6 July 2025

1300 794 893

Investment markets and key developments over the past week

Share markets started the week on a positive note, clawing back some of the declines that occurred in January. However, the elevated US inflation data worried investors about fast interest rate rises from the US Fed alongside heightened fears of a Russia/Ukraine conflict (which I think is a low probability). US shares were 1.8% lower over the week but this was not uniform across other share markets. Australian equities rose by 1.4%, reacting positively to this week’s December half-year earnings results. European shares were 1.7% higher over the week, Japan +1.7% and China +0.8% after the Lunar New Year holiday last week.

Iron ore prices remained elevated at close to $150US/tonne after news that China set 2030 as the new deadline for peak emissions for the steel industry (which was 5 years later than the previous target). Higher iron ore prices provide a boost to the Federal government budget. Oil prices are still high at about $90/barrel and most metal and agricultural commodity prices rose over the week. The AUD rose ever so slightly to 0.71 US dollars.

Higher than expected US January consumer price data

The highest US inflation in 40 years will put more pressure on the Federal Reserve to rein in easy monetary settings at upcoming meetings. US voting Fed member Bullard spoke after the inflation data was released and said that the Fed would need to raise rates by 100 basis points by July. There are three meetings until July (March, May and June) which would mean a 50 basis point increase at one of the meetings and two 25 basis point rises (although the Fed could also hold an inter-meeting if required).

Market pricing now reflects these comments and assumes interest rates about 1.25% in 6 months time (that’s an increase of just over 1% from current levels). We agree with the market pricing and now see the Fed being more aggressive and front-loading interest rate hikes in the first half of the year to take the heat out of inflation. We expect a 50 basis point hike in March, followed by another 25 basis point rise in May and June. US 10-year yields are now just over 1.9%, an increase of 16 basis points since early last week (with 10-year yields touching 2% after the inflation data). Moves in Australia have been similar, with 10-year yields at 2.2%, from 1.89% early last week.

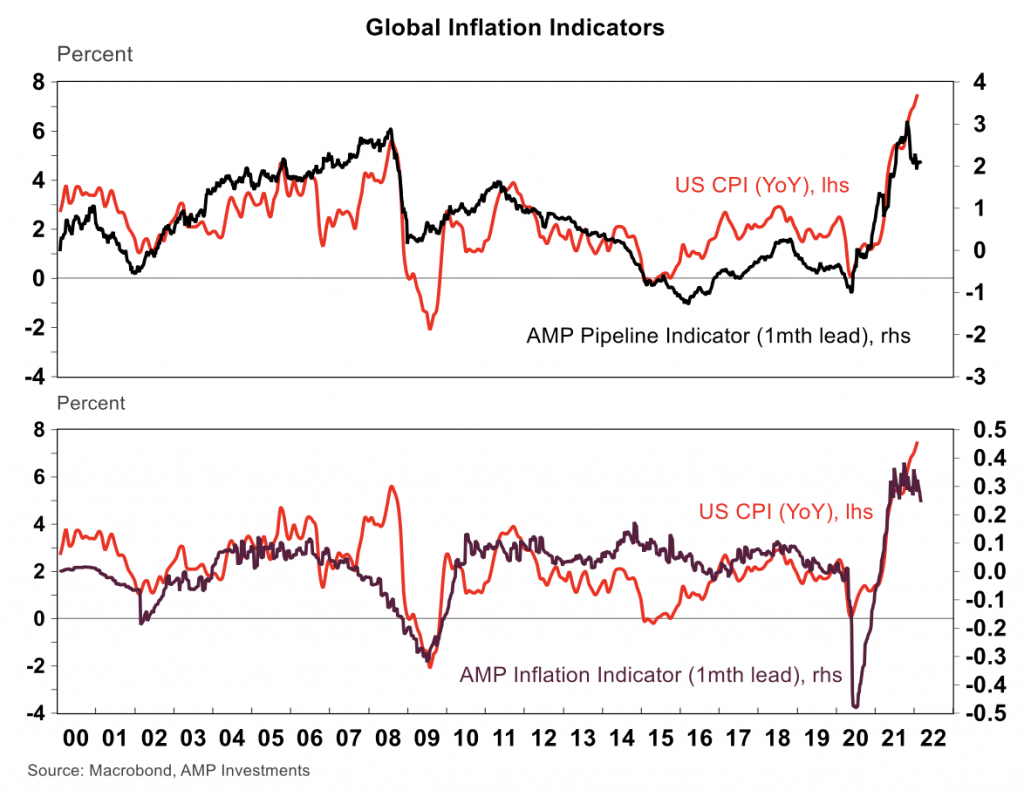

The peak in annual US inflation is likely to be about February/March, according to our inflation indicators that track both supply chain/pipeline pressures and traditional measures of inflation (like output gaps) – see the chart below. But, with annual inflation now at 7.5%, it will take some time for consumer prices to normalise.

