Should you buy stocks during a conflict like Iran vs Israel?

It’s the kind of headline that rattles even seasoned investors: conflict flares up in the Middle East. Iran fires at Israel. Oil prices move. Markets wobble.

Your gut reaction? Probably something like: “Time to sell? Should I sit this one out?” We're one week on from the escalation of the conflict, and markets have been wringing their hands all week over the implications on trade, oil prices and more.

If you ask some of Australia’s sharpest market minds, you might hear a very different answer: actually, this might be exactly the time to buy.

Buying season's open

That’s the view from TenCap's Jun Bei Liu, who’s seen plenty of these market shakeouts before.

Should we be buying right now? We asked Jun Bei on this week's Switzer Investing TV:

“Absolutely. Definitely.” she replied without a moment's hesitation.

She adds that these downturns often come after a burst of scary headlines, typically over a weekend, which fuels a Monday market sell-off — but then sentiment stabilises.

“We often catch up on Monday, and things usually happen on Friday or over the weekend — then they get worse, and Monday is always the major sell-off day.”

But those same scary headlines, she argues, create the very opportunities smart investors wait for.

“Look—it is a good buying opportunity. To be honest, I think the market is responding not as badly as we initially saw on Friday. Yes, there’s a broader sell-off, but it’s not that bad. It’s quite orderly.”

And for those with a shopping list of quality stocks, she’s crystal clear:

“If there’s continued weakness, you just buy the companies you’ve always wanted to own. You top up. I think it’s a great opportunity.”

