The RBA’s decision to raise rates is really an admission that both the Treasurer and the Reserve Bank Governor have not done their jobs properly.

While it’s gambling with our economic future by raising rates, the big news is that not all on the board that makes these cash rate decisions agreed with the 0.25% hike, taking the benchmark rate to 4.1%.

This revelation made me wish that the Governor of our central bank would do a Seinfeld-admission about why the board’s past efforts with interest rates have led to this.

Before I propose my script that Bullock could use to underline her honesty and help average Australians understand why home loan borrowers and small businesses with loans are set to make the belt-tightening exercises to kill inflation, I have to reveal this: the vote to raise rates was 5 to 4!

This means four members thought raising one month after they raised in February was an unnecessary move, considering this Iran war (if it goes on too long) could create a recession and rising unemployment, which usually leads to rate cuts!

In fact, Paul Bloxham, chief economist at HSBC, who thinks we might need a recession to effectively exterminate inflation, also has suggested that rate cuts might be needed by year’s end!

OK, I’ve kept you waiting too long. Now for my Seinfeld-like explanation that I’ve created for the Governor for why rates had to go up.

It could go like this: “You might have noticed we’ve been trying to beat inflation down since May 2022. And you might’ve also noticed that we’ve failed. The people on the RBA board are qualified to reduce inflation, KO unemployment and even influence the value of the Aussie dollar. So, why haven’t we been able to do that? That’s simple, it’s very, very hard!”

Let me join and suggest Bullock could have added the following on why the board has been unable to increase unemployment, which would have brought inflation into the 2-3% band. Here goes:

- They cut three times last year, which shows they didn’t see their assessment of where the economy was going was flawed.

- They didn’t work out that Jim Chalmers’ budget was blowing out, pumping up demand and fuelling inflation, which is a big mistake for economists and other charged with the job of keeping the economy out of trouble.

- President Donald Trump is a hard ‘guy’ to work out. We didn’t see this Iran war coming. It has spiked oil prices and pumped up petrol prices and inflation expectations.

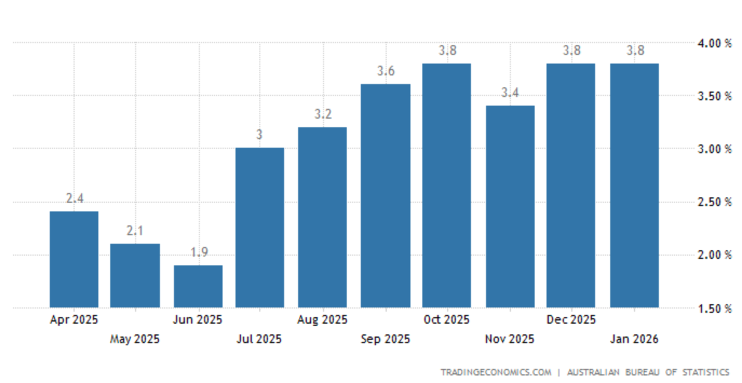

- There was political pressure on the RBA to cut rates in 2025. Why? There was an election in May last year! And the cuts started in February! Another came in May and then August. But after that, inflation started to rise in July, as the chart below shows.

- Our RBA didn’t go as hard as other central banks to kill inflation. While those economies ended up in recession, they did reduce inflation more effectively. I suspect political pressure made our RBA more ‘loveable’ to loan borrowers but now that love is on the slide, big time!

Australian Inflation

This is AMP’s Shane Oliver’s take on the decision:

“The RBA’s decision to hike rates to 4.1% was no surprise with it being about 65% factored in by the money market and 22 of the 30 economists surveyed by Bloomberg expecting a hike. The decision means that the RBA has now reversed all but one of the three rate cuts we saw last year, which of course followed 13 rate hikes seen in 2022 and 2023. Once passed on to mortgage holders, it will leave mortgage rates around levels prevailing 14 years ago. Of course, it should also mean a slight rise in bank deposit rates.”

Aside from my finger-pointing blame game about why rates were jacked up yesterday, here are a few other revelations from the RBA board meeting:

- 1. While the 5/4 vote in favour of a hike versus a hold suggests a close decision, Governor Bullock indicated that the debate was about timing not the direction of rates. In other words, while those looking for a hold were also hawkish, the four who said ‘no’ were in effect saying, ‘rates might have to go up but not now’.

- The RBA also indicated it will remain data dependent. On this front, the March quarter CPI data to be released in late April will be important.

- Shane Oliver says: “With the RBA hiking and the money market expecting nearly two more hikes by year end, interest rates in Australia are moving very differently to other major countries.”

- Oliver also pointed out: “Petrol prices have already increased by around 35% from their average in February, which, if sustained, implies a direct boost to inflation of around 1.2 percentage points, which will take it to around 5% from 3.8% year-on-year in January if prices stay around current levels.”

Did you see that?

There could be two more rate rises this year, which could leave the names Chalmers and Bullock as unforgettable figures in the memories of mortgagees and small business owners.

At times like these, those words of George Santayana, which I first saw decades ago in the memorial to Jews who suffered in the German concentration camp at Dachau, near Munich. At the end of the tour, we were reminded: “Those who cannot remember the past are condemned to repeat it.”

The upcoming May Budget will be a test for Jim Chalmers and his reputation going forward. If it is soft, interest rates will rise. If he goes hard, he could help many Aussies in both cash crises and mortgage stress.