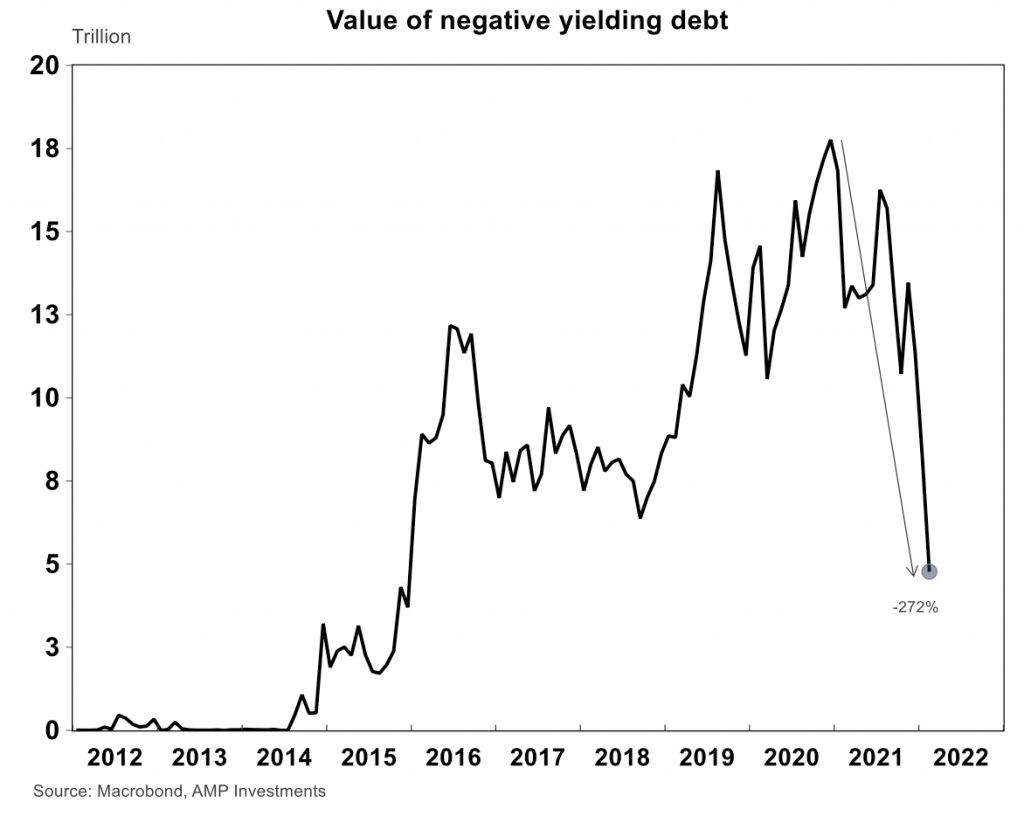

The value of negative-yielding debt has plummeted since its peak in December 2020 (down by 272% so far!).

European yields have swiftly moved into positive territory again and Japanese yields are approaching 0.25%, with the Bank of Japan saying this week that it will step in to defend the upper end of its yield target (0.25%).

We see further upside to global bond yields as central banks hike interest rates further. While higher bond yields can occur in tandem with further share market gains, it is unlikely to be smooth sailing as the market worries about interest rates getting hiked too fast.