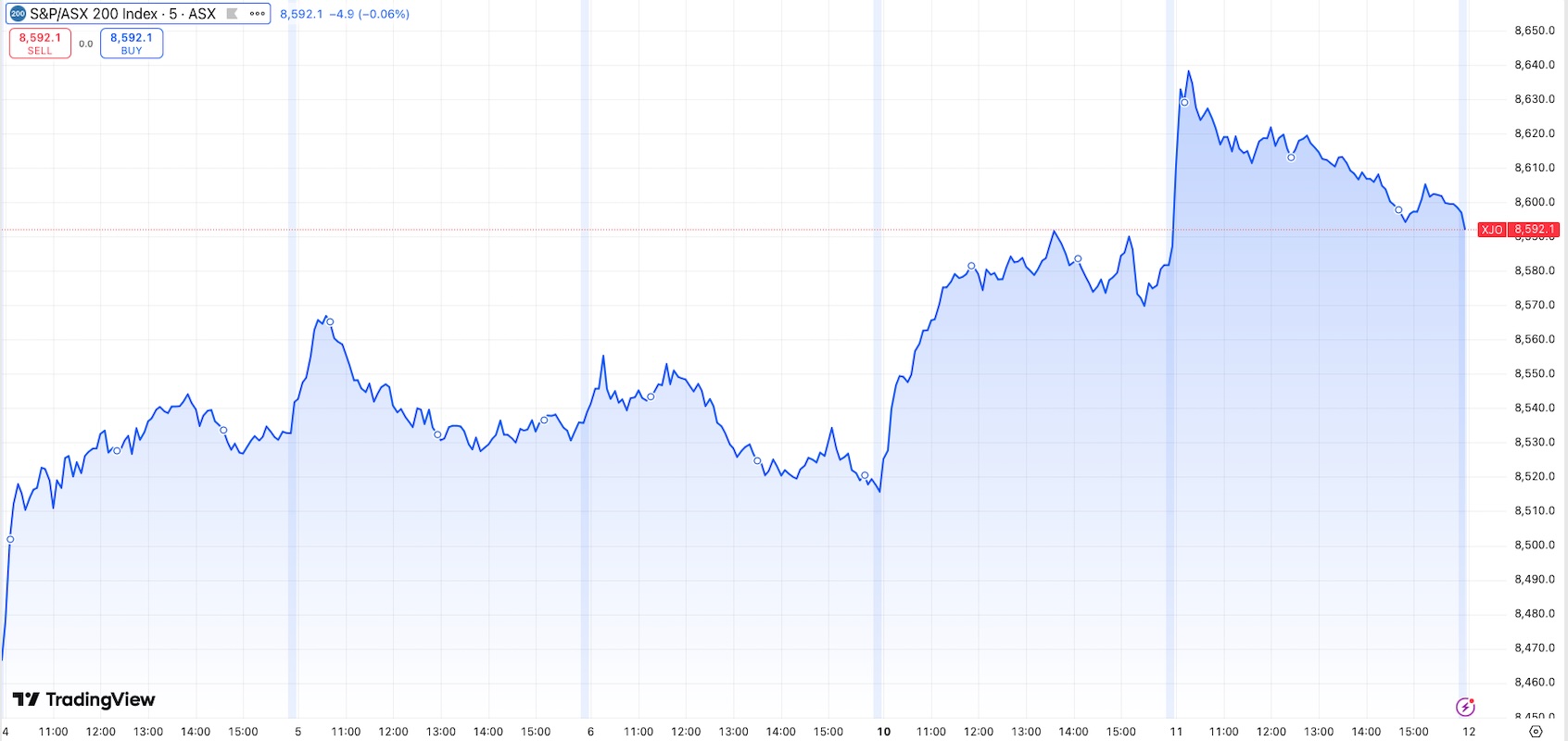

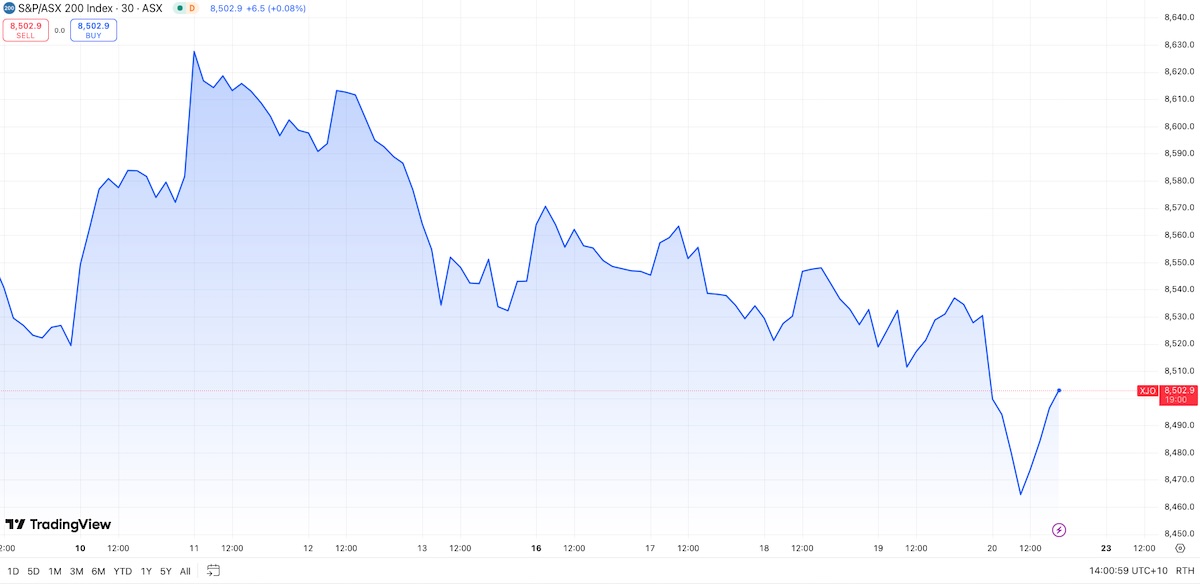

The week that was according to the ASX200 (XJO) index.

Markets climb the wall of worry

It’s not just Liu leaning in.

Michael Wayne from Medallion Financial sees history repeating itself in how markets handle geopolitical shocks like Iran vs Israel:

“There are always these global events. When you look back through history, you can pick any decade — there’s always flare-ups. Markets tend to climb the wall of worry.”

In other words: short-term fear, long-term opportunity — if you stay disciplined.

Wayne acknowledges that investors can’t predict these events, but says market resilience in the face of conflict is often underappreciated.

“We’re cautiously optimistic. We tend to be like that most of the time.”

The economist’s take: don’t panic

Michael Knox, Chief Economist at Morgans, sees little reason for markets to unravel in response to the Iran–Israel conflict specifically.

“To be frank — honestly — I don’t think we should be worried.”

He notes that while Iran grabs headlines, its oil production isn’t large enough on its own to cause global supply shock:

“Iran, of course, is an oil producer — but it’s a relatively small oil producer in comparison to the others I’ve just mentioned. So it’s a short-term scare — but I don’t think it’s a major problem.”

Knox is also quick to remind investors that Saudi Arabia and its allies are well protected militarily:

“The Saudis are well defended behind their own missile shields… I don’t think that’s such a big problem.”

Keep watch, buy smart

If you only read the headlines, a Middle East conflict might sound like the moment to pull your money and run.

But for professional investors who’ve seen this pattern before, these sell-offs can be exactly when long-term opportunities emerge — especially if you’re disciplined enough to focus on quality companies rather than reacting to daily noise.

“That’s what the share market is,” Liu summed up. “You’ve got to buy future earnings, right? You’ve got to be optimistic to expect what’s to come.”

And if the pros are right, this latest market wobble could turn out to be more of a buying window than a warning light.

Watch this week's episode of Switzer Investing TV below.