25 April 2024

1300 794 893

A question on the minds of a lot of my financial planning clients and subscribers is whether Afterpay is a good buy at its current price level. In fact, one of Australia’s greatest entrepreneurs and business-builders actually asked me that question only last week, so it’s time I came up with an answer.

I don’t own Afterpay but I’m conflicted as I taught economics to the co-founder and CEO Anthony Eisen, who was a great young man then, and others tell me he still is. I can’t say that for sure as no-one at Afterpay has helped me have an interview with him! What was that Blondie hit? That’s right, “Hanging on the telephone.” And what did Seth Godin say about the marketing department? That’s right — “Marketing is too important to be left to the marketing department.”

Anyway, that’s an aside to a big issue about whether APT can become an Amazon, Tesla or other tech stock that have defied critics, good sense and the history of share prices to keep on growing, even without profits!

There are objective tests for whether you buy a company on the stock market e.g. Is the price earnings ratio above or below 20? I used to worry about a company when the PE went over 20, especially when interest rates were around 5%, but now with interest rates so low, a PE of 30 or 40 is more acceptable.

(If you don’t understand why, buy my book Join the Rich Club, which we will be doing a special deal on for this week’s Black Friday promotion!)

APT’s PE is off the charts, while a company such as Tesla is at 79, Amazon is 91 and Zoom’s is, wait for it 505.29!

Growth companies like Zoom and Afterpay can defy logic and history and many people who invest in them are hoping they become the next Tesla.

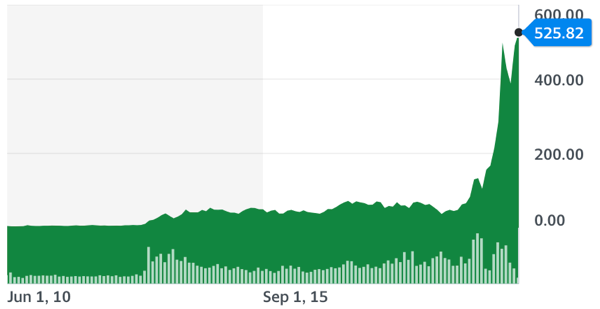

Tesla

We all want to own a stock like Tesla that does this, chart-wise, and we want to have a lot of money committed to it.

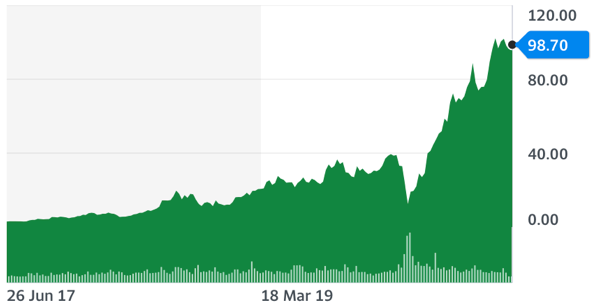

Below I show the chart for APT. While it hasn’t had a sensational rise compared to Tesla, it has done pretty damn well. So the question becomes: Will it do a Tesla? Will its stock price chart look like Elon Musk’s great work? Or will it lose its secret for its past success? Afterpay (APT)

Afterpay (APT)

I’ve always worried about regulation of the ‘buy now pay later’ space and how that could hit the stock price for APT. And lately the arrival of others ‘to eat the company’s lunch’ has me curious about how the company keeps growing and impressing the market.

A very good piece in the AFR by Tom Richardson brought some facts to light that anyone interested in APT should be aware of. I’ll sum up the points that grabbed my attention. So here goes:

• US customers grew by 16% to 6.5 million in the September quarter.

• Active merchants grew by 21% to 13,900.

• But US sales for the quarter were flat at $US1.6 billion!

• The pace of growth of rivals in the US has to be understood.

That last number was good but the growth wasn’t consistent with a “growth company”. But the company told the AFR that the June quarter being a ripper made September quarter look unimpressive in terms of growth.

And this could be vital for an investor wanting to get in, or get out with a huge profit.

If there’s a slowdown in US spending because of the infections spike, then this could be a temporary hiccup for APT. However, what if there are lot of others now eating their lunch?

The US consumer can now choose from PayPal, Affirm, Klarna, American Express, Quadpay and Sezzle in the BNPL space.

Citi research says Klarna, which is 20% owned by the CBA, added one million customers in the US over the last three weeks. And the size of Paypal has to be a concern, with 285 million active accounts and 385 million globally.

Against that, APT is still growing, with Richardson saying the company has added 15,000 new customers a day in October. But at the end of the day, this company needs spenders.

This company has always had huge range when it comes to what analysts think the company’s worth. A few months ago, Morgan Stanley was tipping it would be over $100, while UBS had it more like $29!

The consensus view is that the share price will fall 4.7% from the current level of $98.70, but this is what the analysts are saying right now:

Analyst Target Price

1. Citi $97.75

2. Morgan Stanley $120

3.UBS $30

4. Morgans $104.30

5. Macquarie $97.50

6. Ord Minnett $115

The majority are believers in the company and UBS will either have a lot of egg on its face or will be called a genius assessor of companies.

I think APT has challenges but more importantly, lots of challengers who look hungry to eat the Aussie company’s lunch. There is an argument that the new competitors can grow the whole BNPL market and incumbents can grow out of that, but there are also rivals from overseas coming here.

The AFR says Affirm, which is the third-largest BNPL player in the US by customer numbers, with 5.6 million, is coming to Australia. And it’s a serious player having “the highest number of monthly active users, with almost 300,000 customers using its platform in September this year, compared to about 200,000 for Klarna and Afterpay, according to Citi.”

(https://www.afr.com/rear-window/afterpay-s-us-reconciliation-gap-hard-to-explain-20201123-p56h1n)

Afterpay is a great aussie success story, but I am not convinced that it is the next Tesla.