It’s easy to look at tracking app, Life360, and think that it’s a little odd. Can this business keep up its success even thought Apple and Google offer these features baked into their devices for free? Let’s take a look.

When a tech company builds a business on a feature that Apple or Google might one day bake into their operating systems for free, investors start to get nervous. Just ask Dropbox (cloud storage), Evernote (cloud-based notes) or BlackBerry shareholders how their stock is going.

It’s raises one of the biggest and most persistent questions facing Life360 right now: can it sustain its user and revenue growth if tech giants move further into the location-tracking space?

What is Life360, anyway?

We talk about it a lot on here and on our shows but let’s go back to the beginning: what does this business actually offer?

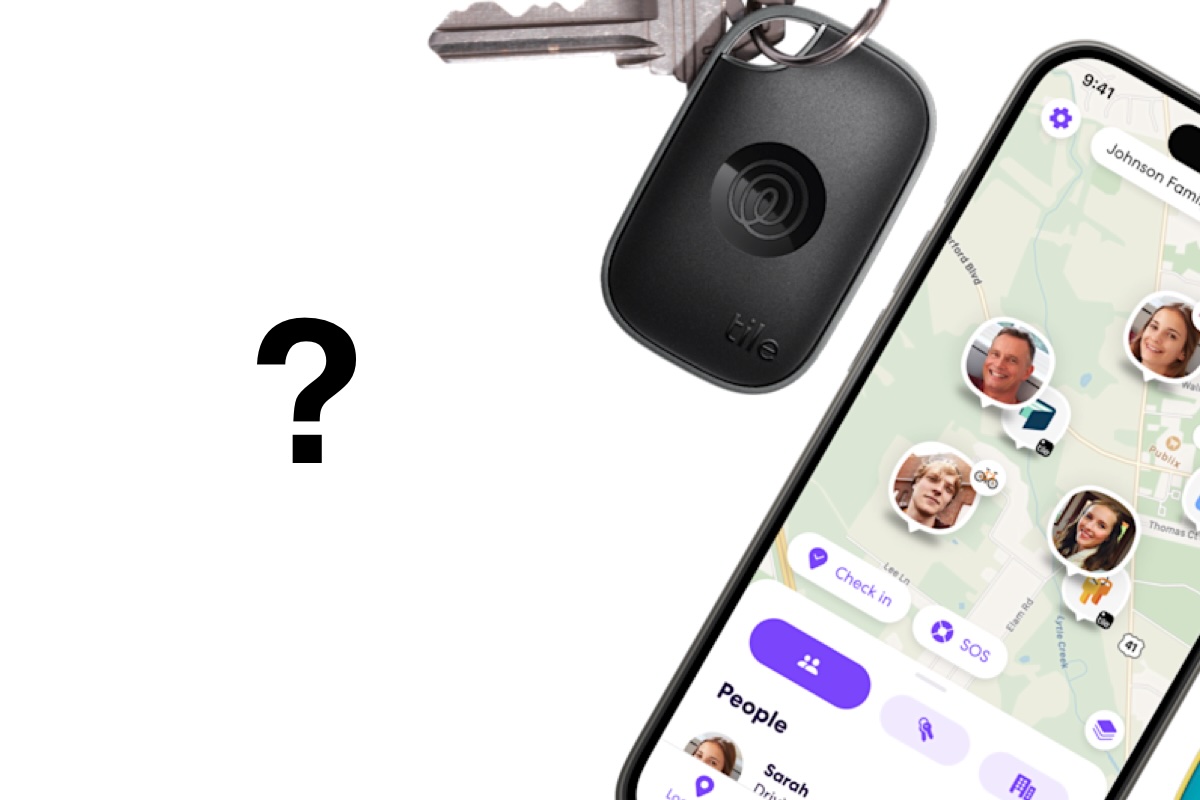

Life360 is a family safety and location-sharing app that lets users see where loved ones are, receive driving reports, and get alerts in emergencies.

It monetises through premium subscriptions, advertising, and increasingly, new services like insurance.

As at Q1 2025, Life360 had approximately 83.7 million monthly active users globally — a 26% increase year-on-year — with 2.4 million paying members.

Revenue hit $103.6 million for the quarter, up 32% year-on-year, while annualised monthly revenue climbed 38% to $393 million. The company’s share price has surged 87% over the past 12 months, reflecting investor confidence in its ability to scale.

Did Apple and Google ‘Sherlock’ Life360?

Life360 had the same advantage as many tech companies that had their lunch cut by big tech: they moved first.

Much like the aforementioned note taking service, Evernote, it was one of the first to come up with the idea of safety-based tracking for your smartphone and the smartphones of those you love.

But those features started coming baked-in to Google Android and Apple iPhone devices a few years ago now. In fact, Apple has a whole business unit dedicated to finding your stuff thanks to AirTags.

So why would anyone want Life360 when it’s already integrated into your phone from the people who actually make it?

This idea that big tech borrows great concepts from smaller developers actually has a name: “Sherlocking”. No, nothing to do with Baker Street’s most famous detective.

Sherlocking is the term that was coined for when big tech companies integrate strikingly similar features from third-party innovations and apps into their own products. Most noteably this happened to “Watson”, a search app invented years ago for the Apple Mac.

Apple built a similar search tool for all your digital stuff called Sherlock, and just like that, Watson was done, and “Sherlocking” was born.

Can Life360 compete against big tech?

Despite the integration of tracking gear into your phone’s operating system, Life360 continues its upward trajectory on the market.

Trading on the ASX, Life360 has jumped an astonishing 104% in the last 12 months alone. It’s off a little in the last week or so but it’ll still run you $32.48 a share today compared to $15.86 this time last year.

On this week’s episode of Switzer Investing TV, TenCap’s founder, picking guru Jun Bei Liu said again that Life360 is one of her faves for the new financial year.

We put it to her that it could fall apart at any minute, but she told us we were being hysterical!

Jun Bei Liu says investor concerns about competition from Apple and Google are valid but still overplayed.

“Life360 first started the tracking business way before Apple started Find My iPhone. And so when Apple first launched this, everyone thought the world [was] over for Life360,” Liu said on Switzer Investing TV.

Rather than killing the business Jun Bei Liu says big tech introducing tracking features actually helps Life360:

“What it has done is that it actually created more awareness in that whole circle,” Liu explained.

She points to the size and engagement of Life360’s user base as its moat. “It is one of the highest used social platforms there when compared to some of the most famous names like Facebook,” she said.

Life360 is growing its moat

That engagement is now being turned into multiple revenue streams.

“It’s got a very strong platform and all it’s doing now is actually trying to monetise that platform through many different initiatives,” Liu said.

“One is that you create the paid circle. The second is advertising. At the same time, you start creating some of those data products — they’re doing insurance, they’re doing other offerings. There are so many verticals.”

Crucially, she believes Life360’s first-mover advantage and user stickiness make it hard to unseat. “Because it’s the first — it is the incumbent and it’s got such a large base — it’s just very, very hard to dislodge.”

In fact, Liu added, “some of the tech companies, such as Google, have previously expressed interest in Life360,” suggesting the giants may prefer to partner or acquire rather than compete head-on.

Still, history shows tech can turn quickly when Apple and Google change course. Whether Life360 can continue to innovate and expand into new verticals faster than first-party features eat into its core value proposition remains the billion-dollar question.

Still, I should know better by now not to bet against Jun Bei Liu!