Coronavirus update

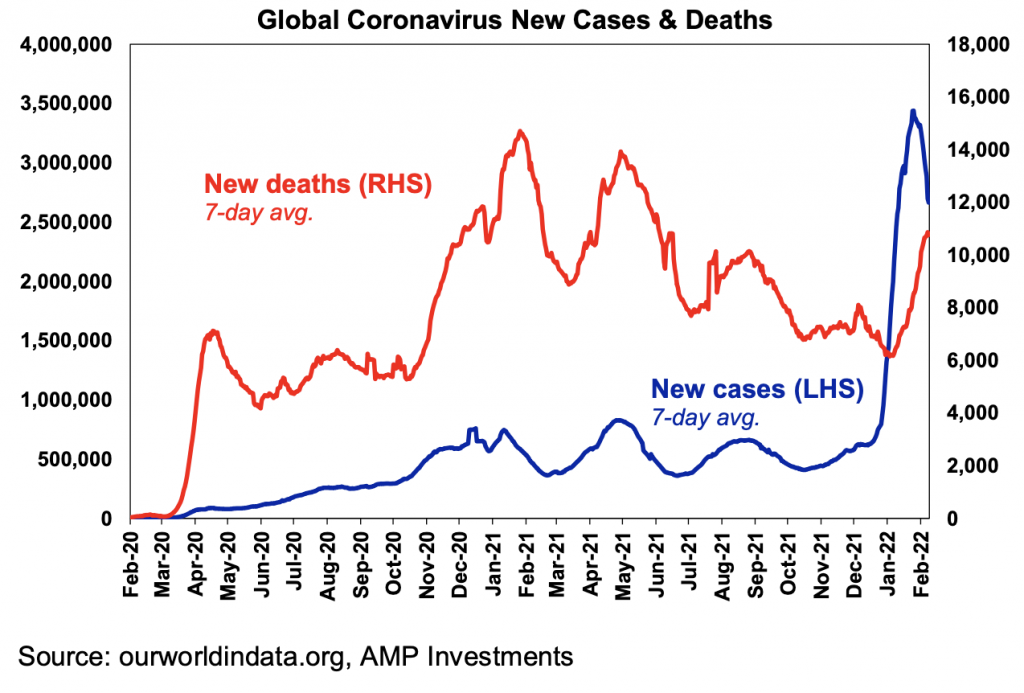

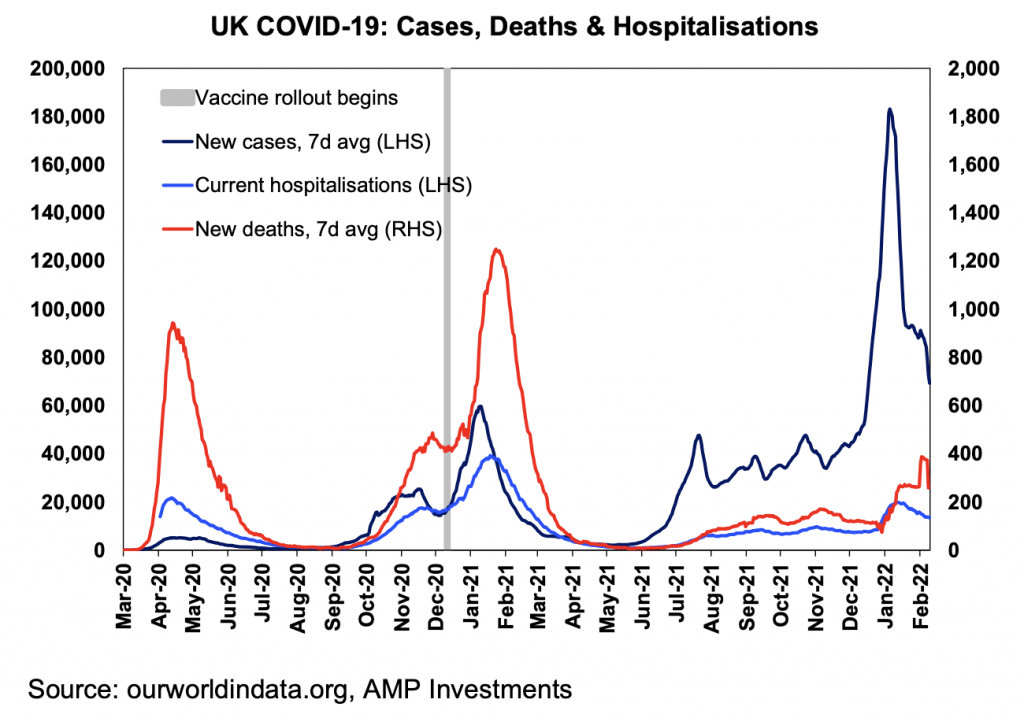

New Covid-19 cases are rolling over again around the world (see the chart below).

