There’s a viral post doing the rounds on LinkedIn and Twitter that claims CBA will unlock additional borrowing power for those who promise to rent out a room of their house. We decided to fact check what truly seems too good (or depressing) to be true.

The claim

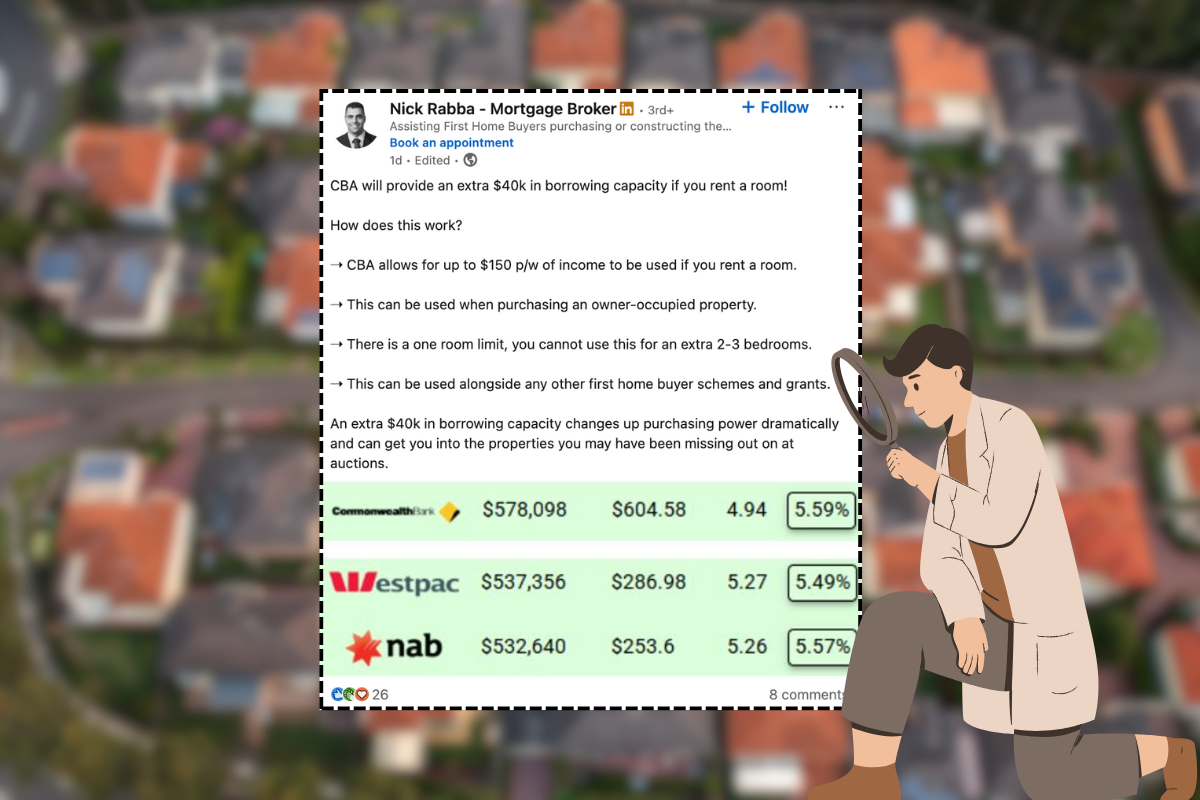

The post doing the rounds is from an enterprising mortgage broker by the name of Nick Rabba. Everyone say ‘hi, Nick’.

Nick – in the name of growing his clout online – decided to post a lesser-known hack for unlocking extra cash in from a bank when it comes to your total borrowing power.

His post reads:

CBA will provide an extra $40k in borrowing capacity if you rent a room!

Bold claim. Here’s how he says it works:

→ CBA allows for up to $150 p/w of income to be used if you rent a room.

→ This can be used when purchasing an owner-occupied property.

→ There is a one room limit, you cannot use this for an extra 2-3 bedrooms.

→ This can be used alongside any other first home buyer schemes and grants.

Thinking this was just another mortgage broker chasing followers (and leads), I decided to fact check. Naturally.

Is it true?

Turns out you can in fact do exactly this to score additional borrowing power out of a bank like CBA.

Here’s what it had to say in a statement it shared with me this evening confirming that the above was (mostly) accurate:

Earlier this year we expanded our rental income policy to allow the use of boarder income in home loan serviceability.

