce back in growth after the Delta lockdowns). March quarter GDP is expected to be softer (our current forecast is a rise of 0.4%) as January activity was negatively impacted by the Omicron outbreak.

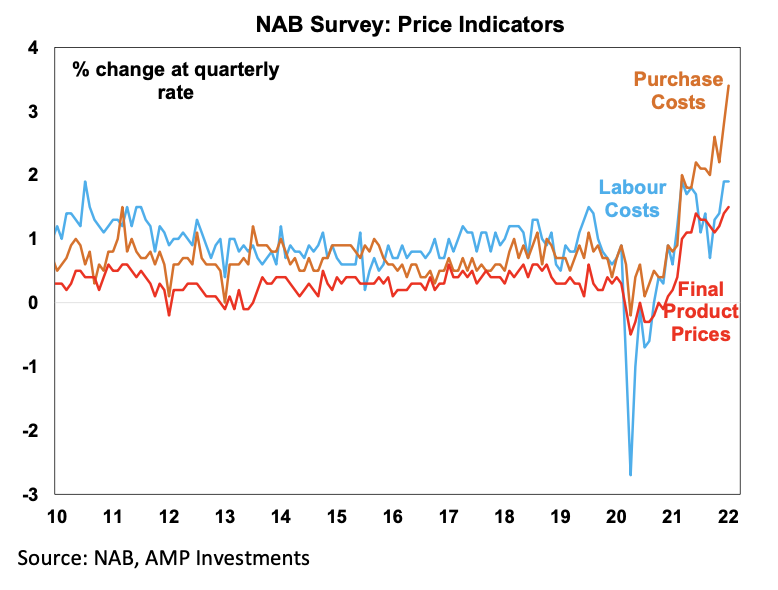

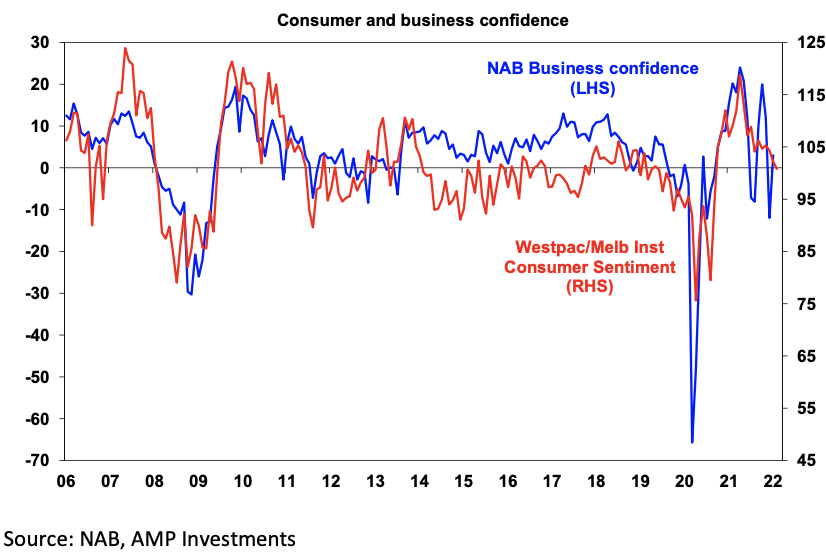

ANZ job ads fell by 0.3% in January after a 5.5% decline in the prior month but have been very over the past year and are still 27.3% higher than a year ago. The January NAB business survey showed a drop in business conditions (down to 3 from 8) but a lift in confidence (up to 3 from -12) but the January survey is complicated by the Omicron outbreak which caused some weakening in economic activity and staff shortages. Lower Omicron cases in February should mean a lift in both confidence and conditions. Price indicators in the survey still suggest elevated purchase costs for businesses while final product price increases haven’t been as large. Labour costs have also risen and are above long-run averages.

The February Melbourne Institute consumer confidence survey fell again in February (for the third month in a row) to 100.8 which means that confidence is just positive (a reading of 100 is neutral). This is in line with the weekly ANZ consumer confidence readings that have been trending down in recent weeks. Consumer confidence is now at its lowest level since September 2020. While low consumer confidence is generally not a good sign for consumer spending, retail consumption doesn’t seem to have been affected too much (so far).

RBA Governor Lowe appeared before the Standing Committee on Economics in parliament and re-iterated that the central bank has time to be patient in raising interest rates because high inflation is still reflected in some Covid-related disruptions. Lowe noted that raising rates too soon could slow progress in the labour market at a time when the unemployment rate is moving lower. In our view, the RBA will only have a limited amount of time to be patient before it has to raise interest rates. We see inflation and wages running above the RBA’s forecasts in 2022 which will result in rate rises starting from August (although the risk is an earlier move in June after the election). This is probably sooner than the RBA themselves expect at the moment but inflation is increasing swiftly around the world, which Australia is now catching up to.

December half-year earnings continued this week, but only about a quarter of ASX200 companies have reported results so far. Consensus earnings expectations for this financial year are for a 13% rise in earnings led by energy, industrials, and financials. Given Delta and Omicron disruptions a key focus will be on outlook statements.

Australian borders will completely open to fully-vaccinated tourists from February 21 (subject to arrival caps and quarantine requirements of each state/territory). An inflow of overseas workers could put some downward pressure on employment growth and wages, but it depends how fast workers come back. Some industries facing skills shortages (like hospitality) would welcome the move.

What to watch over the next week?

US January industrial production data, February NAHB housing index and January retail sales figures are all released on Wednesday along with the FOMC meeting minutes for the January Board meeting. The meeting minutes are likely to reflect the sentiment in the January press conference which sounded hawkish on interest rate rises without being panicked. Although all of this looks a little dated now after the January inflation data and comments from Bullard. January building permits, housing starts and existing home sales figures are also released (on Thursday). US December quarter earnings season also continues next week.

In Europe, Euro area industrial production for December is released (on Monday). December quarter employment (released on Tuesday) is likely to be negatively impacted by high Omicron cases over the quarter, similar to the low rise in December quarter GDP.

UK data next week includes the December unemployment rate (released on Tuesday) and January consumer price data (released on Wednesday) which is expected to show core inflation remaining high at over 4% per annum.

In Japan, December quarter GDP (released Tuesday) is expected to show a 1.5% lift but this follows a drop in the September quarter from Covid-related issues. January consumer price data (on Friday) is expected to show a lift of 0.6% but in core terms (excluding fresh food and energy) annual inflation is likely to be 1% lower over the year to January.

China consumer price data for January (released on Wednesday) should show annual price growth of 1% over the year to January.

In Canada, consumer price data for January (released on Wednesday) should show continued strong inflation pressures with core consumer price data tracking around 5% on an annual basis.

In Australia, RBA Board minutes for the February meeting are out (on Tuesday) but it’s difficult to see anything new in them given the release of the Statement on Monetary Policy, The Governor’s speech last week and the appearance before parliament today. January employment data (released on Thursday) is expected to show a fall in jobs over the month, by 20K because of the decline in economic activity in January, (according to the timely activity indicators) from the outbreak of Omicron. A decline in the participation rate (from 66.1% to 65.9%) should help to keep the unemployment rate low at 4.1%.

December half-year earnings also continue with close to another 50 companies reporting next week including Carsales.com, BHP, Seven West Media, Dexus, Treasury Wine Estates, Vicinity Centres, Fortescue Metals, CSL, Santos, Wesfarmers, Transurban, Magellan, Newcrest Mining, Tabcorp, Whitehaven Coal, Woodside Petroleum, Crown Resorts, Goodman Group, Origin Energy, Telstra and QBE.