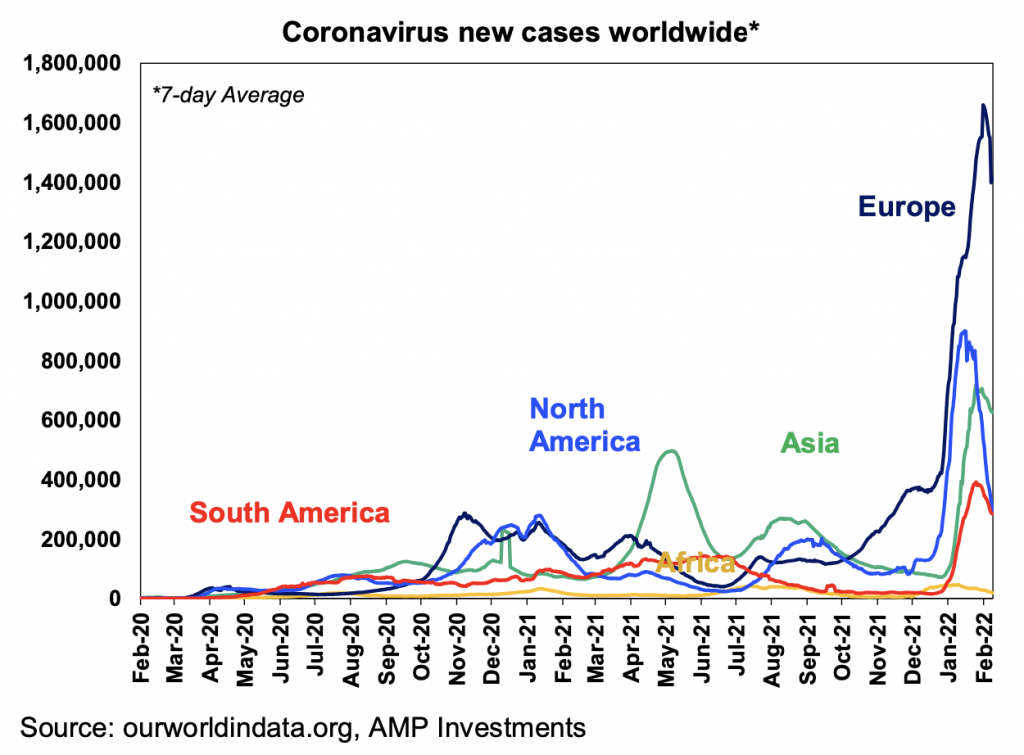

New cases have fallen in the US, Asia, South America and now Europe after the recent spike in the UK from the Omicron sub- variant BA.2. Within Europe, cases have fallen significantly in Spain, Italy, France and the UK but are still rising in Germany. Some European countries are opting to remove all Covid restrictions (Denmark, UK, Finland) leaving it up to individuals to manage illnesses which will hopefully not lead to any strains on the hospital systems.

New deaths from Covid-19 and hospitalisations are still running at lower levels compared to previous waves (see the UK as an example below), and are at much lower multiples of new cases which confirms the less severe nature of the Omicron variant, prior covid exposure and vaccines working and better treatment for those infected.