At CommBank, we are constantly reviewing and monitoring our home loan policies and processes to see how we can best meet our customers’ home buying needs while maintaining our prudent lending standards.

Mostly accurate?

I say ‘mostly’ because CBA couldn’t go as far to confirm that the $40,000 claimed by the poster is spot on.

According to the bank, ‘this will vary depending on each customer’s individual financial situation’.

So where did that $40,000 figure come from?

That extra $150 a week adds up to $7,800 a year in assessable income. Using a typical lending rule of thumb—where every extra dollar of annual income can support roughly five to six dollars of additional borrowing—that translates to about $39,000–$46,000 in extra capacity.

In practice, that means someone earning $90,000 a year might be approved for a $600,000 loan without a boarder, but could stretch that closer to $640,000 if they formally declare one.

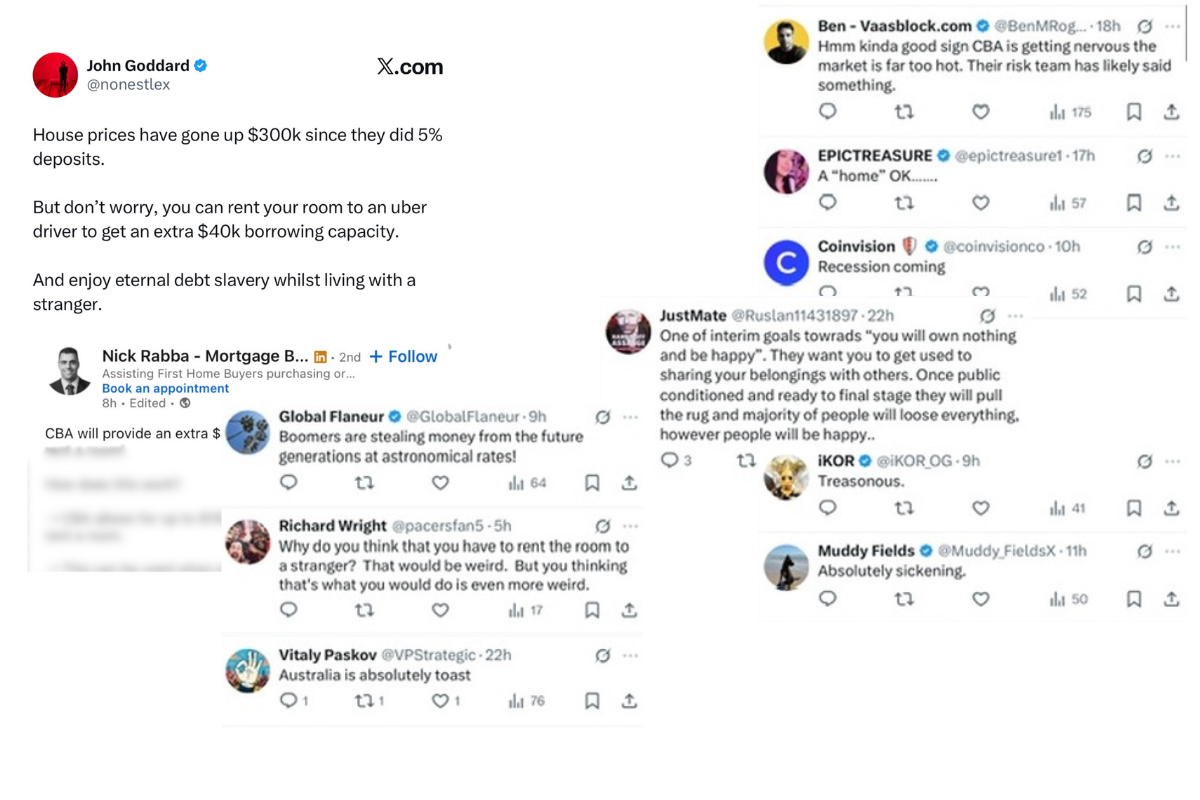

While some brokers have touted the change as a “hack” to unlock extra funds, it’s really a modest broadening of the bank’s income policy rather than a loophole. And regardless of the boost to buyers, not everyone loves the policy given the state of housing affordability in Australia’s capital cities right now.

Please enjoy the discourse.

If only home loan rates were coming down any time soon…