On a recent podcast, Scott Galloway and Ed Elson made a call: the standout new listing to watch right in the coming days is not SpaceX. It is a little-known Italian company that has spent two years buying up a graveyard of faded web brands, and turning them around.

SpaceX has already been and gone as the headline float. It listed on the Nasdaq in mid-June at a valuation near US$1.8 trillion, the largest IPO on record, and rose about 19 per cent on day one. Galloway and Elson say the bigger first-day jump could come from a much smaller name: Bending Spoons.

What it is

Bending Spoons is a software company based in Milan, founded in 2013 and run by co-founder Luca Ferrari. Its model is a roll-up. It buys established consumer and web brands that have a loyal user base but weak finances, cuts costs, and pushes them back to profit on subscription revenue. It has made more than 50 acquisitions.

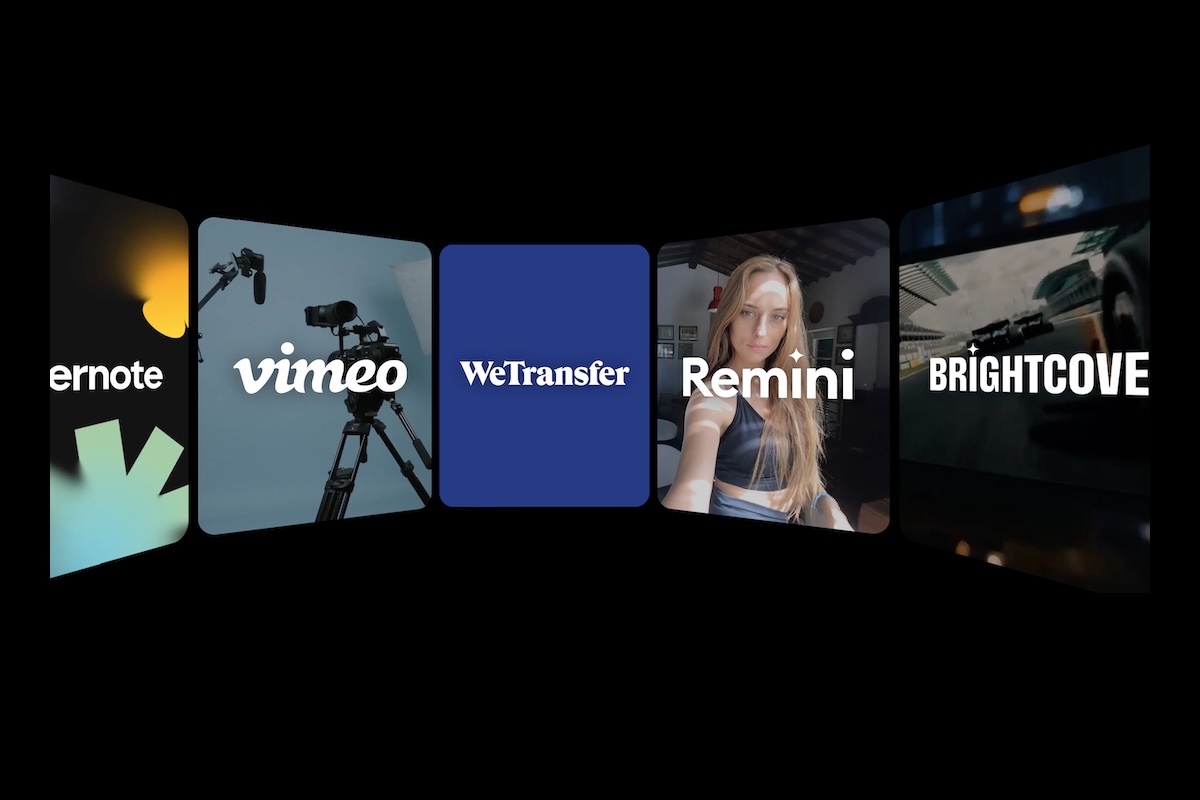

The brands are ones plenty of Australians have used and half-forgotten: Evernote, Eventbrite, Meetup, Vimeo, the file-sharing service WeTransfer, and, since the start of this year, AOL. In its most recent quarter subscriptions made up about 84 per cent of revenue.

In its IPO filing the company disclosed that more than 90 per cent of its code changes in the first quarter of 2026 were written or co-written by AI, around 70 per cent of them entirely by AI, part of how it strips cost out of the businesses it buys.

By the numbers

In the first quarter of 2025 Bending Spoons booked US$259 million in revenue and a US$112 million net loss. A year later it booked US$601 million, up 132 per cent, and swung to a US$27.5 million profit. Full-year 2025 revenue was US$1.31 billion, up 95 per cent.

Bending Spoons plans to list on the Nasdaq Global Select Market under the ticker BSP. The marketed range is US$26 to US$28 a share, for around 58 million shares, raising up to about US$1.62 billion and implying a valuation near US$18 to US$19 billion at the top of the range. Goldman Sachs, J.P. Morgan and Allen & Co are leading the offer. Pricing is expected on 30 June, with first trade on or about 1 July.

The “six to eight times revenue” that makes the deal sound cheap only holds if you annualise that bumper first quarter, roughly US$2.4 billion. Against the revenue the company actually reported for all of 2025, US$1.31 billion, the same valuation is closer to 14 or 15 times. Which figure you use decides whether it looks like a bargain.

Galloway and Elson argue the market’s attention, and its money, has gone to AI and a handful of giant American names, leaving a profitable, fast-growing European company priced as an afterthought. Their bet is a sharp first-day pop. The open will test it.

The call was made on Prof G Markets, hosted by Scott Galloway and Ed Elson. The show is on YouTube.