Watching the Treasurer and the Reserve Bank governor is akin to watching a bottle of milk falling from a counter top and knowing there is no way you going to stop it breaking on the floor. The government seem behaving like economic amateurs in the economic board game of life. Surely the voter’s must wake up to the possibility that this abysmal government has no economic policy to hang their hat on.

The greatest unseen inflation creating policy issue since the May 2025 election has been the insidious workplace “reforms” implemented by Albo and Chalmers that have destroyed productivity. Employers can’t even discuss an underperforming employee’s poor productivity with them without opening themselves up to claims of bullying, or worse, a workers comp claim from the employee for the “psychological injury” such a discussion caused them. Add the virtual compulsory maintenance of work from home workforces and its resultant additional reduction in productivity (irrespective of what the unions and employees themselves try to tell you) and we have an inbuilt, irreversible inflation bulldozer.

I doubt that the RBA board have a clue about these issues and it’s probably why their interest rate lever hasn’t got a hope of being calibrated properly or actually working.

Just for the record, what the RBA has done, was to put their foot on out heads and crew it into the ground after we’ve already fallen on our faces.

Yes, I did economics 101 but the inflation we are experiencing is not from discretionary spending, it’s related to world events, where petrol prices have almost doubled overnight, and because we are so dependent on the transportation of goods by road, this means increases on everything we consume from the supermarket, including the poor farmers, who have to also pay more for fuel and animals feed due to transportation costs, and the list goes on………. none of this is discretionary its vital to our existence, and can’t be avoided.

Also, let’s not forget the indiscriminate spending of the government contributing to the inflationary pressures.

So here we are, until we are all down with nowhere to sleep and begging for a few cents to buy a bread roll the RBA simply won’t stop applying their meaningless formulas trying to kerb inflation, when will it stop!? What a joke.

You typically play the Blame Game They RBA are doing a good job Back off!!

“Based on labor market analyses for early 2026, employers in Australia are experiencing structural shortages across multiple industries, with the construction sector facing a massive shortfall of 300,000 skilled workers. While overall labour shortages have slightly eased from 2025 highs, 69% of employers expect to be impacted by shortages in 2026.”

AND………………………………………………………………………………………………………………………………..

“Over 920,000 people in Australia are currently receiving unemployment payments (JobSeeker and Youth Allowance), with a significant 60% (557,000) relying on this support for over a year, according to ACOSS data from early 2024.

Total Recipients: > 920,000

Long-term Recipients (> 1 year): 557,000 (approx. 60%)

Partial Capacity to Work: 363,000 (40%)

Unemployment Payment Rate: 6.0% of the labor force, as of mid-2023, though this has recently risen”

SO…………………………………………………………………………………………………………………………………

STOP importing “potential employees” , RETRAIN the “unwilling” 557,000 [ see above ! ]

[ and the potentially 920,000 if unchecked / discouraged !!! Like the rampant NDIS !!! ]

CUT the burgeoning IMMIGRATION intake and CUT OUT the welfare which is making

“unemployment” a viable option to contributing-their-fair-share-in-taxes and working !

Key Shortage Figures : Construction: Shortages are projected to reach 300,000

Energy Sector: Australia will require an additional 53,000 to 84,000 electricians

Aged and Disabled Carers: 74,900 additional workers.

Software & Applications Programmers: 42,200

Registered Nurses: 40,400

And the most vocal “basket case” of all ……Victoria Specific:

Over 350,000 new workers are expected to be needed in Victoria by 2026

(137,000 for new jobs and 215,000 for replacement/retirements).

SO…………………………………………..There should on the basis of those figures be plenty of choices for the “unemployed” and /or “under-employed” to RETRAIN INTO and find a job

and START CONTRIBUTING and STOP TAKING from “their fellow Australians” !

AND……………..THE CHERRY ON THE TOP OF THE “Economic ” CAKE ………………………

“As of February 2026, combined unemployment and underemployment in Australia reached 3.61 million people (22.2% of the workforce), marking the highest level since early 2020. This high “under-utilisation” represents significant lost wages, estimated at over $24 billion annually in previous analyses, while public expenditure on employment services remains around $1.2–$1.3 billion yearly”

AND………………DUE TO LACK OF FUEL…..THIS WILL RAPIDLY BECOME MUCH WORSE !

So , with all that “lost taxation” [ Mostly “income tax” and even , from spending , GST ]

it’s PAST BEING NECESSARY to revise the EMPLOYMENT LAWS , THE WELFARE and the

OBLIGATIONS of ALL AUSTRALIANS to contribute to the ECONOMIC CAKE !

That would certainly rein-in a lot of unnecessary expenditure , fill a lot of job vacancies ,

cut the need to import skilled labour , reduce the expected demand for EVER MORE HOUSING and SERVICES , and provide the public with better services that they are already PAYING FOR but not receiving ” due to lack of staff , and other priorities” , ….and “Please hold the line but be assured , we value your time and a staff member will be with you as soon as they can , all staff are currently engaged attending to other customers……”

the universal excuse for really poor service……..or the Government answering service as I have experienced it !

My husband and I ( 56yrs married), both retired and over 80 have not received an aged pension since the measly amount was cancelled in 2016. We need to move due to difficulty managing our current property but cannot find another house that we can buy.

I left the UK in 1969 as an employed person, still employed until 2010 and came to Australia employed 3 weeks after I arrived. Now we are aged 80 and 82. We do not received an aged pension due to careful budgeting and savings and care management of a small number of shares.

I am currently seeing a lot of people who do not see the need to contribute to Australia’s and am as disappointed as I was when I left the UK.