Key takeaways

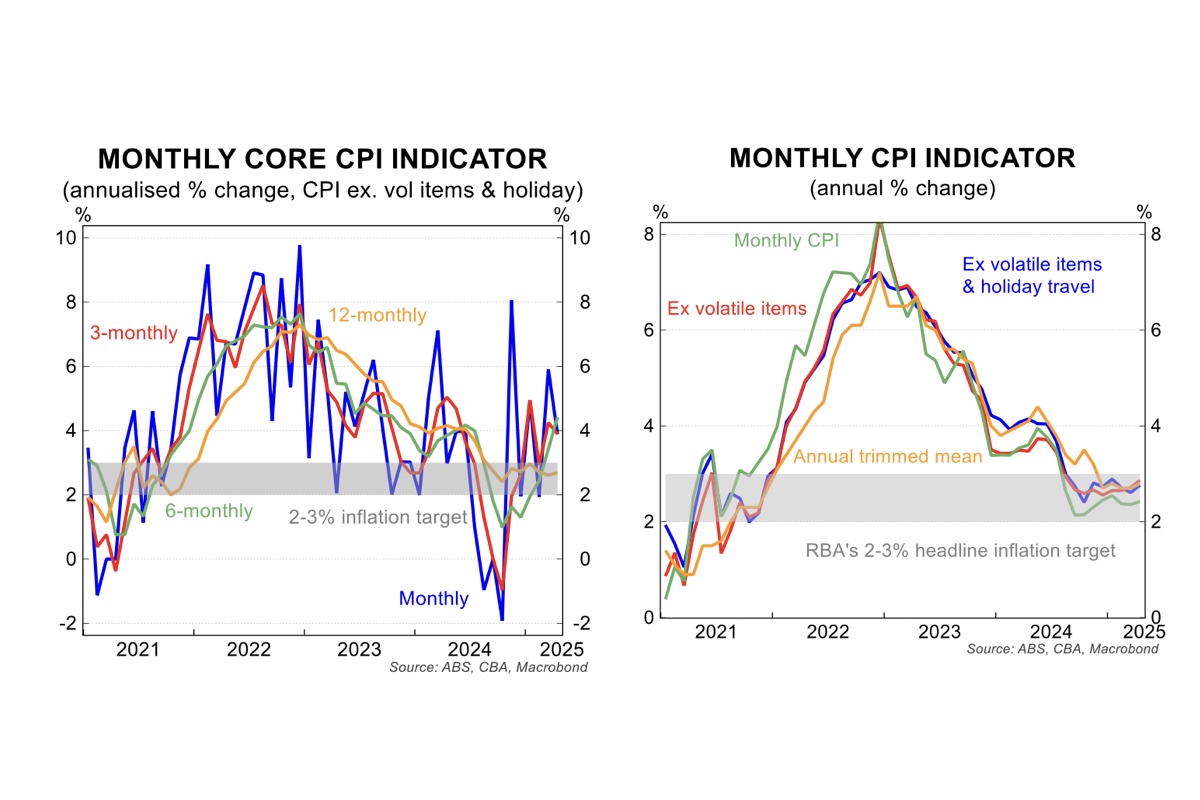

- Headline inflation rose to 2.8%/yr in July, a much bigger rise than anticipated.

- Electricity rose much more than expected due to the timing of rebates in NSW and the ACT, and travel prices were much stronger than expected. Both these should unwind in coming months.

- Annual trimmed mean inflation also rose strongly, up to 2.7% and now in line with the full quarterly CPI.

- The monthly CPI indicator can be volatile and significantly impacted by relatively few components moving sharply in an unexpected way. The RBA will get the August Monthly CPI indicator before their next meeting and this will provide further information on how the outsized moves unwind and an update on how services inflation is tracking.

Headline CPI inflation rose sharply to 2.8%/yr in July. This was well above our estimate (+2.0%/yr) and the market consensus (2.3%/yr). Annual trimmed mean also rose materially, up to 2.7%/yr to closer reflect the quarterly measure.

In the month, headline CPI rose by a large 0.9%/mth. This compares to a flat outcome in July 2024.

There were several key drivers that pushed headline inflation higher that will likely unwind and so are not a major concern. Indeed, there are two major surprises worth calling out in the July data of which alone contributed a large ~55bp to the forecast miss on our end.

