4 July 2025

1300 794 893

This article was originally published in the Switzer Report on May 7, 2020. Click here to take a free trial.

The rally that started in late March has been surprisingly strong. Many equity exchanges have technically entered a new bull market, having rallied +20% or more off their intra-month March lows. (If anything, it possibly suggests that using labels such as bull or bear markets matter less than most people think if you can enter both within a five-week period!) The recovery in markets has most likely been driven by robust central bank support and a belief in a very rapid economic rebound – the so-called V-shaped recovery.

We maintain our view that the global economic recovery will at best start in the fourth calendar quarter of 2020 and will slowly gain traction in 2021 – in other words, a U-shaped recovery. The reason behind our more conservative stance is driven by the surge in unemployment globally.

Economies shed labour much faster than it can be re-employed. When the recovery starts, employers are unlikely to initially staff up to pre-recession levels until a clearer picture of the sustainable demand emerges. Even then, there are the day-to-day frictions of the employment market (employees may have found jobs in other industries, businesses may have closed, people or businesses have relocated, etc.) that will cause a lag to re-employment. The scale of job losses around the world over the last eight weeks has been staggering, and we do not think it will simply bounce back. As such, we believe that labour markets will take a long time to return to 2019 levels, meaning aggregate demand will also take some time to recover.

In addition, we acknowledge that the rising risk of bankruptcies, renewed geopolitical tensions and the possibility of a Eurozone debt crisis triggered by the coronavirus means the risk is more likely to the downside (i.e. an extended U-shaped or possibly L-shaped recovery) than to the upside.

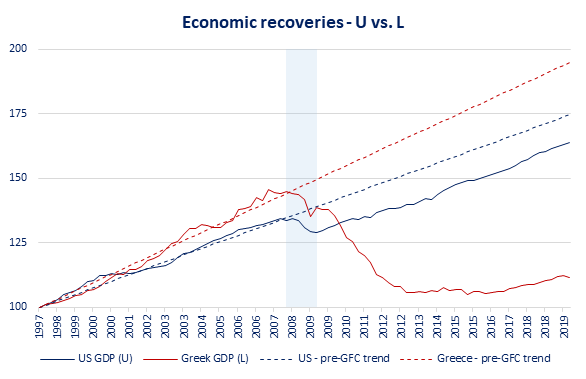

To demystify the alphabet soup of V, U and L-shaped recoveries, consider the chart below, which presents the GDP for the USA (blue) and Greece from December 1997 to December 2019 (red), indexed to 100.

Shaded area indicates US recession during global financial crisis. Based to 100 on 31 December 1997.

Following the global financial crisis of 2008/2009, the US experienced a U-shaped recovery. The growth rate mostly recovered to the pre-crisis trend – the slope of the GDP line is roughly the same after 2009 as to the pre-crisis trend – but the lower output level after the crisis indicates a once-off shock to the economy that reduced output for an indefinite period. Put differently, after 2009 the US experienced no sustained period of above-trend GDP growth that returned the actual output to pre-crisis trend levels. In contrast, Greece experienced lasting structural damage to its economy: not only did the output levels decline precipitously, but the growth rate has never recovered – the dreaded L-shaped recovery.

We believe that central banks and governments are working overtime to avoid the latter outcome but given that the true issue – a pandemic – did not originate in financial markets, it cannot be fully solved by the normal toolkit policymakers would employ. The determining factor of when the economic recovery begins in earnest and how strong it might be will be decided by the duration and severity of the public health response, which in turn will be determined by the successful containment of the spread of COVID-19. In Australia and New Zealand, we are fortunate enough to be debating a phased re-opening of our economies soon; clearly, this is not the case everywhere.

A final word on the outlook: we are not worried about inflation at present. If anything, given the collapse in demand, there are massive deflationary forces at work right now. However, we believe there are some inflationary risks lurking in the future, but it is likely some ways off. We will return to this subject in a future note.

In terms of what to invest in, in my view, remains unchanged. I will continue to own the strongest companies in the world with bulletproof balance sheets.

Microsoft has been the largest holding in my fund for some time now. Given its strong incumbent position as a vendor to large enterprise IT organisations, the business has a foot in both the old (on-premise) and new (cloud-based) worlds of delivering computing services and applications. This expertise, combined with the breadth of offering, institutional knowledge, and strong relationships with technology decisionmakers, means Microsoft is uniquely positioned to help their clients to navigate this hybrid cloud landscape.

This combination of competitive advantages worked strongly in Microsoft’s favour over the quarter. As lockdown measures began to be implemented around the world, the number of employees asked to work from home rapidly increased. This presented substantial challenges to large businesses, as bedrooms and kitchen counters suddenly became endpoints to enterprise networks – endpoints that needed to be secured and integrated into the existing technology architecture.

Microsoft Teams – the application that combines video meetings, text-based chat and file storage and integrates into the Office suite of applications – has seen a massive surge in usage. While Zoom has captured the public imagination, we believe that large enterprises sees more value in Microsoft’s integrated approach. In addition, few technology decisionmakers were about to deploy previously untested or unsupported (and therefore possibly less secure) software into a live IT environment that was being transformed by the day to meet the rapidly growing needs of work-from-home solutions. Beyond Teams, other applications – like Office or Dynamics – also grew by double-digit rates. Demand for laptops to enable remote working supported Windows revenues, while the Xbox gaming division – a smaller component of the overall business – proved to be fairly resilient, with more gamers having time to play online.

We believe the transition to the cloud will likely only gather pace post-lockdown, as more businesses contemplate exactly how much rent they are prepared to pay when many employees can clearly work remotely. Azure – the cloud computing platform offered by Microsoft – saw revenues grow by roughly 60% this quarter.

Overall revenue growth was roughly 15%, while increased utilisation of the Azure cloud platform saw overall margins expand by roughly 2%. Free cash flow grew by nearly 25% year-over-year.

While Microsoft is sure to see some of its clients rationalise IT spend for the duration of the crisis and the recession, the critical nature of the products and services the business provides means it will likely have more resilient demand than many businesses out there.

The company has around $138bn in cash on the balance sheet and is steadily reducing its outstanding debt balance. I not only think Microsoft will navigate the current landscape successfully but believe it will ultimately emerge with a stronger competitive position over the next several quarters.

MSFT shares are up +17% in Australian Dollars in 2020 and remind you of the portfolio power of diversification by sector, stock and currency. Owning the best businesses in the world remains a sensible and sustainable investment strategy no matter what the shape of the economic recovery. Companies like MSFT are both offensive in terms of the structural growth they capture and defensive due to their industry dominance and bullet proof balance sheets.

Stay safe and best wishes.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.