Moving people and things around the world by sea has a big climate impact. The shipping industry produces almost 3% of global greenhouse gas emissions – roughly the same as Germany – largely due to the movement of container ships, bulk carriers and tankers.

Under international rules, these emissions are not included in any nation’s greenhouse gas reporting. That means they often escape scrutiny.

Unlike cars, international shipping can’t shift to using low-emissions electricity – the batteries required are too big and heavy. So clean fuels must play a role.

A proposed shake-up of the global shipping industry would encourage the use of clean fuels and penalise shipping companies that stick to cheaper, more polluting fuels. Should it proceed, emissions from global shipping would be regulated for the first time.

Using our peer-reviewed modelling, we investigated how the changes might affect Australia’s largest export: iron ore.

What is the proposed carbon levy all about?

The International Maritime Organisation (IMO) is the United Nations body responsible for regulating international shipping. It recently approved a draft plan to tackle the shipping sector’s contribution to climate change through a type of “cap and trade” scheme.

The plan would involve setting a limit, or cap, on how much each shipping company can emit. Companies must then either buy credits or be penalised if they go over their limit. Companies that stay under their limit – for example, by using cleaner fuels – would earn credits, which they could then sell.

In this way, high-emitting shipping companies are penalised and low-emitting companies are rewarded.

Under the plan, the total limit for emissions from global shipping would fall each year. This increases the incentive for companies to switch to lower emission fuels and makes higher-emission fuels progressively more expensive to use.

The plan is scheduled to be adopted by the shipping industry in October this year and would begin in 2027.

Not all fuels are the same

The proposed change is particularly significant for Australia. As a remote island nation, our imports and exports are heavily reliant on massive ships. This is most important for our commodity exports – iron ore in particular.

Our recently published modelling estimated the emissions and financial impacts of various low-emission shipping options for Australia’s exports.

We estimated Australia’s commodity exports create about 34 million tonnes of greenhouse gases a year. This is about 8% of Australia’s domestic greenhouse gas emissions, but it’s not included in Australia’s national reporting.