Detail by category

Food

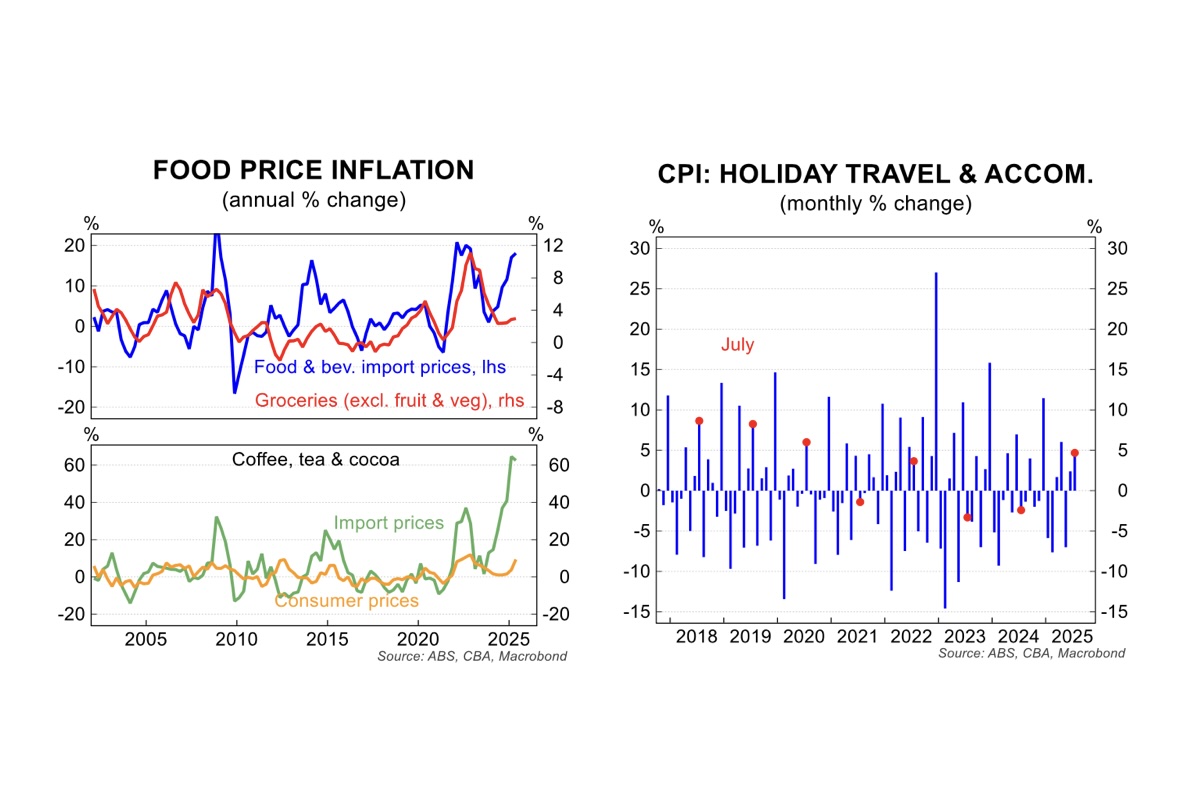

- Food inflation rose by 0.1%/mth which was softer than expected. Through the year, food inflation is sitting at 3.0%/yr. Sub-categories through the year that are a bit elevated include fruit and vegetables (+4.8%) and non-alcoholic beverages (+5.7%).

- Tea & coffee prices are rising at the second highest rate of any product in the CPI, up 14.5%. Global prices for coffee products remain under pressure with prices extremely elevated. Local producers are now passing this onto customers more materially.

Housing

- Housing overall increased by 1.9%/mth. The big driver was electricity (as above).

- New dwelling costs rose by 0.4%, a touch stronger than expected and is a key watch given its large share of the basket. Over the year, prices remain just 0.4% higher due to price declines earlier in the year.

- Rents are evolving as expected, rising by 0.3%/mth which saw the annual rate tick lower to 3.9%. We see continued progress on rents inflation for the next year or so. But advertised rents are starting to pick up again and rental markets remain tight. This will make it a key inflation watch in H2 2026 (see facing chart).

Furnishings & household goods

- Broadly in line with expectations, rising 0.4%/mth. In annual terms, durable household goods remain just 0.9% higher through the year – a benign level.

- Recall Governor Bullock called out durable goods as being higher than expected in April and this caused some anxiety for the Board, but the July numbers shouldn’t be a cause for concern.

What it means

Overall, today’s data was stronger than we and the market had expected. But much of the outsized surge in inflation can be explained by quirks regarding the timing of electricity rebates and holiday travel. These monthly movements will likely unwind in coming months.

This leaves analysts now waiting for the CPI for August to firm up expectations for the all-important quarterly print. We currently expect a 0.6%/qtr outcome for trimmed mean and 0.7%/qtr for headline. After today’s data, the risks at the margins are skewed to the upside and makes the August monthly CPI data a key release.

The first month of the quarter is overweight on goods and provides less informational content than subsequent and the RBA has flagged this in the past. It has also been at pains to point out the volatility in the monthly figures. For this reason, the Board is unlikely to be overly concerned about the surprisingly strong print.

It does however further support the view that the RBA is firmly in a cautious and data-dependant mode. The implied preference for a quarterly cadence of cuts will remain for now making November the next likely 25bp cut to 3.35%.

IMPORTANT INFORMATION AND DISCLAIMER FOR RETAIL CLIENTS

This content is prepared, approved and distributed in Australia by Commonwealth Securities Limited ABN 60 067 254 399 AFSL 238814 (CommSec) a wholly owned but non-guaranteed subsidiary of the Commonwealth Bank of Australia ABN 48 123 123 124 AFSL 234945 (the Bank) and a Market Participant of ASX Limited and Cboe Australia Pty Limited. All information contained herein is provided on a factual or general advice basis and is not intended to be construed as an offer, solicitation or investment recommendation in any way. It has been prepared without taking into account your individual objectives, financial situation or needs. Past performance is not a reliable indicator of future performance. CommSec, the Bank, our employees and agents may receive a commission and / or fees from transactions and / or deal on their own account in any securities referred to in this communication and may make investment decisions that are inconsistent with the recommendations or views expressed within this communication. Any comments, suggestions or views presented herein may differ from those expressed elsewhere by CommSec and / or the Bank. The content may not be used, distributed or reproduced without prior consent and any unauthorised use of the content may breach copyright provisions. CommSec does not give any representation or warranty as to the accuracy, reliability or completeness of any content including any third party sourced data, nor does it accept liability for any errors or omissions. CommSec is not liable for any losses or damages arising out of the use of information contained in this communication. This communication is not intended to be distributed outside of Australia.