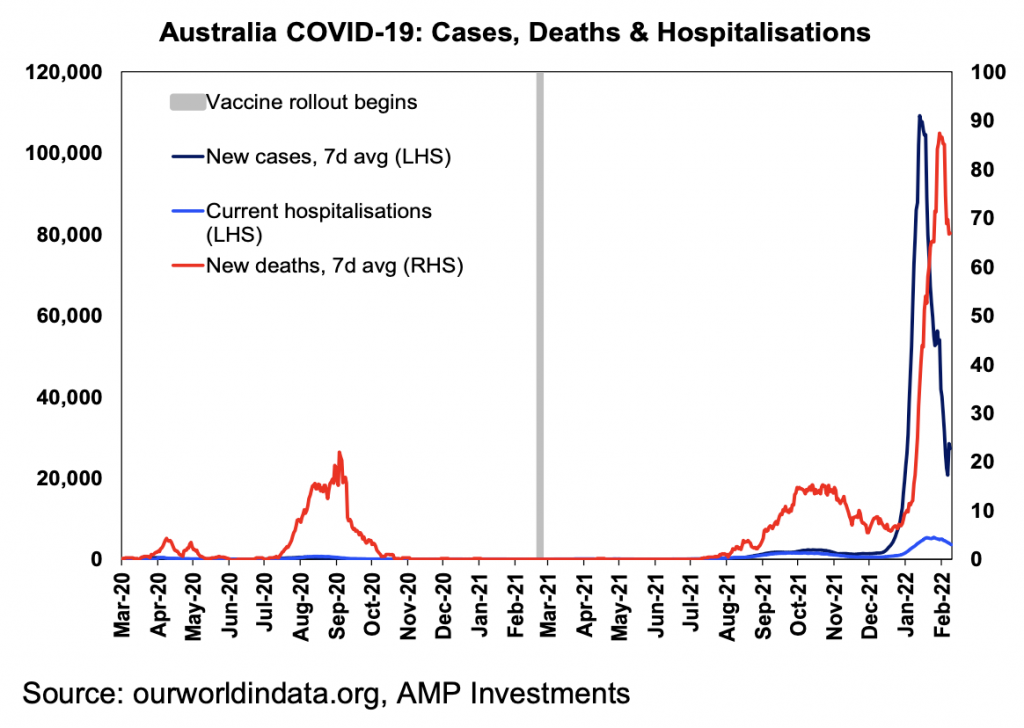

Australian Covid-19 cases continue to decline and deaths are rolling over and are at low levels relative to new cases (see the chart below). There is still a risk that new cases rise as children go back to school but hopefully hospitalisations remain low (as children tend to face fewer health complications compared to adults).

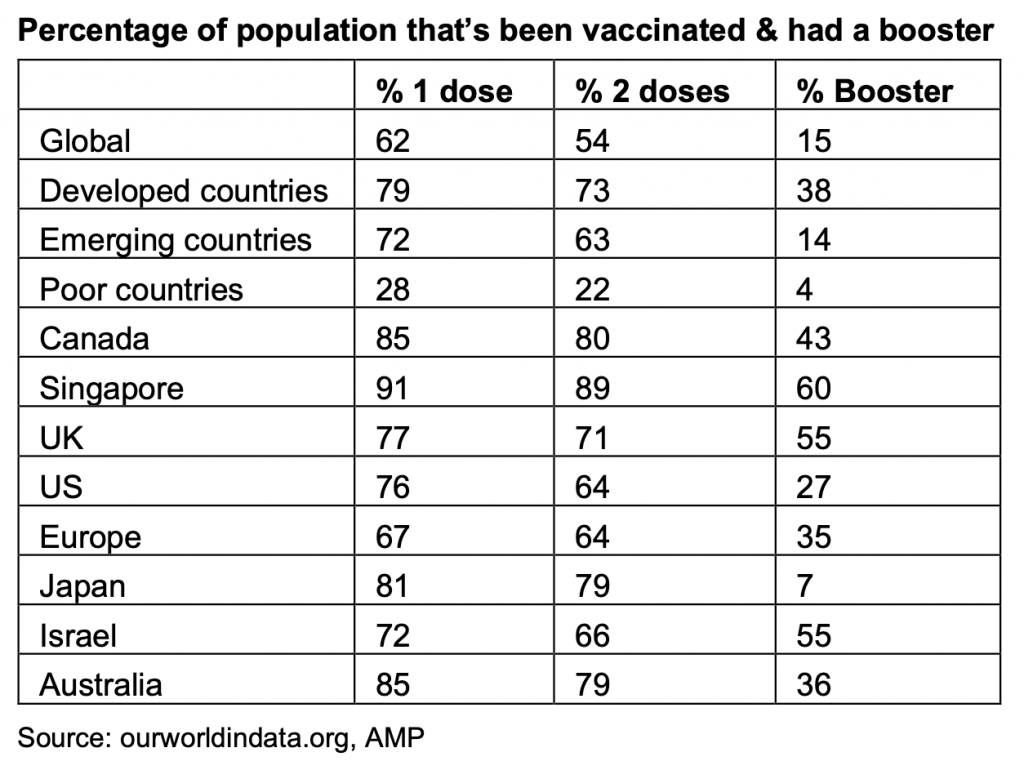

About 54% of the world is now vaccinated with two doses and 15% have had a booster. But, vaccine uptake is slowing in the developed world, especially for boosters (because there are now fewer incentives to get a booster and Omicron has proved less deadly). There is still a risk that a new strain comes along from poor countries where only 22% are fully vaccinated. Rich countries should be assisting poorer countries with access to vaccines and medical staff to administer them.

