19 April 2024

1300 794 893

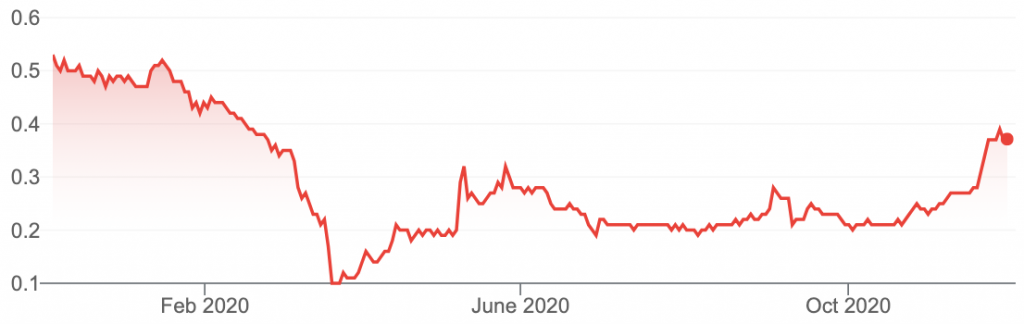

With a mere $220 million market cap entity, Myer (MYR) headed to microcap territory yet the once-esteemed retailer chalked up $2.6 billion of sales in the year to July 2020.

Takeover rumours abound.

Myer’s redemption story is one of a serious tilt to online sales, a channel that accounted for $422 million or 16% of total sales for the year.

The category more than doubled during the national lockdowns.

CEO John King sticks to an “aspirational” target of growing online sales to $1 billion.

He reckons that as a department store, Myer has the advantage of a better range, while the cachet of the Myer name provides succour to first-time online users (in other words, the retailer’s baked-on older customers forced to use ecommerce).

In theory, Myer could thrive with an online focus, which is more profitable. A wee problem is what to do with the excess store space – and in some cases whole redundant stores.

The retailer has won Covid-related rent concessions and is engaged in “constructive dialogue” with its landlords about its future footprint.

The space retreat is ongoing, with Myer reducing its coverage by 14,000 square metres in 2018-19 and 26,000 sq m in 2019-20. The retailer also has 76,000 sq m across 21 leases expiring within eight years.

That provides some serious leverage for dealing with the likes of Scentre and Vicinity, which aren’t known for taking a step back.

We reckon the latest revival effort, dubbed ‘customer first’, is the last chance for Myer, which has trotted out myriad remedial programs since infamously listing at $4.10 a share in late 2009 (ascribing a $2.3 billion market cap). It might take a (virus) crisis to implement the requisite hard decisions on store presence and staffing, rather than just tinkering with the merchandise.

Tim Boreham edits The New Criterion ([email protected])

Disclaimer: The companies covered in this article (unless disclosed) are not current clients of Independent Investment Research (IIR). Under no circumstances have there been any inducements or like made by the company mentioned to either IIR or the author. The views here are independent and have no nexus to IIR’s core research offering. The views here are not recommendations and should not be considered as general advice in terms of stock recommendations in the ordinary sense.