The RBA says practically nobody is in negative equity. But modelling says one more rate rate hike could push some into real mortgage stress.

Who’s right and who’s wrong? Or could both be right in different ways?

This week gave us a fresh demo of the disconnect between the data Martin Place leans on and the numbers flying around the rest of the country. On Thursday, Michele Bullock fronted Senate Estimates in Canberra and told the room what every mortgaged Australian wants to hear: practically nobody is sitting underwater on their home loan.

Asked in Q&A whether first home buyers on 5 per cent deposits could end up in negative equity if prices fell, the Governor’s answer was blunt. “Practically no-one was in negative equity.” She paired it with a caveat that has had less airtime.

“Negative equity matters if people get into trouble with their loans, and then they have to sell their homes to meet that. That’s why a strong employment market at the moment is really important.”

A few weeks ago, however, delivered the opposite headline: more mortgage holders are now at risk of being in stress with their repayments.

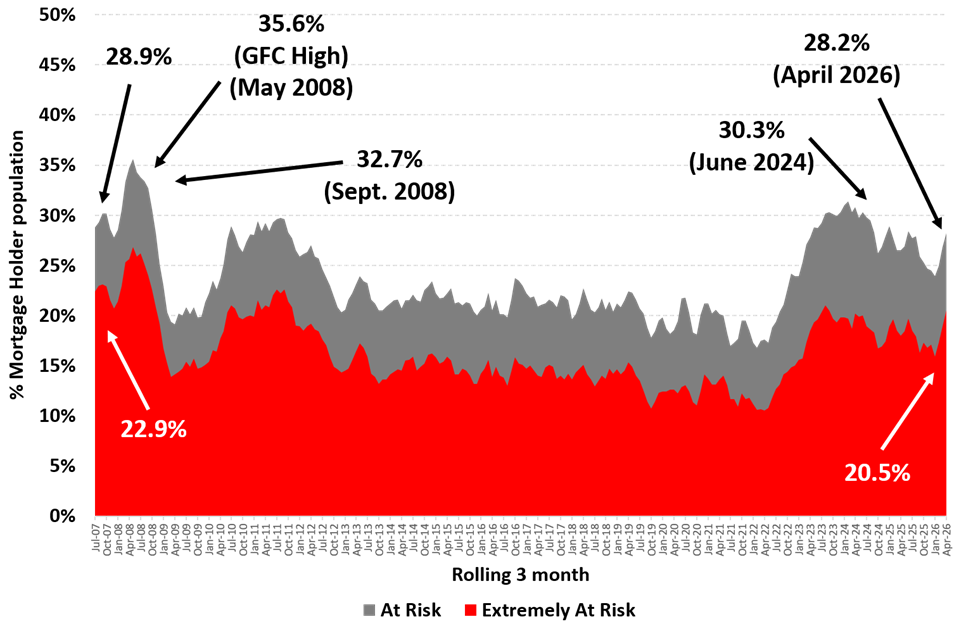

Source: Roy Morgan

Roy Morgan mortgage stress modelling, covering the three months to April 2026, puts 28.2 per cent of Australian mortgage holders, or 1.47 million people, at risk of stress. If the RBA goes again in June and lifts the cash rate to 4.60 per cent, Roy Morgan models that share rising to 30.7 per cent, or 1.6 million holders, by July. A 4.60 per cent cash rate would be the highest setting in nearly 15 years, since November 2011.

So who’s on the money?

Technically, both are. They’re not measuring the same thing.

Negative equity, where the loan owes more than the house is worth, is uncommon in this country. That’s because property prices have refused to behave like prices in any other asset class. Plus, Australians have not spent the past three years racing each other to take out high-LVR loans on properties that subsequently tanked. The RBA’s most recent Financial Stability Review puts the share of mortgaged households in negative equity below 1 per cent, lower than pre-pandemic levels.

Mortgage stress is something else entirely, however. And you don’t need to be in negative equity to feel the strain.

Roy Morgan’s measure looks at the share of households whose mortgage repayments are eating an unsustainable chunk of their after-tax income. You can be a long way from owing more than your house is worth and still be one rate hike away from giving up the family car or the next school holiday. It’s the difference between having the water at your neck and above your head.

The arrears data sits somewhere in between. APRA’s most recent Quarterly ADI Property Exposures release, covering the December 2025 quarter, has non-performing residential mortgages at 0.99 per cent. That figure is already above the post-GFC peak of roughly 0.9 per cent recorded in mid-2011, but it has eased from a cyclical high of around 1.07 per cent in mid-2025 as the RBA’s 2024-25 rate cuts started to flow through.

Negative equity isn’t the binding constraint here, because Australian house prices have done what they always do. The binding constraint is employment, because mortgage stress only turns into arrears the moment an income stops covering the repayment. Bullock said as much. A strong job market is what holds the line.

For now, the line is holding. Arrears are running below their mid-2025 high. The job market has not cracked. But three hikes have already gone through this year, more are priced in, and the cushion is thinner than it was 12 months ago.

General information only. Not financial product advice. Consider your objectives, financial situation and needs, and seek licensed advice before acting. Past performance is not a reliable indicator of future performance.