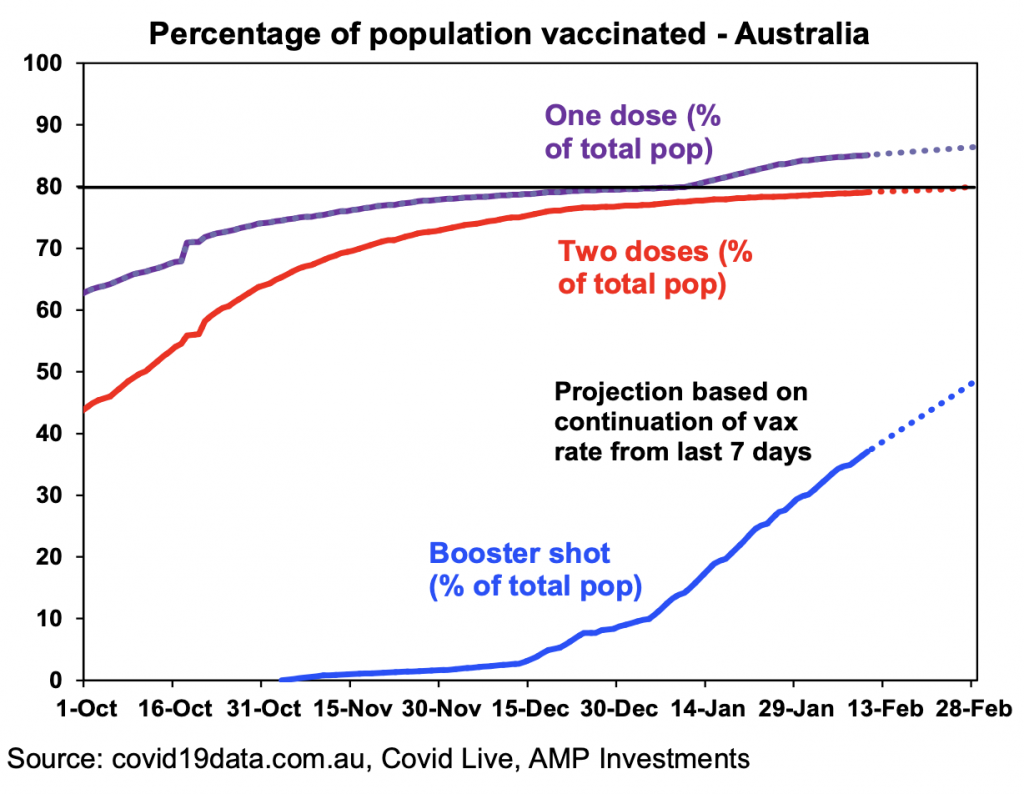

In Australia, 36% of the population have had a booster shot but again, the take-up has been much slower than the first two vaccines.

Outlook for markets

Global shares are expected to return about 8% this year but we may now be starting to see the long-awaited rotation away from growth & tech-heavy US shares to more cyclical markets. Inflation, rate hikes, the US mid-term elections and China/Russia/Iran tensions are likely to result in a far more volatile ride than 2021, and we are already seeing this.

Despite their rough start to the year Australian shares are likely to outperform helped by stronger economic growth than in other developed countries and leverage to the global cyclical recovery.

Still-very low yields and a capital loss from a rise in yields are likely to again result in negative returns from bonds.

Unlisted commercial property may see some weakness in retail and office returns, but industrial property is likely to be strong. Unlisted infrastructure is expected to see solid returns.

Australian home price gains are likely to slow with prices falling later in the year as poor affordability, rising mortgage rates, higher interest rate serviceability buffers, reduced home buyer incentives and rising listings impact.

Cash and bank deposits are likely to provide very poor returns, given the ultra-low cash rate of just 0.1%.

Although the AUD could fall further in response to coronavirus and Fed tightening, a rising trend is likely over the next 12 months helped by still-strong commodity prices and a decline in the USD, probably taking it to about $US0.80.