Stocks

are expected to open up today but are still down 7% since the start of the

year, while we all know that house prices are falling as interest rates choke

off the boom that started when Bill Shorten lost the May 2019 election.

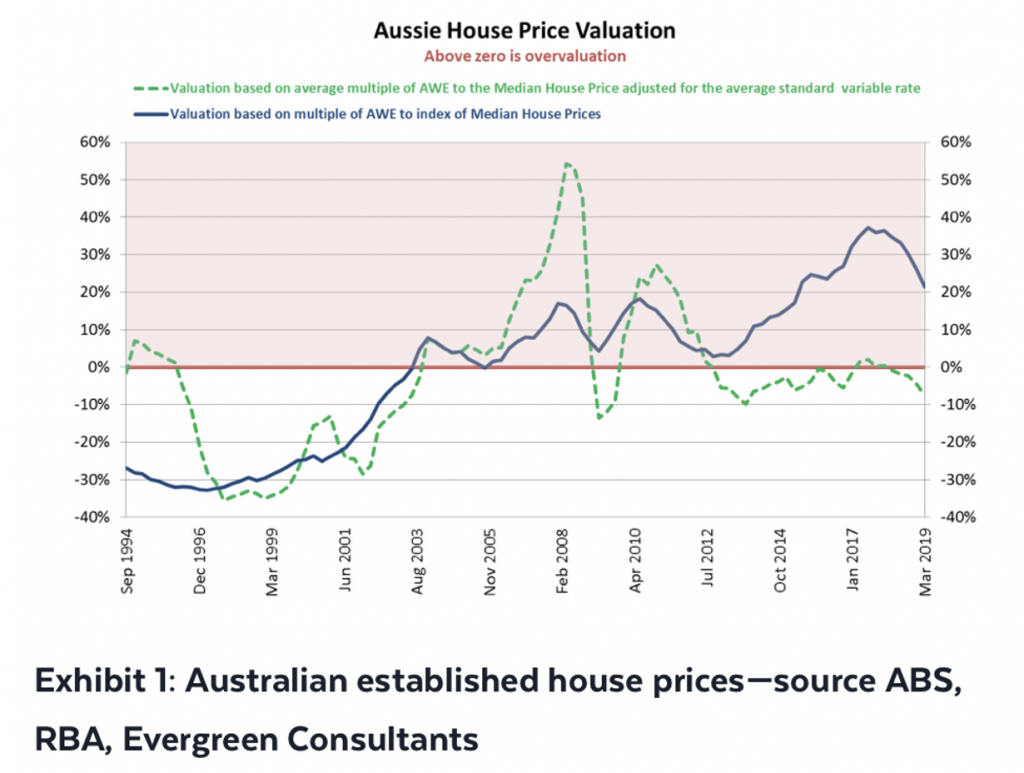

This huge surge in property prices was helped by Covid forcing interest rates down to rescue levels, pushing what we pay for homes close to 30% since the middle of 2020 nationally. And if you want more price growth numbers, take this from the SMH in December last year:

“Sydney

house prices have more than doubled in the past decade, rising 146.4 per

cent in the 10 years to October 2021, a Ray White analysis of CoreLogic

data showed. That was followed by Hobart, up 117.6 per cent, and Canberra, up

108.2 per cent over the same period.”

So who pays $80 million for a Melbourne mansion tagged the ‘ghost mansion’? The Australian’s John Stensholt tells us it’s an ‘unknown’ 26-year-old Aussie called Ed Craven.

His business is called Stake.com but when you

Google it to see what it does, we get this notice: “Sorry, Stake isn’t

available in your region.” So what does the business do?

Wikipedia says: “Stake.com offers traditional casino games (such as slots, blackjack and roulette) and sports betting. It offers video streams with live dealers. Users on Stake.com typically do not deal with traditional currencies, instead, they deposit and withdraw cryptocurrencies to and from their betting account.”

It's thought

the betting site is among the first online gaming

sites to exclusively use cryptocurrency as

a medium of exchange. So it’s double gambling — playing blackjack online

while punting on your bitcoin stake not going down.

I guess it can be a win-win, loss-loss or you could lose half your stake if the cards go against you but the other half you have left could double in value while you’re gambling!

But one thing Ed Craven has proved by buying this

Toorak mansion on 7,200 square metres of land, is that the house always wins

with casinos.

This landmark property was owned by David Yu of Ausvest Holdings and was never finished, hence its nickname “the ghost mansion”.

Yu bought the place in the recession year 1991 from

Leon Fink for $5 million. Fink used to own Hoyts cinema business and Triple M,

in the top-rating days of Doug Mulray in Sydney and the Degeneration crew which

starred the likes of Rob Sitch, Tony Martin, Jane Kennedy and Mick Molloy.

David Yu

hasn’t struggled, owning more than 40 Melbourne properties, but in 2001 he sought approval to demolish

Ed’s new house to make way for a five-storey apartment block. Since the

planning application was rejected in June of that year, the house he bought in

1991 for $5 million has stood empty.

But I guess $5 million turning into $80 million

over 30 years is an ok return — it’s about 10% plus a year, so he could have

slammed it in a good industry super fund and gone close, but he wouldn’t have

had the tax deductions!

Back to Ed’s house and it’s not the most expensive

sold, with Mike Cannon-Brookes taking out that one with his $100 million

purchase of Fairwater on Sydney Harbour, which was owned by the Fairfax family

of SMH and AFR fame.

Interestingly, John Stensholt points out that a top-level apartment at Sydney’s Barangaroo sold for more than $100 million, which makes me ask questions about the severity of this expected house price crash.

All this is interesting but what about Ed’s

business that has bankrolled it all?

Sarah Danckert at the SMH and the Age looked at Ed’s business Easygo Gaming in humble digs in Melbourne, late last year, and revealed how this start-up, co-founded with 27-year-old Bijan Tehrani, also owns Stake.com. “Within a few short years, Stake.com has processed tens of billions of bets on sports, slots and casino table games,’ Danckert wrote. “Industry observers conservatively value the operation at $1 billion.

The business is actually the shirt sponsor for EFL Championship football team Watford, which was once owned by Elton John.

Interestingly,

online casinos are banned in Australia but not in the US, and given the Watford

sponsorship of $9 million, Poms can gamble at online casinos.

By the way, Ed also previously bought another Melbourne mansion in Orrong Road, Toorak for $38 million. I guess the moral of this story is that not only does the house win with casinos, but the casino owners also win a pile of houses!

In

fact, the history of the very rich is to start a great business and buy great

properties — it’s as safe as houses — but learn from the Fink/Hoyts story,

don’t borrow too much.