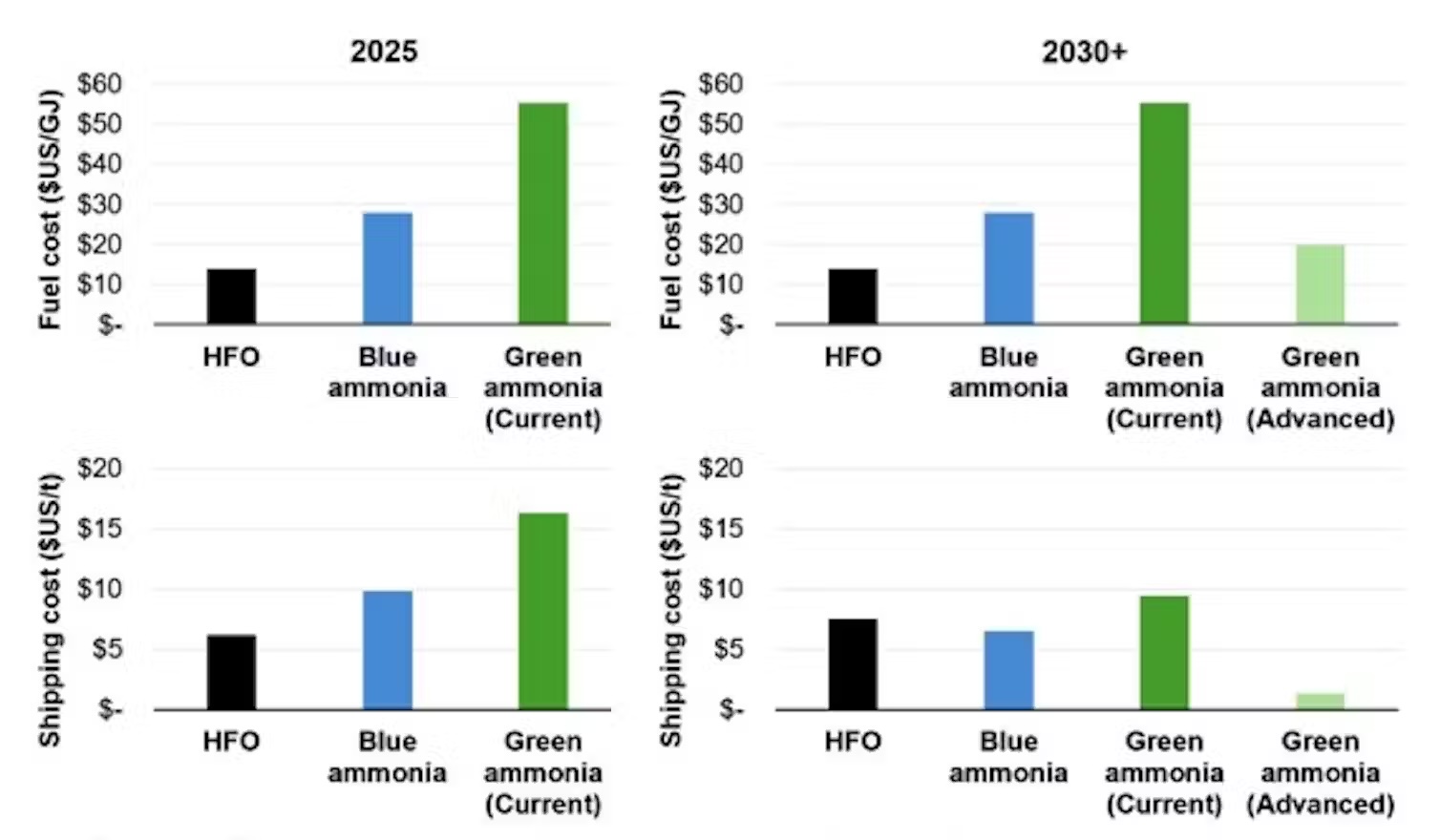

Using the same modelling, we then examined how the proposed new regulation would affect the cost of shipping Australia’s largest export, iron ore. We chose a common route from Port Hedland in Western Australia to Shanghai in China.

First, we looked at current fuel costs, as well as overall shipping costs measured per tonne of delivered ore. Shipping costs include both the fuel costs and the cost of the ships designed to use it. Then we estimated how much fuels and shipping might cost from 2030, assuming the proposed regulation has come into force.

We also examined three types of fuel.

The first was heavy fuel oil (HFO), one of the main fuels used in international shipping. It’s traditionally the cheapest shipping fuel and also has the highest greenhouse gas emissions.

The second was “blue” ammonia. This fuel is typically made from natural gas using a manufacturing process where the carbon in the natural gas is captured and stored. It has lower greenhouse gas emissions than heavy fuel oil, but it is not a “green” fuel.

Thirdly, we looked at “green” ammonia, which is produced using renewable energy. We examined two types of green ammonia - that produced using current technology, and “advanced” green ammonia, made using new technologies in development.

Is green ammonia an answer?

From about 2030, the overall cost of shipping powered by heavy fuel oil will start to rise significantly under the proposed regulation. That’s because shipping companies using this fuel must purchase credits from those using cleaner options.

Blue ammonia may then make it cheaper to ship iron ore from Australia to Asia. Users of this fuel could generate and sell credits that higher-emitting fuel users buy, offsetting some of the shipping costs associated with using blue ammonia.

But if international shipping is to reach the IMO’s goal of net-zero emissions by about 2050, this is very likely to require a green fuel.

However, green ammonia is more expensive than heavy fuel oil and blue ammonia with current technology. And our analysis found the proposed regulation – and associated subsidy – doesn’t make it the lowest cost shipping option from 2030 onwards either.

This is why technological innovation is important. CSIRO projections of the future costs of renewable energy and green-fuel manufacture suggest that, should technologies improve, green ammonia may compete on cost with heavy-fuel oil in the 2030s, even without subsidies.

If so, this zero-emission fuel could become the cheapest way to export Australian iron ore.

Looking ahead to net-zero

As our calculations show, a combination of regulation and innovation could help international shipping achieve its goal of net-zero emissions.

These fuels could be made in Australia, and potentially used by other industries such as rail, mining, road freight and even aviation.

Such an industry would therefore contribute significantly to the world’s emission-reduction goals, and could help Australia realise its ambition to become a major global exporter of green fuels and other green products.![]()

Michael Brear, Director, Melbourne Energy Institute, The University of Melbourne; Gerhard (Gerry) F. Swiegers, Distinguished Professor of Chemistry, University of Wollongong; Michael Leslie Johns, Professor of Chemical and Process Engineering, The University of Western Australia; Nguyen Cao, PhD Candidate in Mechanical Engineering, The University of Melbourne, and Rose Amal, Professor of Chemical Engineering, UNSW Sydney

This article is republished from The Conversation under a Creative Commons license. Read the original article.